Company Overview - Veda Group Limited (Veda) is a data analytics company and the provider of credit information and analysis in Australia and New Zealand. Veda operates four business lines: Consumer Risk & Identity, Commercial Risk & Information Services, B2C & Marketing Services, and International. Consumer Risk & Identity includes data intelligence about individuals to enable business customers to make consumer credit risk decisions, validate identity, avoid fraud and manage risk. Commercial Risk & Information Services include data intelligence and third party data about businesses and the people behind them to enable business customers to assess commercial credit risk, verify entities and manage supplier risk. B2C & Marketing Services include an online offering allowing consumers access to their personal credit information and associated analytical tools. International includes New Zealand offering of consumer and commercial credit bureau and commercial and property solutions.

Analysis - Credit reporting agency Veda has a near monopoly in the Australian consumer risk segment and is the largest in the commercial segment in Australia. The introduction of comprehensive reporting provides an earnings tailwind as it increases the attractiveness of the product offering, but Veda’s value proposition must be attractive to customers in order to thwart large ambitious new entrants. A large data pool and entrenched customer relationships, which create a network effect and customer switching costs, strengthen Veda’s position. Customers will welcome competition to encourage ongoing product development and ensure quality is not compromised. However large credit bureaus have been subject to competition in other countries for years and in most oligopolistic markets the main players continue to make attractive returns.

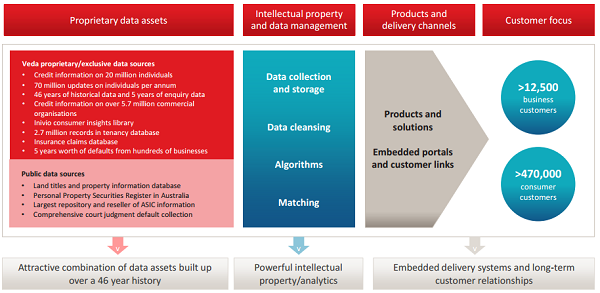

Business Model (Source - Company Reports)

Business Model (Source - Company Reports)

The transition from negative only to comprehensive credit reporting provides a significant earnings tailwind for Veda as sales volume through both business and consumer channels gradually increase. Armed with additional information lenders can use risk based pricing and proactively monitor changes in a customer’s financial position. The onus is on consumers to be aware of their report and score and for the first time makes credit reports important to the masses.

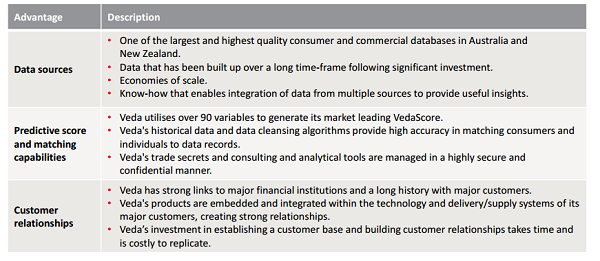

Competitve Advantages (Source - Company Reports)

Competitve Advantages (Source - Company Reports)

Although a key driver Veda’s earnings growth is not bound solely to credit volumes. Growth is also underpinned by: opportunities to continue to penetrate non-bank markets such as law and accounting firms; growth in the use of its online identification services; increased use of its data and analytics to help firms build marketing strategies; access to additional government data enabling new products and selling more products to existing customers. Major international bureaus have operated within competitive environments for years and all continue to earn attractive returns. We expect potential pricing pressures stemming from increased competition will be too minor to hurt Veda’s competitive strengths in the medium term.

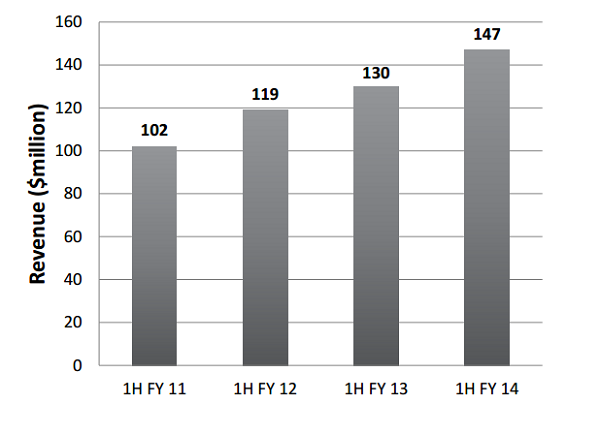

VEDA Revenue (Source - Company Reports)

VEDA Revenue (Source - Company Reports)

We take a more optimistic view of the flow on impact of comprehensive reporting on increased demand from consumers to directly purchase credit reports. The potential for lenders to move to pricing loans based on an individual’s credit rating incentivises consumers to maintain awareness of their credit score. Our assumptions imply Veda’s revenue from selling consumer reports reaches a quarter of the size of its credit revenue in 10 years or 10% of group revenue. Experian (EXPN) listed on the London Stock Exchange which is an international bureau operating in 40 countries. It’s North American division makes almost as much revenue from consumer services as it does from credit services and forms 20% of the firm’s USD 4.7 billion revenues.

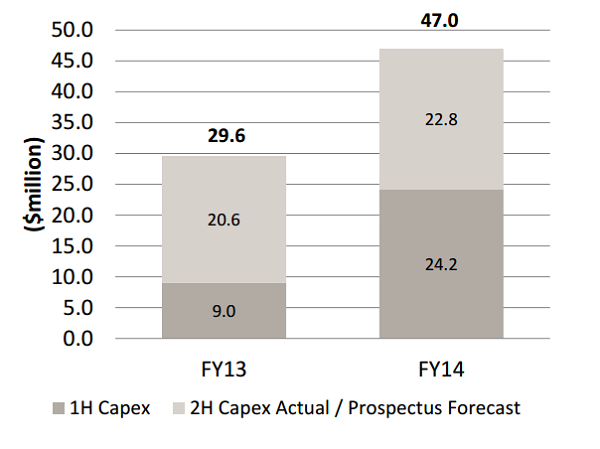

VEDA Capital Expenditure (Source - company Repeorts)

VEDA Capital Expenditure (Source - company Repeorts)

Including market share leakage to Experian in the consumer risk division, we assume average revenue growth of 9% during the next 10 years. We expect Veda to maintain revenue growth ahead of system credit growth. While total credit growth averaged 3.5% per year in the past 2 years, Veda achieved 7% growth per annum from existing products, emphasizing its ability to raise the value and in turn price of its products, penetrate underrepresented markets and cross sell additional information. For example access to the Personal Properties Securities Register (which records interests attached to assets such as motor vehicles, boats, machinery, shares and personal assets) and the launch of Property Exchange of Australia (online exchange of property ownership) increases exposure to law and accounting firms and adds another product offering to existing bank customers. A track record of data integrity permits Veda access to such data. Strong cash flow generation and an initial dividend payout ratio set as between 40% and 60% of net income leaves ample funds to fulfil the growth initiatives.

VEDA Daily Chart (Source - Company Reports)

VEDA Daily Chart (Source - Company Reports)

Coinciding with the introduction of comprehensive reporting is the entrance of a new competitor in the consumer credit industry in Australia. Experian with the financial backing of six large financial institutions (Commonwealth Bank, Westpac, ANZ Bank, National Australia Bank Citigroup and GE Capital) enters the current consumer credit bureau duopoly occupied by Veda and Dun and Bradstreet. We believe the investment by banks in Experian’s Australian foray aims to ensure healthy competition and to protect them from being on the receiving end of unjustified price hikes. It also implies dissatisfaction with Dun and Bradstreet as a respectable alternative to Veda. While Dun and Bradstreet’s market share is quoted to be about 15% by market research firm IBISWorld, we understand the banks use Veda on every credit check with Dun and Bradstreet used as a secondary report if required.

Data is the foundation of all Veda’s business lines. With collected and externally purchased data, Veda helps verify identities and asses the credit worthiness of individuals and businesses. Veda achieved steady growth during the past decade not exclusively related to credit application volumes. A compound annual growth rate of 8% in revenue during the past 10 years was underpinned by success in developing new products which leverages its pool of data and increase exposure to additional industries. Veda has also made a number of acquisitions which increase market share in a segment, bring additional technology and present cross selling opportunities.

Since listing on the Australian Securities Exchange or ASX in December 2013, Veda has reported first half results in line with expectations and has confirmed full year earning’s guidance and the share price has now doubled. Pacific Equity Partners or PEP’s decision to retain 64% ownership share of the business resulted in Australian fund managers and high net worth individual getting a small or zero allocation in the IPO and there was no general public offer. This undoubtedly created buying pressure and support for the share price. Inclusion in the S&P ASX 200 compounds the upward price pressure as index based funds or funds allowed to invest in top 200 stocks add to the demand.

Veda is the primary credit bureau in Australia and New Zealand. However most parts of Veda’s business are contested by one or more competitors including Dun & Bradstreet, Experian, SAI Global, Global X and CITEC Confirm. The industry has material practical barriers to entry. These include the substantial data reserves and the software embedded in most credit risk processes and decisioning tools. The industry also exhibits scale and network benefits from having a single or dominant player. We believe that due to comprehensive reporting the level of bureau enquiries could materially increase mainly driven by periodic account reviews. World Bank data suggests that the level of bureau enquiries are 90% higher in comprehensive reporting markets relative negative only markets. In addition B2C enquiries and reports are a substantially larger contributor in the UK and the US to the Experian’s revenues (20% vs 8% for Veda). With increased awareness of comprehensive reporting we would expect this business to grow rapidly. We put a

BUY recommendation on the stock at the current price of $2.00.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...