Kalkine has a fully transformed New Avatar.

Company Overview: Treasury Wine Estates Limited is engaged in grape growing and sourcing; wine production, and wine marketing, selling and distribution. The Company's segments include Australia and New Zealand (ANZ), which is engaged in the manufacture, sale and marketing of wine within Australia and New Zealand, and distribution of beer and cider under license in New Zealand; Americas, which is engaged in the manufacture, sale and marketing of wine within the Americas region; Asia, which is engaged in the sale and marketing of wine within the Asia (including the Middle East and Africa), and Europe, which is engaged in the manufacture, sale and marketing of wine within Europe and Latin America. It is also engaged in the sale of branded wines, principally as a finished, bottle product. The Company's wine portfolio includes Commercial, Masstige and luxury wine brands, such as Penfolds, Beringer, Lindeman's, Wolf Blass, Stag's Leap, Chateau St Jean, Beaulieu Vineyard and Sterling Vineyards.

TWE Details

Decent Performance in 1HFY19: Treasury Wine Estates Limited (ASX: TWE) is one of the largest wine companies across the world with the market capitalisation of circa $10.85 Bn as of 27 May 2019. The company posted its half-year results to December 2018 wherein Net Sales Revenue (NSR) stood at $1,507.7 million, showing a decent rise of 16% on PCP basis. However, on a constant currency basis, it reflects a rise of 13% which implies the strongest organic growth rate in the history of the company. The company’s EBITS growth was delivered across the regions via top line execution supported by volume growth, portfolio premiumisation, and price realisation. The company witnessed robust performance with respect to Asia region wherein EBITS stood at $153.1 Mn in 1HFY19, showing strong growth of 31% on PCP basis. Resultantly, EBITS margin for Asia region came in at 38.9%. It was mainly driven by the competitive advantaged business model, brand portfolio, and outstanding sales execution during the same period. TWE possesses a flexible and efficient balance sheet which might help it in supporting the company’s growth prospects moving forward. The company stated that key top-line and profitability metrics are reflecting continued positive momentum. The cash conversion of 53.5%, reflects growth in the top-line growth, timing of sales execution, as well as currency. The company’s net debt to EBITDAS (Earnings before interest, tax, depreciation, amortisation, material items & SGARA) stood at 2.0x and its interest cover was 13.9x and, at the same time, TWE managed to maintain investment grade credit profile. Moving forward, it can be assumed that the company’s performance would be sensitive to trade relations between the US and China. The trade battle can affect the Australian companies which are having business operations in China. However, disciplined capital management, decent balance sheet position, lesser dependency on debt with respect to funding the asset base (as can be seen from 1H FY 2019 Assets/Equity ratio) and sound liquidity position are expected to act as tailwinds for the company.

.png)

Key Measures of Performance (Source: Company Reports)

Top 10 Shareholders: The following table provides a broad overview of the shareholding pattern of Treasury Wine Estates Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Better Key Margins Strengthen the Confidence: Treasury Wine Estates is having a decent standing with respect to its key margins as its net margin stood at 14.3% in 1H FY 2019 which implies a rise of 1.9% on YoY basis that reflects the company is possessing strong capabilities to convert its top line into bottom line. TWE’s gross margin stood at 41.9% which implies a rise of 1.1% on YoY basis. The company’s current ratio stood at 2.55x which implies a rise of 5.6% on the YoY basis that reflects that the company is in the improved position to address its short-term obligations and it has sufficient headroom to make deployments towards growth. The company’s assets/equity ratio stood at 1.62x in 1H FY 2019 which is lower than the industry median of 2.80x and, therefore, it looks like that the company’s assets are largely being funded by equity.

.png)

Key Metrics (Source: Thomson Reuters)

Asia Depletions & Australian Vintage Update: TWE recently reiterated the caution against using Wine Australia export data for the quarter ended March 2019 as a direct read through to TWE’s trading performance. The usage of the short term trade export and import data could be misleading with regards to the company’s underlying trading performance in Asia region as it does not consider primary structural differences in TWE’s business model, the premium mix of its portfolio, nor variability in export shipment profile. With respect to China, the company stated that following the establishment of TWE’s Shanghai warehouse in 1H of fiscal 2018, selected trade export and import data points do not have a direct relationship to the company’s sales performance.

The company also threw light on its operating performance across all the regions for nine months to March 2019 and it confirmed positive momentum with respect to Asia with record depletions delivered for nine months to March 2019, including the robust trading performance throughout the key Chinese New Year festive period. The company also confirmed expectations which were communicated in the month of February 2019 that Vintage 2019 in Australia happens to be a very strong and high-quality Luxury wine vintage for the company. The Luxury intake increased around 10% on Vintage 2018 because of multi-regional sourcing strategy.

Overview of TWE’s Americas Segment: With respect to the Americas region, TWE stated that the US route-to-market changes is on-track and progressing well. The improvement in the portfolio mix has been supporting top-line revenue and growth of NSR per case. In 1H FY 2019, the Americas region NSR stood at A$604.6 million which implies a rise of 20% (Y-o-Y) on a reported currency basis. Its EBITS amounted to $112.1 million in 1H FY 2019 reflecting a rise of 11.7% on a reported currency basis. There are expectations that transitional costs would be removed from 2H FY 2019 and returns to margin accretion is expected from FY20 onwards.

.png)

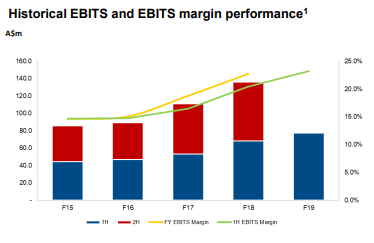

Historical EBITS and EBITS margin performance (Source: Company Reports)

Growth Rate In Asia In 2H FY19 Expected To Be Marginally Ahead Of 1H FY19: TWE’s Asia region posted NSR amounting to $393.8 million in 1H FY 2019 which implies a rise of 32.4% on the YoY basis on reported currency basis while, during the same period, its EBITS amounted to 153.1 million reflecting 30.9% rise. The business model, richer portfolio mix, and outstanding sales execution have been supporting growth in top-line as well as earnings.

.png)

Asia Region (Source: Company Reports)

The sales channels are in good position throughout the Asia region and the higher cost of doing business (CODB) implies early deployment to help the future growth, including the investment towards new brands, people as well as a business model.

Robust Trading Performance Witnessed in Europe Region: TWE’s Europe region posted NSR amounting to $175.6 million in 1H FY 2019 which reflects a rise of 9.6% on a reported currency basis. The company stated that the region’s NSR was supported by robust trading performance throughout key regional markets alongside Masstige-led mix improvement.

.png)

Europe Region (Source: Company Reports)

Analysing TWE’s Australia and New Zealand Region: On Australia and New Zealand region front, net sale revenue (NSR) stood at $333.7 Mn in 1HFY19 which is broadly in-line as compared to the prior corresponding period. However, EBITS margin for the ANZ region expanded by 280 bps to 23.2% in 1HFY19 against 1HFY18. It was mainly supported by the improvement in COGS per case and CODB during the same period. Additionally, the company has been targeting 25% volume and value market share in Australia and the current value market share happens to be 22%.

Australia and New Zealand (Source: Company Reports)

What To Expect From TWE Moving Forward: TWE is having the people, the brands as well as the business models in order to maintain the competitive advantage with respect to all the markets. The growth prospects in Asia are attractive and there are expectations that expanding distribution and growing market share with regards to imported wine category would be supporting the future prospects. The macro-economic uncertainty had created challenges for some of the global consumer companies, however, the strength of TWE’s routes-to-market, particularly in the key markets like China and the US, had provided the company with a significant competitive advantage.

With regards to China, the company stated that there is significant opportunity to continue growing the share of the imported wine market from the current sub 5% level by leveraging the brands as well as multiple countries of origin portfolio. It can be said that the performance of TWE is sensitive to the broader performance of the economy in China. As the market players are aware, the US and China trade battle is a crucial metric when it comes to analysing the performance of the Chinese economy. A rise in the trade battle between them could impact the global business environment and the operations of the Australian companies which are having businesses in China.

Treasury Wine Estates would be aiming to build on existing French country of origin proposition, Maison de Grand Esprit, using Penfolds as well as Beaulieu Vineyard brands. The company has reiterated the guidance for reported EBITS growth of around 25% for FY 2019, and between around 15%- 20% for FY 2020.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methods: Based on few exemplary methods, we have obtained a range of stock price upside as indicated in below tables:

Method 1: PE- Based Valuation

PE- Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Method 2: Price-to-Book Value Approach (NTM)

.PNG)

Price-to-Book value-based valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of Treasury Wine Estates had delivered a decent return of 6.49% in the span of the previous six months while, on the YTD basis, the returns stood at 2.79%. The company has continued focus on delivering the returns to the shareholders in a disciplined and sustainable manner which might attract the attention of market players moving forward. Based on the 1HFY19 performance, the Board of Directors declared a fully franked interim dividend of 18.0 cents per share, representing a dividend rise of 20% as compared to the previous corresponding period. It equates a dividend pay-out ratio of 58% of NPAT which is within the company’s target range of 55-70%. Besides this, the company’s flexibility has been enhanced because of the strengthened financing structure. The inventory composition has been reflecting premiumisation which is supporting the earnings and margin growth in FY 2020 and beyond. The company is expecting FY 2019 cash conversion of between 60%- 70% and cash conversion target of 80% is appropriate over the long term. By looking at decent growth in the long run, we have valued the stock using the two Relative valuation methods, P/E and Price-to-Book Value and have arrived at target price upside in the ambit of $15.8 to $16.4 (single-digit upside (in %)). Given the backdrop of the aforesaid facts and current trading level, we give a “Buy” recommendation on the stock at the current market price of $15.120 per share (up 0.199% on 27 May 2019).

TWE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...