Kalkine has a fully transformed New Avatar.

.png)

China has by far been the largest trading partner to Australia across numerous categories, with iron ore, gas and coal comprising a bulk of Australia's exports to the country. Australia also exports a large part of its agricultural produce to China, including beef, meat, wool, wheat, barley, sugar, etc. China has recently removed tariffs on sugar imports, including Australian Sugar. As per the information published on media platform, tariffs have been a barrier for Australian farmers for two years, limiting exports to China, which forms a key market for Australian sugar. The above decision came as a relief to the country, indicating some scope for settlement between the two countries amid the rising trade tensions on account of trade restrictions on beef and barley.

China, that accounts for a large portion of Australia’s barley exports, has sent across a shock wave in the form of the recently introduced import tariffs. Beijing announced that it will be imposing anti-dumping and anti-subsidy duties of 80.5% on Australian barley, based on the claims that barley farming has been highly subsidized by the government. The Ministry of Commerce in China stated that the dumping of cheap barley by Australia had hurt the sentiments of the domestic market. Before the decision to impose these massive tariffs on barley imports, the country had also banned the import of beef from four major suppliers in Australia on account of packaging issues.

Tariff Increases Weigh Heavy on Australia: Australia’s high dependence on China for barley exports may put the country’s farmers in trouble if the above practice continues. Almost half of the country’s exports go to China, which can cost the Australia farmers a lot in the presence of these inflated tariffs. While the country suffers from an economic threat of losing a large market share, Australia has decided not to turn things uglier by responding aggressively. The Australian Trade Minister, Simon Birmingham, stated that the country does not intend to engage in a trade war with China. Simon is seeking a dialogue with Zhong Shan, his Chinese counterpart, to discuss the recent events. The government is now mulling over the anticipated impact of the above decisions along with a corrective action to protect domestic farmers.

What Triggered China: There has been suspicion around the fact that China’s decision was triggered by Australia’s role in pushing for an international inquiry into the origins of the coronavirus, after discussions with US President Donald Trump. Beijing cited trade violations in the past to be the reason for its actions, denying any association with Australia’s involvement in initiating a COVID-19 related probe against China. As per news articles, it is believed that Beijing had earlier issued a warning to Canberra regarding the heavy duties imposed on Chinese steel, aluminium and chemical imports. However, due to repeated ignorance from the other side, Beijing proposed a high tariff on Australian barley in retaliation. The Australia Trade Minister has, however, denied the above historical events being a possible reason for the ongoing tensions.

The country has been under huge distress due to COVID-19, which makes it highly sensitive to any moderation in trade with China. Another event that confirms the threat looming over Australia’s trade relations with China is the agreement between Xi Jinping and Donald Trump, pertaining to a massive increase in China’s imports of American agricultural and energy products. This is expected to bring more trouble to the already hurt Australian exporters of agricultural goods if the US starts substituting it as a major source of agricultural produce to China. As a result, the government has proposed for the same reduction in bureaucratic trade barriers to be granted to Australia to make it a fair game for all. However, considering the emerging tensions between the two countries, it is doubtful whether China will respond positively to this matter or will continue the battle.

However, the economy remains vulnerable during these challenging times and needs a quick response to the current trading patterns with China. China turning its back towards Australian exports would bring a significant downturn in the absence of a rescue strategy. Therefore, the government has advised the businesses with exposure to China to be wary of the risks of selling into China and suggested to rely on stable and dependable markets for their offerings. For instance, the top 5 export markets for Australian produce in 2019, included China, South Korea, Japan, EU, and the USA. Therefore, suppliers have a choice to divert their exports to other markets if the ongoing tensions with China continue to escalate. Apart from China, other countries in South-East Asia are expected to stimulate further demand for Australia’s produce as population and income continue to grow. Moreover, China’s dependence on Australian beef because of its incapability to match the rising demand with domestic produce can raise the chances of settlement.

Bright Spots to look at despite the challenges: Come what may, the current situation calls for a conservative approach to business to avoid any significant losses in the future due to large Chinese exposure. While companies having a considerable market share in China mull an appropriate strategy to protect themselves from any adversities, there are others who offer a safe platform with limited or no exposure to China. Let us have a look at four such stocks in detail.

1. Incitec Pivot Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 3.85 Billion, Annual Dividend Yield: 2.34%)

Capital Raising to Strengthen Balance Sheet: Incitec Pivot Limited (ASX: IPL) is primarily engaged in the manufacturing and distribution of industrial explosives, industrial chemicals and fertilizers, and other related services. The company recently announced that its Share Purchase Plan to raise up to $75 million has been opened on 19th May 2020. The SPP followed the recently completed institutional placement of 300 million ordinary shares, which raised $600 million. During the half-year ended 31st March 2020, the company reported statutory NPAT amounting to $65 million, up 22% on prior corresponding period NPAT of $42 million. Earnings per share also increased to 4 cents per share, as compared to 2.6 cents per share in pcp.

Outlook: During the first half, the company reported good progress on its premium explosives’ technology, which will help it operate safely through the COVID-19 pandemic. The company’s premium technology supported overall mining volumes during the half. In addition, it witnessed record demand for fertilizers over the last three months as conditions stabilised. Going forward, the company expects to benefit from improvement in global fertilizer prices. Despite the uncertainty with respect to COVID-19, the company is well placed to manage short term risks and pursue organic growth opportunities, with a strong balance sheet position.

The company’s fertilizers, industrial explosives, and other related products are sold in Australia, the Asia Pacific region, and Turkey. The company also manufactures and sells industrial explosives and related products and services to the mining, quarrying and construction industries in the USA, Canada, Mexico, and Chile. Out of its four principal countries of operation, namely, Australia, the USA, Canada and Turkey, Australia & USA formed the top two sources of revenue in FY19. Total revenue for the year stood at $3.92 billion, out of which Australia accounted for $2.30 billion, followed by the US at $1.32 billion. The company’s premium technology helped it gain a larger market share in the Quarry & Construction sector in the US during 1HFY20, with an increase of 29% in EBIT of Dyno Nobel America during the half. In the Asia Pacific, the company witnessed a strong demand for fertilizers over February, March and April, on account of improved weather conditions. Henceforth, the above scenario reflects a brighter future for the business as it continues to grow the market for its product and services and remains independent of the bilateral friction between Australia and China..png)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative).png)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs IPL (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company corrected by 25.83% in the last three months and is currently inclined towards its 52-week low price of $1.565. As the markets collapsed due to COVID-19 and witnessed unprecedented levels of volatility, the stock price reacted through a heavy fall. However, the latest movements in the price have been stable, which can be attributed to the strength and resilience depicted by its business model and a decent performance despite challenges. The recent capital raising via an SPP and the institutional placement will strengthen the company’s balance sheet and provides enhanced flexibility during these unprecedented times. The company has in place a COVID-19 Response Plan, which is expected to deliver ~$60 million in cost savings through deferrals in capital expenditure and other cost reduction initiatives. We have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside in percentage terms. Hence, we give a “Buy” recommendation on the stock at the current market price of $1.99, down 0.995% on 01st June 2020.

2. GrainCorp Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 1.01 Billion, Annual Dividend Yield: NA)

Significant Turnaround in 1HFY20: GrainCorp Limited (ASX: GNC) provides a diverse range of products and services across the food and beverage supply chain. During the half-year ended 31st March 2020, the company reported strong results with underlying EBITDA amounting to $183 million, as compared to prior corresponding period value of $27 million. Underlying NPAT amounted to $55 million, as compared to a net loss of $48 million in pcp. The results were achieved after a significant repositioning of the company’s portfolio, comprising the sale of the Australian Bulk Liquid Terminals business and the successful demerger of United Malt.

Outlook: The company is continuously delivering on its operational initiatives to strengthen its core and deliver value to its stakeholders. During the first half, the company’s agribusiness benefited from its new more flexible rail contracts and the first year of the Crop Production Contract, which included a $45 million net gain. Going forward, the company is planning for higher grain exports in 2H20, offset by lower grain trans-shipments to ECA ports as domestic demand is likely to taper with positive crop outlook for FY21. Favorable ECA soil mixture has supported widespread planting for FY21 crop. Moreover, the company expects oilseed crush margins to remain favorable in 2HFY20, due to prevailing canola oil and meal values.

The company is a diversified food ingredient and agri-business company, with customers spread across 30 countries. As of FY19, the company recorded its revenue under three reportable segments, including Grains, Malt and Oils. During FY19, total revenue amounted to $4,849.7 million. Grains revenue amounted to $2,522.3 million, with Australiasia accounting for more than half of the revenue at $1,465.8 million. In response to the recent trade tensions between Australia and China, GrainCorp’s CEO, Robert Spurway, highlighted that the direct impact of the recent events is not significant on the business in the short term, but will ultimately bring disappointment to the domestic growers if a settlement is not reached. China remains an important market for trade and resolution for the ongoing issues should be a key priority for the government at the current stage. Meanwhile, the company will continue to benefit from its performance in other markets, with a diversified geographical reach and a new and simplified operating model..png)

Valuation Methodology: P/CF Multiple Based Relative Valuation (Illustrative).png)

P/CF Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

A-VIX vs GNC (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gained 23.46% in the last one month and is currently trading close to the average of its 52-week trading range of $2.810 - $6.470. At the end of 1HFY20, the company had a strong balance sheet with zero core debt. The company’s new operating model helped it deliver a decent performance in each of its business segments during the first half. A significant turnaround during the first half and simplification of the business model raised optimism around the company’s performance in the market, due to which the stock price spiked high, as depicted in the chart above. The above decisions are expected to add further value to the business in the future and will ensure that investor confidence remains intact, going forward. We have valued the stock using a P/CF multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside in percentage terms. Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $4.41, down 0.226% on 01st June 2020.

3. South32 Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 9.26 Billion, Annual Dividend Yield: 3.02%)

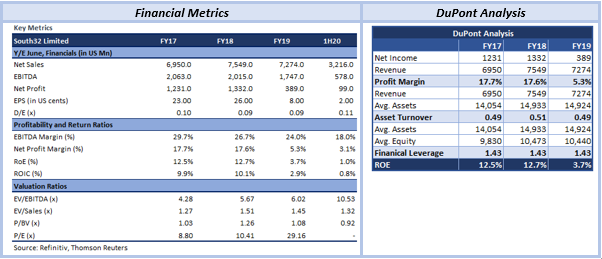

A Diversified and Resilient Portfolio: South32 Limited (ASX: S32) is a diversified mining and metals company, engaged in the production of alumina, aluminium, bauxite, energy coal, metallurgical coal, manganese coal, manganese alloy, etc. In the March quarter report, the company updated that it increased Alumina production by 4%, with record YTD production at Brazil Alumina. The company also reported record year to date production at Hillside Aluminium. Net cash for the period declined by US$127 million, partially due to the distribution of interim ordinary and special dividends.

Outlook: The company’s strong financial position and resilient portfolio have placed it well to navigate and mitigate the impact of COVID-19 on the business. In response to the turbulence in the market, the company adjusted its capital expenditure priorities to defer, rescope, or cancel non-critical projects. The company has a portfolio diversified by commodity and customer with growth options embedded and a pathway to exit low returning businesses. The company’s production and sales volumes from the Australian operations have remained largely unaffected by COVID-19. However, in response to COVID-19 containment restrictions, production guidance for Australia Manganese ore has been reduced by 5%. After the ease of restrictions in South Africa on 1st May, the company guided that FY20 production for South Africa Energy Coal is anticipated between 21-23 Mt. For Hillside Aluminium, production is expected at 718 kt, with lower raw material and power price expected to benefit unit costs in H2.

The company has a diversified profile of customers spread across Australia, Singapore, Southern Africa, Switzerland, Netherlands, India, China, etc. During FY19, total revenue from external customers amounted to US$7,274 million, out of which China contributed US$438 million. Southern Africa was the largest contributor to revenue at US$1,214 million, followed by Singapore at US$1,090 million. The top two were then followed by four other locations before China. As per the above data, the company seems to be in a safe position amid the rising tensions between Australia and China. Given the quality of its portfolio and a diversified geographical footprint, the company seems capable of effectively dealing with the ongoing crisis.

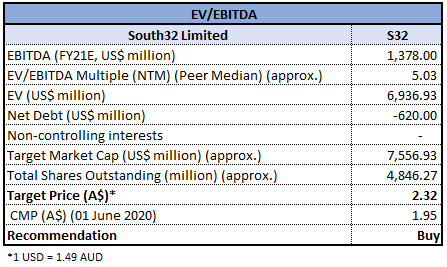

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

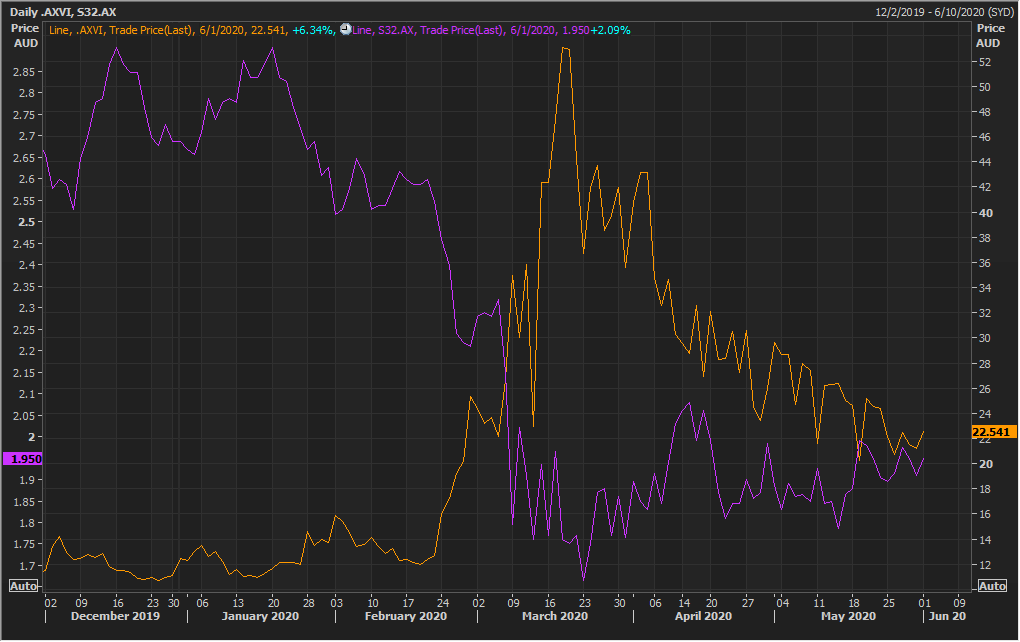

A-VIX vs S32 (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company corrected by 16.19% in the last three months and is currently inclined towards its 52-week low price of $1.585. The company’s stock was no different than others in terms of its reaction to a highly volatile market in March. Since then, the price has demonstrated a gradual path of recovery. A strong balance sheet position remains at the core of its strategy. The company’s disciplined approach to capital allocation and a simplified capital management framework ensures that the shareholders will be rewarded as financial performance improves. Despite the uncertainty in the market, South32’s diversified business is what makes it a safe-haven while other industry players struggle due to limited market exposure. We have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside in percentage terms. Hence, we give a “Buy” recommendation on the stock at the current market price of $1.95, up 2.094% on 01st June 2020.

4. JB Hi-Fi Limited (Recommendation: Watch, Potential Upside: Low Single-Digit)

(M-cap: A$ 4.26 Billion, Annual Dividend Yield: 4.04%)

Continued Sales Growth in April & May: JB Hi-Fi Limited (ASX: JBH) is primarily engaged in the retailing of home consumer products, including consumer electronics, software, appliances, etc. The company recently released a sales update for the quarter ended 31st March 2020, wherein, it reported comparable sales growth of 11.3% for JB Hi-Fi Australia and 13.9% growth for the Good Guys. Comparable sales for JB Hi-Fi New Zealand declined by 3.3%, which does make a large impact due to a small financial contribution it makes to the Group. The company continued to provide customers with the necessary appliances while at home and witnessed strong sales growth in Australia.

Outlook: The company has seen continued strong sales across Australia in April and May, as it addressed consumer demand through its online businesses. Going forward, the company will be focused on modifying its online channels to deliver better customer experience and drive future demand. However, due to the uncertainty regarding consumer purchase behaviour, the company has withdrawn its FY20 sales and earnings guidance. The company has a loyal customer base and a decent financial position to sail through these difficult times.

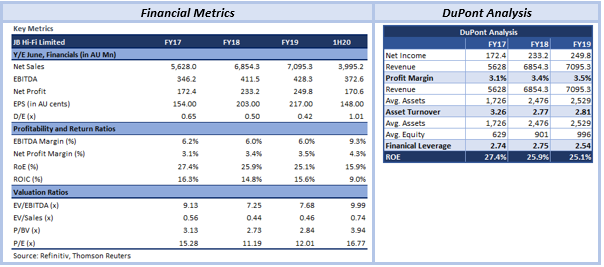

The company has an excellent business model which makes it a leading supplier of electronics and appliances in Australia. The two brands, namely, JB Hi-Fi and The Good Guys enjoy a large market, for the high-quality electronics and appliances provided by them. It enjoys a strong position with its sticky customers purchasing the best brands at convenient prices. Moreover, with a customer-focused approach to business and multi-channel operations, the company has a competitive edge over other retailers. Out of the total sales of $3,995.2 million, around 97% was contributed by JB Hi-Fi Australia and The Good Guys. The company witnessed an 18.3% growth in online sales during the half and continued to invest in its online channel. Overall, with a large part of its sales occurring in the domestic land, the company remains safe from the risks of selling in the international markets.

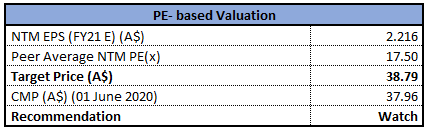

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative)

P/E Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

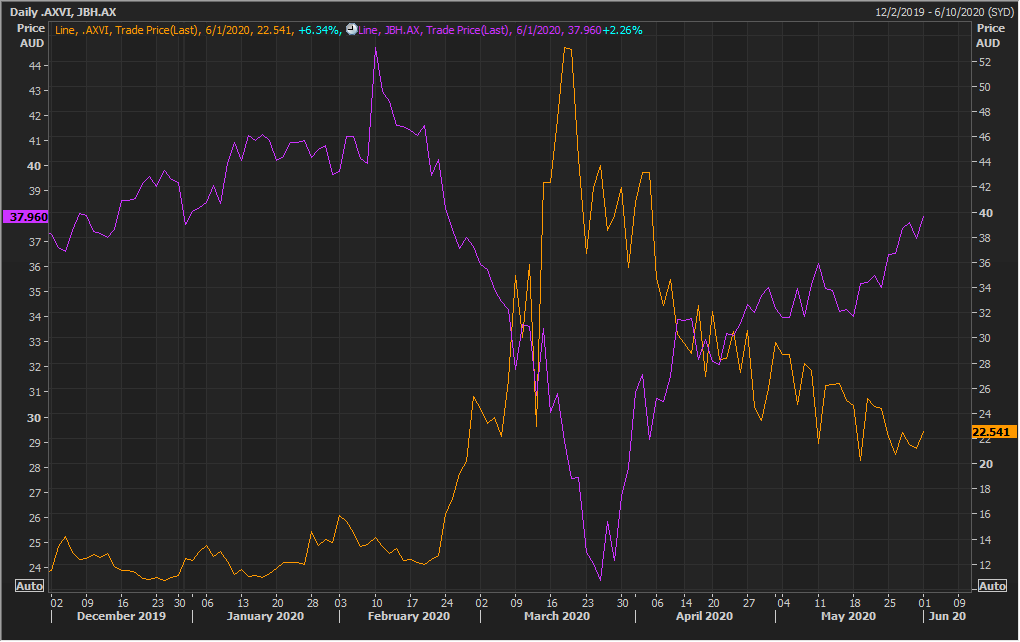

A-VIX vs JBH (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gained 6.61% in the last one month and is currently trading above the average of its 52-week trading range of $20.790 - $46.090. Amid the COVID-19 led crisis, the company has continued to adopt a conservative approach to managing its balance sheet and strengthening the liquidity position, by securing facilities worth $260 million in this uncertain environment. Being the go-to brands for a large set of customers, JB Hi-Fi and The Good Guys continued to witness demand for electronics and appliances even during these challenging times. The stock price reacted positively to the recent update provided by the company, which reported continued sales growth in April and May. Considering the above scenario, we anticipate that the company’s strong market position will continue to provide support to the stock price, going forward. We have valued the stock using a P/E multiple based illustrative relative valuation method and arrived at a target price with low single-digit upside in percentage terms. Hence, we have a wait and watch stance on the stock at the current market price of $37.96, up 2.263% on 01st June 2020.

(7).PNG)

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...