Company Overview: Virtus Health Limited is an assisted reproductive services provider engaged in the provision of healthcare services, including fertility services, medical day procedure services and medical diagnostic services. The Company has six operating segments: New South Wales, Queensland, Victoria, Tasmania, Australian Diagnostics and International. It has consolidated its operations into two segments, being an Australian aggregated healthcare services segment (Healthcare Services Australia) and an International healthcare services segment (Healthcare Services International). Its fertility clinics include IVFAustralia, Melbourne IVF, Queensland Fertility Group, Rotunda IVF and Virtus Fertility Centre. Its day hospitals include North Shore Specialist Day Hospital, Spring Hill Specialist Day Hospital, Mackay Specialist Day Hospital, City East Specialist Day Hospital and City West Specialist Day Hospital. It offers general pathology services, as well as specialist fertility and genetic testing.

.png)

VRT Details

Higher Investments & Increase in VRT’s IVF Cycle Activity are Key Positives: Virtus Health Limited (ASX: VRT) is engaged in providing fertility services, medical diagnostic services, and medical day procedure services. The company is one of the top leaders in offering Assisted Reproductive Services (ARS) in Australia, UK, Ireland, Singapore, and Denmark. VRT has greater than 125 fertility specialists with more than 1,300 professional staff all over the world.

For the half year ended 31 December 2019, the company’s revenues increased approximately 1% year over year. EBITDA for the period increased ~21.9% year over year, resulting from the implementation of AASB 16 ‘Leases’. The company has exhibited strength in changing market conditions and outpaced overall market growth in Australia. Revenue was positively impacted due to growth in Virtus cycle activity in Australia, which increased around 2.7% during the period. Moreover, robust performance by The Fertility Centre (TFC) and progress in Virtus’ Victorian and Queensland cycle activity were key positives during the period.

The company expects to grow premium service volume in FY20 and beyond. VRT remains on track to grow its low-price service volume and diagnostic revenue in Australia along with higher non-IVF day hospital revenue. It also aims to grow International revenue in existing locations and is focused on cost-cutting initiatives. Higher investments in scientific research and new technologies including Artificial Intelligence helps the company to deliver improved patient experience.

VRT is investing in new technologies and scientific research to enhance profitability through cost reduction initiatives. Growth bolstered as the company is developing its international revenue, on the heels of organic activities and acquisition synergies in international markets. Additionally, VRT’s diversified and vertically integrated model is likely to facilitate business development opportunities and growth. The below picture depicts the revenue and EBITDA performance over the period covering 1HFY16 – 1HFY20.

.png)

Growth in Revenue & EBITDA (Source: Company Reports)

1HFY20 Financial Performance: During the period, revenue came in at $142 million, increasing 1% year over year. EBITDA for the year stood at $39.5 million, increasing ~21.9% year over year. Notably, revenues from international operations grew to 21% of group revenue. EBIT for the period came in at $26.9 million, up from $25.8 million reported in 1HFY19. The company’s net profit after tax (NPAT) came in at $15.5 million, an increase of 3.7% year over year. NPAT was primarily impacted by CEO transition and recruitment costs. Diluted earnings per share for the period came in at 18.48 cents, as compared to 18.1 cents in 1HFY19. The company declared an interim dividend of 12 cents per share (fully franked) in 1HFY20, payable on 16 April 2020.

.png)

1HFY20 Results (Source: Company Reports)

Strong Growth in Australian Operations Fertility: The company’s overall IVF cycle activity in Australia’s Assisted Reproductive Services during 1HFY20 increased 2.7% year over year and came in at 8,302 cycles. Virtus TFCs low price cycles represented 22% of overall Virtus Australian activity, as compared to 17.3% in 1HFY19. Virtus TFCs delivered improved performance across all states. Average number of cycles per fertility specialist in 1HFY20 grew by 6.6% on a year over year basis. Australian segment EBITDA margin in 1HFY20 came in at 29.9%, almost flat year over year.

.png)

Virtus Cycle Analysis (Source: Company Reports)

Sneak Peek at Australian Segment Overall Performance: During the year, revenue from the Australian segment stood at $112.8 million, up marginally (0.3%) year over year. Growth in Queensland and Victorian premium service volumes was partially offset by a decline in Premium service volumes in New South Wales and TAS. Revenue from non-IVF procedures increased 6.8% year over year, as the company takes business development initiatives to increase volumes at newly commissioned facilities. On the international front, the company saw revenue from the Irish operations to be flat year over year, that came in at €10.5m, primarily due to lower cycle volumes following the increase in frozen cycles. In the UK, the company’s revenues increased by 13.4% on pcp, due to robust donor activity and value add NHS outpatient activities. Volumes and EBITDA from the Singapore operations continued to grow during the period. Revenue from Singapore operations was up 13.5% year over year. Danish operations witnessed a challenging environment due to reduction in cycles from Sweden.

.png)

Australian Segment Details (Source: Company Reports)

Balance Sheet & Cash Flow Position: At the end of the period, the company reported a cash balance of $12.6 million. The company’s total borrowings at the end of the period came in at $170.9 million, down from $173.7 million as at 30 June 2019. The gearing ratio was 2.8 times adjusted group EBITDA. Operating cash inflow in 1HFY20 came in at $23.6 million as compared to $15.1 million in 1HFY19. Free cash inflow after dividends stood at $5.5 million, as compared to a negative free cash of $3.5 million in the previous year.

.png)

Cash Flow Details (Source: Company Reports)

The company has around 43 Assisted Reproductive Services fertility clinics worldwide, with around 63 laboratories for specialised diagnostic services. In connection to IVF and non-IVF procedures, the company has around 7 days hospitals. With this network of care, the company remains focused to improve the scope of testing and capacity for future growth prospects. The company also remains on track to scientifically evaluate advanced technologies for non-invasive PGT. Further, the company is taking necessary measures to recruit specialists to assist in diagnostics growth. In addition, the company is focused on developing its business to increase internal and external specialist referrals.

With the above scenario in place, the company is confident about retaining its existing customer base and expects to maintain dominant growth momentum in FY20.

.png)

VRT Network of Care (Source: Company Reports)

Recent Update:

(a) In a recent update on ASX, the company announced about the appointment of Ms Kate Munnings as VRT’s Group Chief Executive Officer, effective from 4 May 2020.

(b) Recently, the company informed the market that Challenger Limited has ceased to be a substantial holder of the company, effective from 20 January 2020.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 47.27% of the total shareholding. Allan Gray Australia Pty Ltd is the entity holding maximum shares in the company at 10.77%. Dimensional Fund Advisors, Ltd. is the second-largest shareholder, with a holding of 5.3%.

.png)

Top Ten Shareholders (Source: Thomson Reuters)

Key Metrics: In 1HFY20, the company had a gross margin and EBITDA margin of 72.6% and 26.1%, which is substantially higher than the industry median of 36.7% and 9%, respectively, representing decent fundamentals. Net margin of the company was reported at 10.9%, higher than the industry median of 3.4%. .png)

Key Metrics (Source: Thomson Reuters)

Outlook: Artificial intelligence or AI has been a booming accomplishment in healthcare. Outpatient companies choose bots and automated techniques for controlling and managing health information. With the support of AI, hospitals will accomplish better outcomes, while patients will receive more effective and differentiated care. Virtus commercialises “Ivy” AI technology. It is also expanding its R&D activities into new spheres in the health care industry wherein AI can additionally improve and enhance patient’s outcomes on a global basis.

In the recent times, the industry has started consolidating through mergers and acquisitions mainly due to the difficulties of healthcare reforms. The move has aided the players in establishing operational efficiencies, and financial value for their business. VRT is aiming for potential acquisition opportunities across key international markets to increase international revenue and operating performance.

Furthermore, for FY20 and beyond, VRT expects to grow premium service volume and remains on track to grow its low-price service volume and diagnostics revenue in Australia. Moreover, higher non-IVF day hospital revenue in Australia will eventually aid the company in strengthening its foothold in the space. It also aims to grow International revenue in existing locations, while pursuing its cost-cutting initiatives.

Key Valuation Metrics (Source: Thomson Reuters)

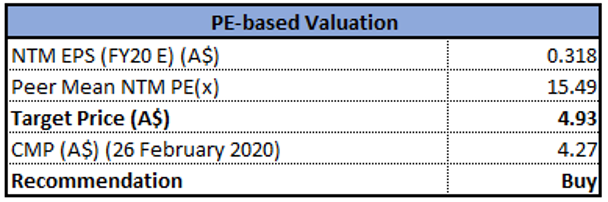

Valuation Methodology: Price to Earnings Based Relative Valuation

Price to Earnings Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company is currently trading below to the average of its 52-week trading range of $3.810 - $5.280. In 1HFY20, the company delivered a decent result, driven by the Virtus cycle activity in Australia. As per ASX, the stock of VRT gave a return of ~9% in the past six months with a price to earnings multiple of 12.34x, and an annual dividend yield of 5.43%. The company made substantial investments in infrastructure, people, and technology. Considering the decent performance in 1HFY20, positive outlook, and current trading levels, we have valued the stock using a relative valuation method, i.e., Price to Earnings multiple, and for the purpose, we have taken the peer group - Monash IVF Group Ltd (ASX: MVF), Japara Healthcare Ltd (ASX: JHC) and Estia Health Ltd (ASX: EHE). As a result, we have arrived at a target price depicting an upside of lower double-digit (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $4.27, down 3.394% on 26 February 2020.

.png)

VRT Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...