Kalkine has a fully transformed New Avatar.

Company Overview: Vmoto Limited is a scooter manufacturing and distribution company. The Company is engaged in the development, manufacture, and international marketing and distribution of electric powered two-wheel vehicles, petrol two-wheel vehicles and all-terrain vehicles. The Company's geographical segments include Australia and China. The Company offers green electric powered two-wheel vehicles and manufactures a range of western designed electric two-wheel vehicles from its manufacturing facilities located in Nanjing, China. It sells its products on an original equipment manufacturer basis. The Company operates through two brands: Vmoto, which is aimed at the value market in Asia, and Emax, which targets the western markets with a premium end product. The Company has a total capacity of approximately 450,000 two wheel units per annum. The Company consists of approximately 40 outlets through a combination of its own retail outlets and third party distributors across China.

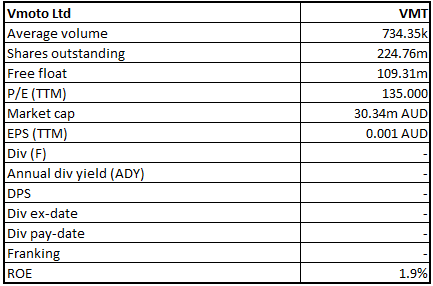

VMT Details

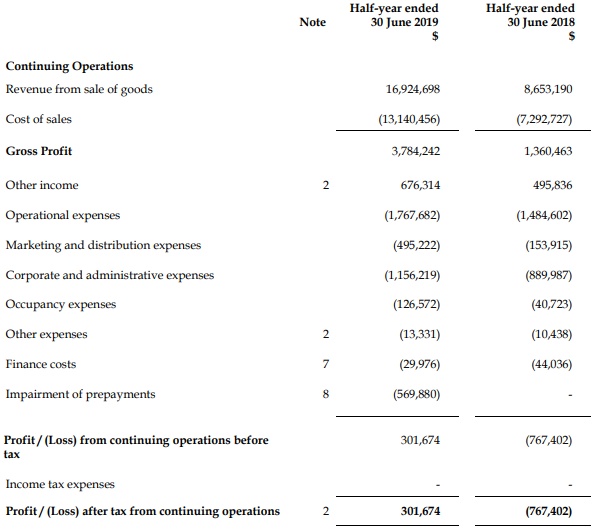

Long-term Strategic Drivers in Place: Vmoto Limited (ASX: VMT) is a global scooter manufacturing and distribution group. It specialises in the high quality “green” electric powered two-wheel vehicles and manufactures a range of western designed electric scooters from its low-cost manufacturing facilities in Nanjing, China. As on November 8, 2019, the market capitalisation of Vmoto Limited stood at ~A$30.34 million. The company released its results for six months period ended 30 June 2019, in which it delivered robust financial and operational progress with increased cash position by around $1.0 million via delivery of increased unit sales in the international markets and signing of a landmark agreement with Ducati. The company achieved numerous strategically important deliverables ensuring that it is perfectly poised to deliver continued growth in 2H and onwards. The company delivered its first positive EBITDA of $940,856 in 1HFY19 against loss of $303,875 in 1HFY18. This was mainly driven by the sale of high-value and high margin two-wheel electric vehicles into the international market. Revenue from continuing operation in 1HFY19 increased to $16.92 Mn, up 96% on PCP, mainly driven by growth in international sales, with 6,936 units of electric vehicle products sold into international markets during the first half of 2019. Out of the total sales unit of EV products, 6,893 units were sold to international customers and distributors. This demonstrates a continuing upward sales trajectory. The company witnessed a turnaround in 1HFY19 in terms of profitability from losses in 1HFY18 and recorded a significant rise of ~139.3% in NPAT, and the figure stood at $301,674 in comparison to the net loss of $767,402 for a six-month period to June 30, 2018. We presume that the company will continue to increase its order flows from customers in years to come, thus resulted in top-line growth.

During 1HFY19, the company managed to deliver robust operational and commercial growth as it has continued to progress the strategy of developing, manufacturing and distributing high quality “green” electric two-wheel vehicle products to international B2B sectors, which includes delivery, sharing and rental customers. The company retained robust cash position of $5.1 Mn, which was up $0.9 million in total since December 31, 2018. Finally, over the six-month period to June 30, 2019, the company’s net assets rose by 5% to $16 Mn as compared to December 31, 2018 figure of $15.3 Mn.

Moving forward, the company’s low-cost manufacturing facilities, decent cash position, high entry barriers to business model, strong brand presence in 35 countries, and potential to replicate European expansion model in other markets are expected to act as tailwinds for long-term growth. Also, orders from existing and new distributors and building distribution networks can also help the overall company in achieving growth objectives.

1HFY19 Income Statement (Source: Company Reports)

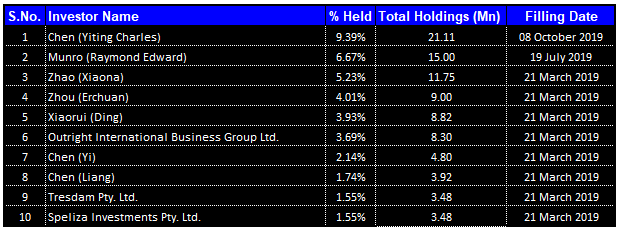

Top 10 Shareholders: The following image provides an idea of the top 10 shareholders in Vmoto Limited:

Top 10 Shareholders (Source: Thomson Reuters)

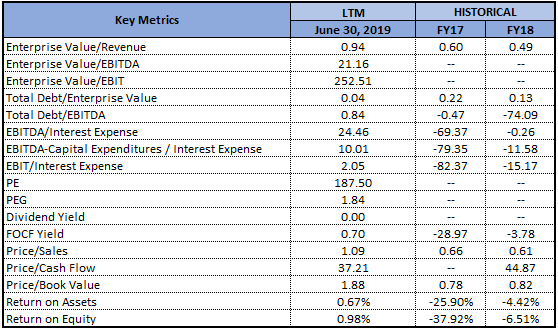

Improvement in Key Ratios: The company’s net margin stood at 1.8% at the end of June 2019, which reflects a significant improvement on a YoY basis, and, therefore, it can be said that VMT has decent capabilities to convert its top-line into the bottom-line. Its EBITDA margin stood at 5.5% as compared to the figure of -3.8% at the end of June 2018. The company’s RoE stood at 1.9% at the end of June 2019 as compared to -5.5%, and, therefore, it can be said that VMT has managed to deliver returns to its shareholders, which could attract the attention of market participants. The company’s current ratio stood at 1.83x at the end of June 2019, which is higher than the industry median of 0.99x, and, therefore, it can be said that VMT has better capabilities to meet its short-term obligations as compared to the broader industry. Also, respectable liquidity levels reflect that VMT could make deployments towards strategic business activities, which can help in achieving long-term growth. The company’s Debt/Equity ratio stood at 0.06x at the end of June 2019, which is lower than the industry median figure of 0.12x and, thus, it looks like VMT’s balance sheet is less leveraged as compared to the broader industry. It can be said that lower debt on the balance sheet reflects stability, and the company can focus on achieving long-term growth prospects.

.png)

Key Metrics (Source: Thomson Reuters)

Update on Activities for Q3 FY19: Vmoto Limited has recently come forward and provided an update on the activities for the quarter ended September 30, 2019 (or Q3 FY19), wherein it delivered robust operational and commercial growth. The company also continued to progress the strategy of selling high value electric two-wheel vehicle products into the international markets. The following image provides an idea of the sales performance for Q3 FY19:

International Sales Units (Source: Company Reports)

The company posted a robust rise in the total sales in Q3 FY19 and, in this period, 6,027 units were sold, reflecting a rise of 94% on Q2 FY19. For Q3 FY19, 4,839 of these units were sold in international markets, reflecting a rise of 57% on Q2 FY19 and an increase of 77% on 3Q FY 2018. Because of the continuous order flows from customers, the company’s sales continue to be on an upward trend, and there are expectations that the sales trend might continue moving forward. In order to help European sales growth, VMT has been pursuing additional sales opportunities in the B2B and B2C sectors, which includes sharing and delivery markets. It is exploring the potential to collaborate with world-renowned brands in the vehicle and mobility industry.

Overview of Order Book: As at September 30, 2019, VMT has firm orders for 4,421 units, and continued to receive further orders from its existing and new distributors post Q3 FY19. The company’s B2C products have been generating increased interest in motorcycle enthusiasts and trendy consumers. Also, the government policy and initiatives, primarily in Europe, which includes the offering of monetary incentives for utilising EV, green initiatives, banning of the petrol vehicles along with deployment towards charging infrastructure drives growth in the adoption of EV as transportation. It was also stated that these factors are anticipated to further drive growth when it comes to VMT’s sales.

Exclusive Distribution Agreement Inked with Hobbyzone LLC: During Q3 FY19, VMT has inked exclusive distribution agreement with Hobbyzone LLC for warehousing, distribution and marketing of B2C range of electric two-wheel vehicle products in Mongolia. The company added that Hobbyzone has robust experience when it comes to importing the electric scooters and other high-end retail products into Mongolia. VMT also supplied samples to and/or is in the discussions with numerous potential B2C and B2B distributors and customers in Cyprus, Brazil, Dominica, Czech Republic, Dubai, Egypt and Indonesia, Malaysia, Netherlands, Maldives, Panama, Nepal, Peru, Philippines, Russia, Singapore, Saudi Arabia, Thailand and Vietnam.

What to Expect from VMT Moving Forward: VMT has been executing its strategy of selling high value, high performance electric two-wheel vehicles in the international markets. Also, it is building a distribution network. And, the discussions with numerous other potential partners are ongoing worldwide. VMT’s robust sales network and ongoing marketing activities have been increasing brand and product awareness and are driving the healthy and growing pipeline of sales leads. The management of the company is focused on securing further firm orders from the new and present customers.

VMT is expecting significant potential in the B2B market for the high performance electric two-wheel vehicle delivery products. It is in discussions with numerous groups with regards to the cooperation agreements to secure orders.

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: The company’s stock has delivered a return of 37.76% in the span of the previous one month while, in the time frame of six months, it rose 22.73%. As at September 30, 2019, the company had a cash reserve of A$6.4 million as compared to Q2 FY19 figure of A$5.1 million, and an increase was because of cash receipts from customers for firm orders placed and products delivered during the quarter and the draw down of operating facilities. The cash position of the group remains robust and reflects an A$1.3 million rise on the previous quarter, and a total increase of A$2.2 million since December 31, 2018. During Q3 FY19, VMT drew down additional RMB5 million (around A$1 million) from the operating facility as working capital as it is preparing for an expected step up in the production, which is needed to meet the anticipated increasing orders from the customers. As at September 30, 2019, the total amount drawn down stood at RMB10 million (around A$2.1 million), and RMB15 million (around A$3.1 million) remains undrawn and available. By considering the aforesaid facts, decent outlook, replenishment orders from its existing and new customers, and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current price of A$0.130 per share (down 3.704% on 08 November 2019).

VMT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...