Kalkine has a fully transformed New Avatar.

Company Overview: Treasury Wine Estates Limited is engaged in grape growing and sourcing; wine production, and wine marketing, selling and distribution. The Company's segments include Australia and New Zealand (ANZ), which is engaged in the manufacture, sale and marketing of wine within Australia and New Zealand, and distribution of beer and cider under license in New Zealand; Americas, which is engaged in the manufacture, sale and marketing of wine within the Americas region; Asia, which is engaged in the sale and marketing of wine within the Asia (including the Middle East and Africa), and Europe, which is engaged in the manufacture, sale and marketing of wine within Europe and Latin America. It is also engaged in the sale of branded wines, principally as a finished, bottle product. The Company's wine portfolio includes Commercial, Masstige and luxury wine brands, such as Penfolds, Beringer, Lindeman's, Wolf Blass, Stag's Leap, Chateau St Jean, Beaulieu Vineyard and Sterling Vineyards.

.png)

TWE Details

Robust Organic Growth in 1HFY19: Treasury Wine Estates Limited’s (ASX: TWE) principal activities consist of production, marketing, and sale of wine. As on April 29, 2019, the market capitalisation of TWE stood at $12.35 billion. With respect to China, the company has been targeting to expand the city distribution coverage by more than 50% in the span of the next three years with higher allocations of luxury wine. With respect to the US operating model, the company stated that dedicated sales and merchandising teams happen to be in place, and they are driving improved execution.

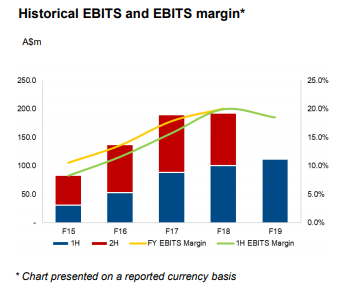

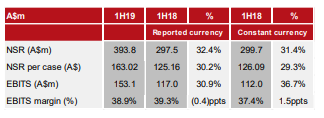

The company witnessed NSR (or Net Sales Revenues) of $1,507.7 million in 1HFY19 which reflects a rise of 16.4% on reported currency basis and 12.7% on a constant currency basis on the prior comparative period. The company’s earnings before interest, tax, SGARA, and material items amounted to $338.3 million reflecting a rise of 19.4% on a reported currency basis. However, on a constant currency basis, TWE’s EBITS rose by 17.8%. All the regions managed to deliver EBITS growth in 1H FY 2019. The company stated that the execution of the US route-to-market transition is ramping up well and is on track. Coming to the regional performance, the company’s Asia region delivered robust, sustainable growth which was enabled by its business model which is having competitive advantages. However, its brand portfolio and strong sales execution were also the factors which aided. The company’s ANZ and Europe regions witnessed positive momentum and were supported by Masstige-led premiumisation and collaborative customer partnerships. Cash conversion stood at 53.5% which mainly reflects revenues growth and timing of the execution of sales in Americas and Asia in 1H FY 2019, along with the foreign exchange translation of working capital balances in the US. The macro-economic uncertainty created challenges for some global consumer companies, however, TWE’s routes-to-market strength, primarily in key markets like China and the US, provided the company with a competitive advantage.

.png)

Net Sales Revenue (Source: Company Reports)

TWE Possesses Decent Position in Key Margins: Treasury Wine Estates Limited is having a decent position with respect to its key margins as its net margin stood at 14.3% in 1H FY 2019 which is higher than the industry median of 12.2%. This reflects that the company is having better capability to convert its top line into the bottom line as compared to its peers. TWE’s EBITDA margin stood at 23.8% as compared to the industry median of 22.1%. The company recorded top-line growth at CAGR of 15.3 per cent over 1HFY15-19 while bottom line recorded a CAGR growth of 59.7 per cent over the same period. Also, Treasury Wine Estates is having strong cash-generation capabilities which are evident from the growth levels of its cash receipts. We expect that strong cash generation capabilities would be able to improve its liquidity position which might help in making deployments towards its business objectives.

NSR in Americas Region Rose by 12.5%: Treasury Wine Estates Limited’s Americas region generated NSR of A$604.6 million which reflects a rise of 12.5% (Y-o-Y) on a constant currency basis on the back of increased volumes supported by positive execution under new route-to-market model, and 10.4% rise in the NSR per case, which was led by volume growth in Luxury and Masstige segments, and overall benefits from route-to-market changes in the US. The company stated that Canada has been performing strongly with the help of a partnership with Mark Anthony Wine & Spirits and LATAM EBITS was higher and strong customer relationships are driving growth throughout all the price segments. The company has been maintaining its focus towards growing Luxury and Masstige portfolios, and it exited lower margin commercial volumes in the previous years, ahead of the other market players. Margin accretions expected from FY20 onwards.

Americas Region (Source: Company Reports)

Analysing TWE’s Asia Region’s Performance: Treasury Wine Estates Limited’s Asia region witnessed robust NSR growth which was because of increased availability of Luxury and Masstige wine and strong sales execution. The growth in volumes reflects a more balanced sales profile of Rawson’s Retreat volumes and exit of lower margin commercial volumes in SEAMEA in 1Q FY 2019. However, a rise in the NSR per case demonstrates mix improvement, price realisation within Luxury and Masstige segments, and new Luxury product launches. The Asia region witnessed NSR amounting to A$393.8 million in 1H FY 2019 which reflects a rise of 32.4% on 1H FY 2018 on reported currency basis and a YoY increase of 31.4% on a constant currency basis. The company stated that the fundamentals of the Asian wine market is attractive and there has been growth in the imported wine category. The company has been seeing a substantial opportunity to grow the market share from the current sub 5% level with the help of its multiple countries of origin portfolio.

Asia Region (Source: Company Reports)

Volume and NSR per case Growth Supported Europe’s NSR: Treasury Wine Estates Limited’s Europe region generated NSR of A$175.6 million which reflects a YoY rise of 5% on the constant currency basis. This rise was because of volume growth throughout key regional markets as well as NSR per case growth of 3.6%, driven mainly because of Masstige-led mix improvement. The region’s EBITS rose by 4.8% and stood at $26.3 million and the EBITS margin was flat. The company also added that UK wine market conditions are challenging and there has been a decline in overall volumes. However, Australian wine is performing ahead of the market. The strengthened partnerships of the company with key European retailers have been driving the improved distribution of priority brands. TWE has been focusing on joint business planning and increasing share of shelf space.

Europe Region (Source: Company Reports)

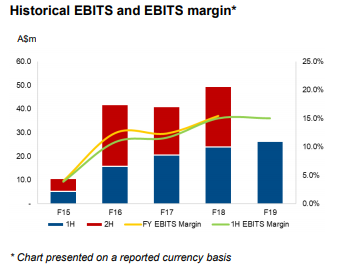

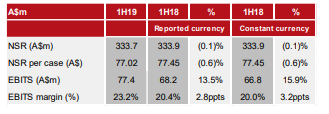

A Look at TWE’s ANZ Region: Treasury Wine Estates Limited’s ANZ region witnessed NSR amounting to $333.7 million in 1H FY 2019 which reflects a marginal fall of 0.1% on YoY basis. An improvement in the cost of doing business (CODB) demonstrates ongoing focus and a discipline approach around cost management. The company has been targeting 25% volume and value market share in Australia on the back of deployments towards portfolio growth and innovation within the Masstige segment. Its current value market share stood at 22%.

Australia and New Zealand Region (Source: Company Reports)

Prudent Capital Expenditure Might Support Growth Prospects: In 1H FY 2019, TWE incurred capital expenditure amounting to $93.6 million which consist of capex amounting to $82.0 million towards maintenance & replacement while growth capex stood at $11.6 million. We expect that these capital expenditures place the company in a strong position to tackle the challenges of the broader market and can also support it in witnessing growth moving forward. For FY 2019, the company stated that maintenance and replacement capex is anticipated to be in line with the guidance i.e. between $130 million- $140 million (including oak barrels).

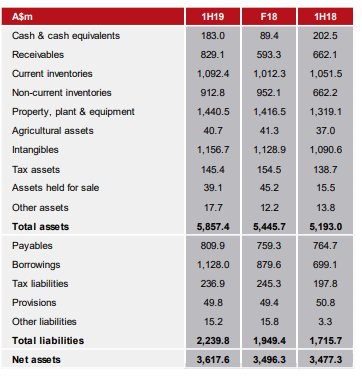

Decent Balance Sheet Position: Treasury Wine Estates Limited’s net assets witnessed the rise of $121.3 million and stood at $3,617.6 million mainly because of a rise in receivables and high-quality Californian vintage which increased inventory. Also, the company’s cash balance is being mainly supported by the earnings growth. However, the impact got offset by the higher dividends, tax paid, working capital investment and capital expenditure. The company’s working capital position in 1H FY 2019 was helped by higher receivables which reflects growth in the revenues and timing of sales execution and by higher payables, driven by business growth and higher brand building investment in Asia and the Americas in order to help Australian, US and French brand portfolios. As of 31 December 2018, the company has a decent cash position i.e., $183.0 Mn with debt-to-equity ratio of 0.31x. The current ratio and quick ratio stood at 2.55x and 1.25x, respectively in 1HFY19, representing adequate liquidity to fulfill any shortcoming liability in near future.

Balance Sheet (Condensed) (Source: Company Reports)

What To Expect From TWE Moving Forward: Treasury Wine Estates Limited made an entry to FY 2019 with higher luxury wine availability, robust pipeline of innovation and new product development, strengthening customer partnerships in all the regions and brand portfolio initiatives that have the potential to be incremental to existing 5-year expectations. The company reiterated the guidance of around 25% growth in EBITS in FY 2019 and anticipates reported EBITS growth for FY 20 to be between ~15% to 20%, which is broadly in line with the consensus. TWE would be providing a further update on expectations for FY 20 at the time of full-year results released in the month of August 2019.

The management of TWE stated that brands, the people and the business models are in place to maintain the momentum of the half and continue delivering sustainable growth for the shareholders. We expect that the company’s strong cash generation capabilities and decent balance sheet position might help it in achieving respectable growth levels moving forward.

.PNG)

Key Metrics (Source: Company Reports and Thomson Reuters), *LTM – Last Twelve Months

Stock Recommendation: The stock of Treasury Wine Estates Limited delivered a decent return of 15% in the past one month, while in the time frame of previous 6 months, the return stood at 14.39%. In 1H FY 2019, the company’s key top-line and profitability metrics have been reflecting continued positive momentum which might attract the attention of market players. The company’s ROCE stood at 13.3% which reflects a rise of 0.7 percentage points in 1H19 and, thus, demonstrates that TWE continues to deliver robust returns while investing in the future growth prospects. The company declared interim dividend amounting to 18.0 cents per share (fully franked) reflecting a rise of 20% on prior year which demonstrates the company is having strong financials. Additionally, TWE is expected to be aided by the US route-to-market transition and strong cash generating capabilities. Also, there are expectations that the company’s flexible and efficient balance sheet would be supporting it in witnessing growth. The company expects cash conversion, for FY 2019, to be between 60%-70%. Over the long-term, the company targets 80% cash conversion. Hence, considering the above-mentioned parameters and decent outlook in the long run, we give a “Buy” recommendation on the stock at the current market price of A$17.110 per share (down 0.349% on 29 April 2019).

.png)

TWE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...