Company Overview: Transurban Group is engaged in the development, financing, operation and maintenance of toll roads networks, as well as management of the associated customer and client relationships. The Company's segments include Victoria (VIC), New South Wales (NSW), Queensland (QLD) and the Greater Washington Area (GWA). Its VIC segment's operations include CityLink operations and development of CityLink TullaWidening and Western Distributor. Its NSW segment's operations include GLIDe tolling system and the development of NorthConnex. Its QLD segment's operations include AirportlinkM7 and the development of Inner City Bypass (ICB), Gateway Upgrade North and Logan Enhancement Project. Its GWA segment's operations include 95 Express Lanes and the development of I-66, I-395 and Southern Extensions to 95 Express Lanes. The Company manages and develops urban toll road networks in Australia and the United States. Its subsidiaries include Transurban Holdings Limited and Transurban Holdings Trust.

TCL Details

Revenue levers in place: Transurban Group (ASX: TCL) is an infrastructure and road operator company that manages and develops urban toll road networks in Australia and North America; with expertise in execution of effective transportation solutions. It holds interest in 14 roads in Australian portfolio, 2 in the US state of Virginia and one in Montreal Canada. TCL sales have grown at CAGR of 30.1% during FY14-18 on the back of increase in toll revenue from existing assets driven by traffic growth and toll price escalation. Going forward, revenue is expected to grow with the huge push in traffic growth across Sydney, Melbourne, Brisbane, and North America regions. The company reported underlying proportional EBITDA margins of 74.9%, a 100 bps improvement Y-o-Y and this was in line with expectations while statuary EBITDA contracted to 540 bps and recorded 50.6% in FY18 against prior year. TCL, after reporting strong growth in FY17 and in FY18, is expected to report strong growth in FY19E onwards at the back of full contribution from A25 and toll revenue growth. However, the company offers a low risk predictable return, with management who has been successful to secure unique growth options thereby we expect the RoE to improve significantly in FY19E onwards. Historically, the stock has been trading at four year average P/E of 75.73x but presently it is trading at 49.34x of FY18 which makes it below the historical average. Hence, we value stock at average P/E 65.73x (10x discounted to four year average) to FY19E EPS (consensus estimates, $0.19) which gives the target price of $12.49, representing an upside of 13.7%.

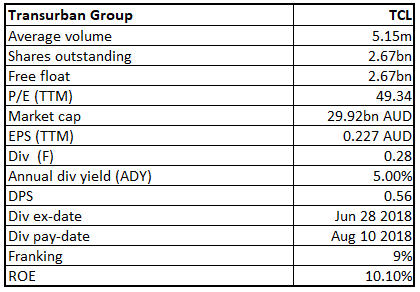

Key Financial Metrics:

.PNG)

(Source: Company Reports, Thomson Reuters), NA - Not Available

What Could Aid Transurban Moving Forward?

Transurban’s approach to tap the investment opportunities in a disciplined manner might prove beneficial for the company. The company’s approach is reflected when it comes over for bidding. The company follows structured process during the valuation approach as well as project selection. The company presently enjoys core capabilities like focusing on the customers, advancements in the technology platform, community engagement as well as its partnerships with the governments. According to the management of Transurban, they also have their core focus on the funding opportunities. The company plans to maintain adequate debt/equity funding so that its credit metrics are taken care of and it witnesses no credit downgrades. In December 2017, the company garnered funds of $1.9 billion via equity entitlement offer. These funds have been deployed towards West Gate Tunnel Project. The company plans to do improvements which could help in decreasing the fees as well as in enhancing the digitized solutions for the customers. In addition, it would also conduct the CAV trials which could help the company in improving the automated vehicles. The management believes that there are ample opportunities which are yet to get tapped in the North America as well as Australia.

.png)

$10 billion committed pipeline (Source: Company Reports)

Transurban Won Bidding for WestConnex – Landscaping Growth Momentum:

On September 10, 2018, Transurban made an announcement that the company was successful in acquiring 51% holding in WestConnex. The company had acquired it from NSW Government at the price of $9.3 billion. With the acquisition, the position of Transurban has strengthened. The company now leads the way globally in regards to delivery, operations, road development as well as Technology Company. Transurban is currently operating significant toll roads and it enjoys network effect which places the company well above the competition. Apart from Australia, the company also plans to target Canada as well as United States. Moreover, TCL’s recent acquisition of WestConnex, which is a 4-stage toll road concession, allowed it to vouch for 25.5% interest at a price of $4.1 billion. The key aspect is that the WCX traffic corridors have been established well and the M4 traffic volumes have also been up. This is expected to drive revenue growth for TCL in the future while cost might be moderate. An internal rate of return in the single digit level might fall in place with completion of roads in subsequent years till FY27. TCL has also funded the issue with new equity in this regard. The group will have project clarity by FY22 while cashflows will be established with the M4 Stage 1A open and stage 2 becoming accessible to traffic. Further growth is expected to come with Stage 3 in FY25 with the Rozelle interchange and FY26 with the opening of Western Harbour Tunnel.

.png)

Potential next generation opportunities (Source: Company Report)

Needle on Key Indicators

1. EBITDA and EBITDA Margin expected to be at higher levels going forward: The Company has recorded EBITDA Y-o-Y growth of 9.1% in FY18 due to increased traffic and toll prices across the Australian and GWA assets and disciplined cost control approach. EBITDA margin contracted to 540 bps and recorded 50.6% in FY18 against 56.0% in FY17 as the same was mainly impacted by the higher construction cost incurred during the year. However, we believe that EBITDA margin would be revamped in the range of 60% - 65% during the period of FY19E-21E due to strong growth in toll revenue from large vehicle toll multipliers and cost optimization strategy.

.png)

EBITDA and EBITDA Margin (Source: Company Reports)

2. Growing PAT and PAT Margin: PAT grew at CAGR of 121.3% during FY16-18. Bottom line is boosted by robust operating income growth during the same year. On the back of operating efficiencies, we expect the bottom line of the company to pick-up.

.png)

PAT and PAT Margin (Source: Company Reports)

3. RoE and RoIC on the Rise: RoE and RoIC substantially improved from 5.0% and 1.0% to 10.1% and 2.3%, respectively, in FY18 over the prior year. Moreover, there has been an incline in both RoE and RoIC over the period of FY14-18. With improved realization from all business segments, improved performances in return on equity and return on invested capital seems to be on the cards.

.png)

ROE and ROIC (Source: Company Reports)

4. Healthy Operating and Free Cash Flow (FCF): FCF has grown at CAGR of 20.7% during FY14-18 on the back of contribution from GWA assets (100% owned), favourable net finance cost, add back transaction & integration costs related to acquisitions, rise in working capital, and decrease in non-100% assets. However, FCF could be benign for short term as the group focuses on TIFIA interest payments and amortisation of the M5 and ED debt as well as scheduled capital releases as pre-agreed with state governments. In the long run, we expect FCF to be strongly backed by continuity in traffic growth and toll price escalation across its networks.

.png)

Operating Cash Flow and Free Cash Flow (Source: Company Reports)

5. Healthy Cash Dividend Payout Ratio: From the past few years, Transurban has been shelling out decent amount of dividends which helped in structuring strong pay-out ratios. In FY 2018, the company recorded significant momentum with regards to the distribution and it also managed to raise $1.9 billion through equity in order to back West Gate Tunnel Project. In FY 2019, the company is expected to shell out approximately 59.0 cents per share in the form of dividends. The company has plans to deliver significant value to the shareholders via dividends. Over the course of time, the company might go for distributing 100% of the FCF (free cash flow) in the form of dividends.

.png)

Total Cash Dividend and Pay-outs (Source: Company Reports)

Stock Recommendation: In last three months, the stock has been down by around 7% and is trading close to its low levels while being in an oversold region. The technical indicators imply a support from the prevailing low levels while resistance can be seen around $12. Historically, the stock has been trading at four year average P/E of 75.73x but presently it is trading at 49.34x of FY18 which makes it below the historical average. Hence, we value stock at average P/E 65.73x (10x discounted to four year average) to FY19E EPS (consensus estimates, $0.19) which gives the target price of $12.49, representing an upside of 13.7%. Given the catalysts in place, we provide a “BUY” recommendation at the current price of $ 10.98.

.PNG)

Historical PE Band (Source: Company Reports)

Key Risks:

1. Changes in government policies

2. Shift in Competitor strategies

3. Inter-dependency on the services offered by key contractors and counterparties

4. Risk associated with Joint venture

.png)

TCL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

AU

AU

Please wait processing your request...

Please wait processing your request...