Company Overview - Village Roadshow Limited is engaged in media and entertainment businesses. The principal activities of the Company are theme park and water park operations, cinema exhibition operations, and film and digital versatile disc (DVD) distribution operations. The Company's segments include theme parks, cinema exhibition, film distribution and other. The Company's theme parks segment is engaged in themepark and water park operations. The Company's cinema exhibition segment is engaged in cinema exhibition operations. The Company's film distribution segment is engaged in film and DVD distribution operations. In addition, the Company has an equity interest in Village Roadshow Entertainment Group Limited, which is engaged in film production activities. The Company's other investments include investments in digital businesses, as well as corporate overheads and financing activities.

.png)

VRL Details

Lower than estimated FY 16 Financial Performance: Village Roadshow Ltd (ASX: VRL) posted an attributable net profit after tax before material items and discontinued operations of $50.9 million in fiscal year of 2016 which has marginally increased on FY15.

The earnings before interest, tax, depreciation and amortization, excluding material items and discontinued operations is $168.8 million, which is up 1.8% from $165.7 million in FY15. On the other hand, VRL delivered a negative free cash flow of $16.6 million in fiscal year of 2016 as compared to $30.3 million in fiscal year of 2015, due to decrease in trade payables and trade receivables which offset the rise in unearned revenues from Theme Park ticket sales.

.png)

Earnings Metrics for FY 16 (Source: Company Reports)

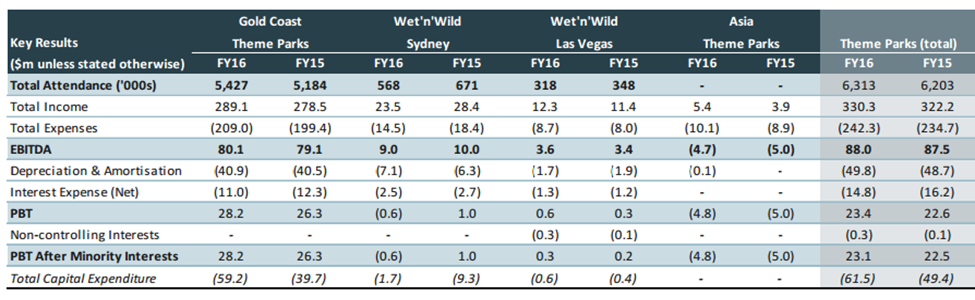

Segments Performance highlights in FY 16: As per the segment’s FY16 performance of VRL, the Theme Parks EBITDA was marginally up, reaching $88.0 million against $87.5 million in prior corresponding period. Moreover, the group is carrying higher deferred revenue into FY17 relative to FY16, largely as a result of the membership program and VIP Pass presales. Meanwhile, the Sea World Resort is the highest occupancy premium hotel of over 90% and the Conference Centre adjacent to Sea World Resort added a new dimension to the business and has exceeded expectations. Moreover, Cinema Exhibition has posted a fifth consecutive full year EBITDA of $82.0 million with increased average ticket price and spend per person. Additionally, despite solid titles such as Mad Max: Fury Road, Oddball and Game of Thrones Season 5, the film distribution division suffered from a weak overall product slate and low margin titles leading to an FY16 EBITDA of $24.5 million. In FY16, the roadshow undertook a restructure to reduce overheads, savings are expected to take effect in FY17. In addition, the

Marketing Solutions division worked with the leading global brands to sell more product, acquire more customers and retain business. The group is constantly making efforts to enhance the division portfolio of complementary products and services to meet current clients’ promotional needs, winning more business from present accounts whilst also opening up new opportunities.

Theme parks fiscal year of 2016 performance (Source: Company Reports)

Other segments’ highlights: VRL has completed renewal of its film financing facilities for USD775 million until 2021. VRL theme parks (VRTP) is in the final stages of design and planning to bring Topgolf, a global leader in sports entertainment, to Australia. The work is underway on the Gold Coast to utilize some of the vacant land and diversify VRTP’s offering. The Village Cube (previously “Big Box”) concept is under development and the discussions advance to roll out in China. The consultation and management agreements offer attractive fee opportunities without the burden of a capital commitment and two such agreements are already in place in Asia. There is considerable development and investigation on other opportunities in Asia with announcements anticipated during the latter part of CY16.

Moreover, VRL has signed deals and the work is underway on major cinema complexes in new growth corridor areas. The Singapore Circuit is expanding with an eight screen site at the SingPost Centre at Paya Lebar due to open in CY17. iPic Theaters is developing its portfolio of market leading cinema and dining with the Fort Lee, New Jersey site opening scheduled for early August 2016 and two additional sites are underway in New York (one expected to open in FY17).

Singapore Circuit (Source: Company Reports)

Additionally, 31% owned Film Nation has two upcoming de-risked titles (The Founder and Arrival), with diverse development including a number of other titles in various stages of pre-production. This is formed in conjunction with John and Dan Edwards, Roadshow Rough Diamond which would create original long-form television and local feature film content for domestic and international audiences from FY17. The roadshow is currently developing a number of feature films that would be announced imminently. In addition, VREG has an opportunity for significant growth and has been building towards shifting the emphasis to global brands and franchises. Marketing Solutions is capitalizing on a broad range of complementary solutions to meet the evolving needs of clients, including advanced financial products and digital rewards, unique promotional insurance solutions, promotional merchandise and marketing platforms. The division has re-signed a number of key clients in Australia and UK that will provide a solid base for growth within existing accounts.

The division has also recently increased its sales force and account management teams to meet the growing demand for the division’s unique suite of marketing and promotional services. Having spent the final few months of FY16, the division is expecting to capitalize on this investment in FY17.

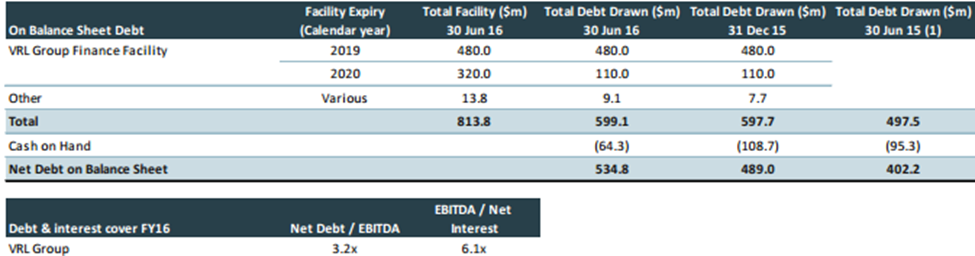

Investments based Growth: VRL has significant opportunities for future earnings growth. The capital investment in Marketing Solutions, VREG and iPic has resulted in an increase in FY16 while Net Debt/EBITDA reached 3.2x, which should reduce as these investments mature. The additional investments for other growth opportunities such as Topgolf planned in the near to mid-term would continue to result in a temporary increase in VRL’s leverage until earnings from developments are realised.

VRL expects that leverage will return to below 3.0x EBITDA as these investments begin to generate earnings.

Debt Position as of June 2016 (Source: Company Reports)

Remuneration arrangements: VRL has implemented changes to the remuneration framework beginning from FY17 to ensure clearer alignment of executive interests with those of shareholders. Moreover, the group has announced a fully-franked final dividend of 14 cents per share, with a record date in September 2016 and payable October 2016.

Moreover, the Directors would consider a special dividend of 10 cps in the future, subject to appropriate leverage, available franking credits, capital commitments and business conditions at the time.

Market opportunity for VRL:The worldwide industry for film and television has never been stronger before and the two fundamental growth drivers are China and the growing quality of long form television content available on traditional multi-channel networks as well as over the top streaming services such as Netflix and Amazon. The group has delivered a solid result for Singapore Cinema Exhibition in fiscal year of 2016, and has over 43.7% market share in the Singapore circuit. Moreover, the average ticket price and spend per person is increasing in the region while Tiong Bahru reopened five screens in May 2016.

Stock Performance:Meanwhile, VRL stock has fallen 8.2% in the last five days alone (as of August 26, 2016) as the group came out with lower than estimated results; and with the pressure this year, the stock fell over 34.6% during this year to date. On the other hand, the group is making efforts to revamp the growth track despite the ongoing volatility in its target markets. In FY 16 results, VRL has reported growth for fifth consecutive year of the Cinema Exhibition division, growth from the Gold Coast Theme Parks and the inclusion of approximately six months of Opia in the Marketing Solutions division. These results have offset disappointment at Wet’n’Wild Sydney and the Film Distribution division. VRL cash flows might improve in the coming months and the company is even considering to give special dividends in the future along with growth initiative among all the divisions giving strong future visibility.

The stock is having a decent dividend yield. We recommend investors to leverage the fall in the stock as a buying opportunity as the stock is now available at reasonable valuations. Accordingly, we give a “Buy” recommendation on the stock at the current price of $4.76

VRL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...