Company Overview - Vocus Communications Limited is an integrated telecommunications provider. The Company is engaged in providing telecommunications and other services to customers across Australia and New Zealand. Its segments include Australia and New Zealand. It supplies broadband, fixed voice, mobile, data center, cloud and energy services to consumer and business segments through the Commander, Dodo and iPrimus brands in Australia, and Slingshot, CallPlus and Orcon in New Zealand. It offers data network solutions, including Dark Fiber, which is a fiber-optic point-to-point connection; Ethernet services; Ethernet Multipoint, which simplifies layer 2 connectivity across multiple offices or data centers, and Internet Protocol Wide Area Network (IP WAN), which converges information and communications technology services, such as Internet or Cloud Connect. It offers unified communication services, and also the cloud services, including cloud computer, backup and archive, and disaster recovery services.

.png)

VOC Details

Agreement with Alcatel Submarine Networks:Vocus Communications Limited (ASX: VOC) has executed the binding agreement (contract-in-force) with Alcatel Submarine Networks (ASN) to construct the Australia Singapore Cable (ASC). The ASC project is expected to cost about US$170 million over the build period, which will take over 19 months to build, while the finishing is targeted by August 2018. The group’s balance sheet is expected to accommodate this with leverage only rising to a peak of about 2.4x at FY17. Primarily, ASC has been projected to be funded from the present debt capacity in fiscal year of 2017, and for FY18 and beyond, the project is funded from a combination of current debt capacity, operating cash flow. VOC is expecting to receive IRU pre-payments of around $US100 million during the build period. The ASC project’s effective life is estimated to be a minimum of twenty-five years. Additionally, after finishing Nextgen Networks acquisition, VOC had confirmed that it got Singapore IDA approval and renewed Landing Rights with MoCIT in Indonesia, which fulfils all the necessary requirements to start and finish the project in combination with moving to a contract-in-force with ASN. VOC now has a unique competitive advantage in combination with the Nextgen network, which provides a platform to increase utilization of both assets. On the other hand, ASC has made the binding Landing Co-operation Agreement with XL Axiata Tbk to offer security of tenure, commercial arrangements and nation-wide coverage in Indonesia through XL’s 21,000km domestic transmission network.

.png)

ASC Project (Source: Company Reports)

Acquisition of Nextgen Networks and strategic opportunities:After the acquisition in October 2016, VOC is in the process of integrating the Nextgen business. Vocus planned to expand its connection points to the NBN from 68 to 112 of a possible 121 nationwide NBN points of interconnect (POIs). The acquisition provided the greater control over its cost base and expanded the VOC’s competitive product offering for corporate, government and wholesale customers. Moreover, the acquisition included two infrastructure projects, North West Cable System (NWCS) and Australian Singapore cable (ASC) project, which will open-up further strategic opportunities.

Integration in process:VOC is completing the integration of the Amcom business with the synergies target of $13-15 million, expected to be achieved by the end of FY17. The merger with the M2 business is also proceeding with all integration milestones being met and the $40 million synergy target is on track to be completed by the end of FY18.

Strong FY 16 Financial Performance:Vocus has reported an outstanding 455% growth in the revenue to $830.8 million for fiscal year of 2016, and generated a 318% growth in the underlying EBITDA to 215.6 million. This solid performance was mainly on the back of Amcom Telecommunications Limited contribution coupled with four-month contribution from the M2 Group. Ongoing growth from Consumer and Corporate segments coupled with growth in services in operation in major market segments also drove the performance. The group is growing their market share in Australian National Broadband Network (NBN) and New Zealand Ultra-Fast Broadband (UFB) rollouts. The group reported a 461% growth in the underlying NPAT to $101.7 million. VOC in FY 16 has posted a 300% growth in the final dividend and generated 388% growth in the full year dividend to 15.6cps. Meanwhile, for first quarter of FY17, the group’s Australian corporate and wholesale business delivered a decent sales growth, in line with earlier quarter and generated a net new monthly recurring revenue of $1.35 million during the quarter. The group’s overall market share of NBN subscribers rose to 7.4% during the quarter against 6.4% in June 2016 driven by consumer division. But broadband consumer growth did not reach expectations.

Change in the leadership: VOC had announced the resignation of James Spenceley and Tony Grist as two of its board members. The resignations are after a difference of opinion between the Departing Directors and the Board on an alternative leadership framework whereby the CEO would change in early 2017. The board member search is ongoing and the group expects to appoint the same by second half of 2017. Moreover, VOC’s CFO search is underway and will soon be appointed. Meanwhile, John Allerton, VOC Head of Commercial and Regulatory has been appointed as interim CFO to ensure detailed handover.

.png)

Acquisition Synergies (Source: Company Reports)

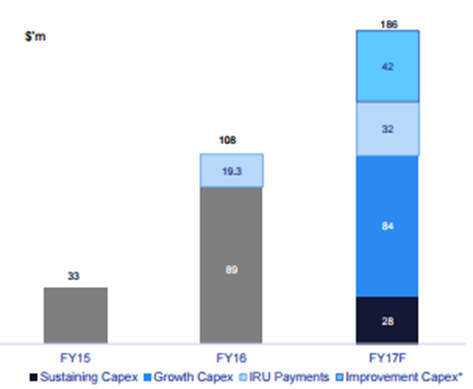

Outlook for FY 17:VOC expects the revenue to be approximately $1.9bn for fiscal year of 2017, while the underlying EBITDA is forecasted to be in the range $430m to $450m. Depreciation & amortization is projected to be over $98 million in FY 17 while FY17 NPAT is forecasted to be in a range of $205m- $215m, resulting to a low to mid underlying EPS growth. The reported net debt to the underlying EBITDA is expected to be approximately 2x by the end of FY17. Moreover, VOC expects to report a material below the line expense of about $105 million in FY 17. VOC is continually reviewing the business portfolio that may result from the sale of non-core assets or businesses. However, the FY 17 result would depend upon the performance of the second half of the FY 17 as the additional investment in consumer sales, marketing affected the first half of FY 17 and provisioning resources did not contribute to the expected revenue growth. Outages on the primary consumer broadband suppliers’ provisioning platform caused this disturbance. Moreover, there was delay for the completion of Nextgen and there is a slight underperformance of the business relative to the expectations. Additionally, the impact of high margin fiber build contract in the Corporate & Wholesale business are not being rolled forward (for which $10 million was EBITDA contribution in 1HFY16 and about $4 million EBITDA contribution in 2H FY16). On the other hand, Vocus is making further investments in the sales and marketing capabilities to leverage the portfolio of brands. VOC has planned to make investments in data analytics capability to take the advantage of the shift from copper to fibre occurring over next few years in both Australia and New Zealand in order to boost their market share, while reduce the customer churn. The capex in FY 17 is expected to be over $186 million, including the $32 million of IRU payments.

Capital Expenditure Projections (Source: Company Reports)

Stock Performance:Vocus stock price declined more than 55.7% in the last six months (as of December 09, 2016), due to the group’s lower than estimated projections for fiscal year of 2017. Moreover, management difference in opinions also hurt the stock sentiment. On the other hand, VOC is undergoing transformation from the past two years to become a fully integrated high speed telecommunication network across Australia and New Zealand. In fact, the group has transformed from a primarily wholesale internet and voice business to a full-service provider of telecommunication services to consumers, corporate and government. This is through a series of merger and acquisition efforts by leveraging the expanded infrastructure platform and market presence. The group is not concentrating on its non-core assets and is offloading them. Spark New Zealand is acquiring the remaining 50% of the Connect 8 fibre construction business from Vocus, who is their joint venture partner. We believe Vocus investments would start reaping benefits on a longer-term basis despite short term pressure. Even management expressed their expectation of a better demand for bandwidth for the coming ten-year period as compared to the past decade. With NBN and UFB rollouts, the group would be well placed to capture the commercial sector as well.

Moreover, the stock’s correction this year placed them at lucrative levels opening a bargain opportunity to investors. The stock also has a good dividend yield. We give a “Buy” recommendation on the stock at the current price of $4.09

.PNG)

VOC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...