Kalkine has a fully transformed New Avatar.

Company Overview - TPG Telecom Limited is an Australia-based company, which is engaged in the provision of consumer, wholesale and corporate telecommunications services. The Company conducts its operations through three segments: TPG Consumer, TPG Corporate and iiNet. The TPG Consumer segment provides retail telecommunications services to residential and small business consumers. The TPG Corporate segment provides telecommunications services to corporate, government and wholesale customers. The iiNet segment provides telecommunications and technology services to residential and business customers. The Company's telecommunications services include the provision of data, Internet, voice, telehousing, network capacity and other services to consumers and corporate customers. The Company provides a range of National Broadband Network (NBN) services. The Company also provides broadband services over its fiber to the building network.

TPM Details

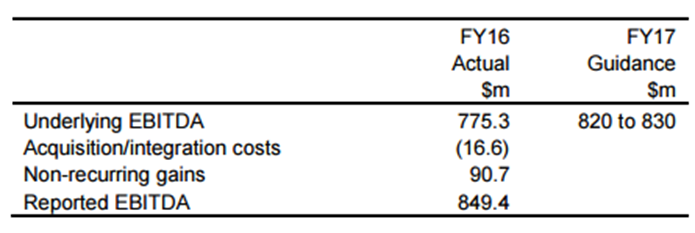

Delivered a strong bottom line performance: TPG Telecom Ltd (ASX: TPM) reported a 69% increase in the Net Profit After Tax (NPAT) of $379.6m in FY 16 and 61% increase in the earnings per share to 45.3 cents per share. The growth drivers for the contribution were realization of post-acquisition integration benefits, nine months of lower access costs arising from the ACCC’s fixed line services final access determination, and an increased contribution from Tech2. TPM revenues rose $12.1 million to $654.6 million for fiscal year of 2016, even though the group faced $10.1 million impact from the iiNet consolidation. The group derives 56% of revenues from Data while both internet and voice account 22%. TPM’s underlying EBITDA grew 60% to $775.3m. However, the group had a bank debt of $1,350m and a net debt to EBITDA leverage ratio of approximately 1.8x at the end of the FY 16 ending 31st July 2016. Additionally, TPM has posted in FY 16 the irregular items that includes $73.1m gain on the group’s previously held interest in iiNet in which $73.1m was post tax. The $17.6m profit is realized on a part-disposal of shares held as an investment by the group in which $12.3m is post tax. There is $10.3m transaction fees relating to the group’s acquisition of iiNet. The $6.3m restructuring costs arose from iiNet integration activities in which $4.4m is post tax. But, the group built a strong cash flow in FY 16 with $759.2m cash generated from the operations (pre-tax). Moreover, with TPM finishing acquisition of iiNet, the company is now focusing on the integration of the businesses to enhance the efficiency of the combined organization.

FY 16 Financial Performance (Source: Company Reports)

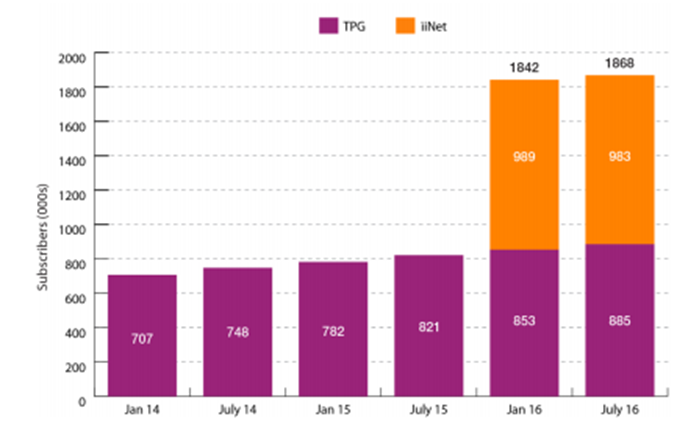

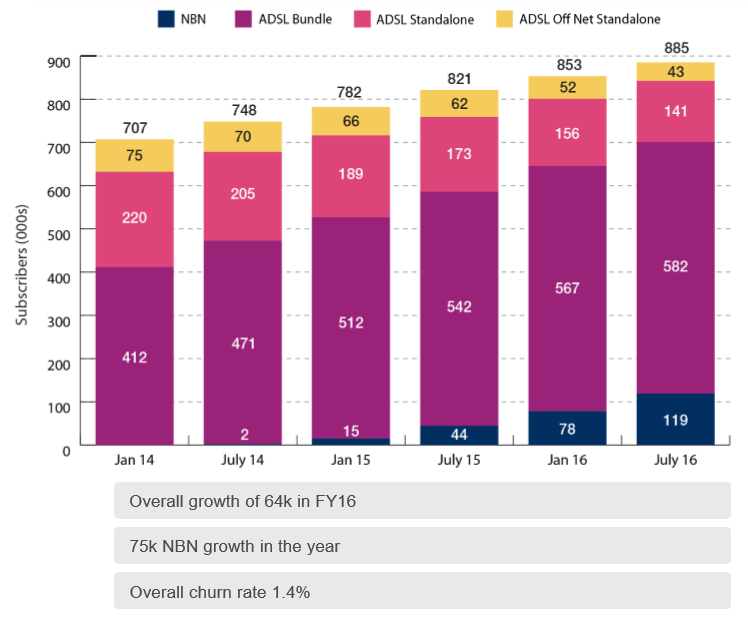

iiNet Contribution in FY 16: iiNet acquired by TPM, has played a strong role in TPM performance for FY16, as this acquisition contributed an EBITDA of $242.6 million post acquisition. With this acquisition, TPM enhanced their consumer broadband subscribers to over 1.8 million. Moreover, the Consumer Division has posted further organic growth of its broadband subscriber base in FY16 as the subscribers grew 64k due to the growth in NBN customers. However, the iiNet broadband subscribers declined slightly from 989k to 983k as at the end of FY16. But, TPM even boosted their mobile subscriber base to 475k including 171k iiNet subscribers. During FY 16, TPM migrated over 200k of its mobile subscribers to its new MVNO arrangement with Vodafone Hutchison Australia.

Group Broadband Subscribers (Source: Company Reports)

Ongoing efforts to strengthen network infrastructure: TPM in FY 16 was a successful bidder in the auction for spectrum in the 1800 MHz band. TPM had acquired two 10 MHz of spectrum lots in each of the regions Darwin, South Queensland, Northern NSW, Canberra, Southern NSW, Regional Victoria, Regional South Australia, and Tasmania. Additionally, TPM was the winning bidder for one lot of 2x5 MHz (i.e., 5 MHz) in each of Adelaide and Western NSW. In addition, TPM’s extensive network infrastructure grew the infrastructure assets acquired through the iiNet acquisition. Overall, the fixed line broadband has been the backbone of the TPM’s growth but wireless connectivity is the future need of Australian telecommunications consumers. Therefore, TPM is investing in the latter to have significant long-term benefits for the group.

Competitive Edge: TPM’s competitive advantages is the extensive network infrastructure which enabled TPM to offer market leading on-net products to a broad range of customers right across the country as well as overseas utilizing the vast international capacity. Moreover, TPM being the second largest fixed broadband customer base in Australia has an opportunity to grow into a major provider of NBN services as well as offer super-fast broadband services over the ‘fibre to the building’ network. TPM is aiming to further expand market share via strength of expanding direct sales team and through its valuable wholesale customer relationships. Additionally, TPM’s has an efficient operating cost model with experienced management and has over 6,000 dedicated personnel across Australia, New Zealand, the Philippines and South Africa.

Guidance for FY 17: For fiscal year of 2017, TPM expects the underlying EBITDA to be in the range of $820m to $830m, excluding any impact from potential operations in Singapore and the capital expenditure is expected to be range of $370 million to $420 million. The guidance for capex in FY 17 includes the $72 million for 1800 MHz spectrum, $50 million for committed international capacity purchases (SX & SEA-US) and substantial fibre rollout capex. Moreover, in FY 17, TPM would continue to focus its efforts on growing its consumer and corporate customer bases profitably and intends ongoing investments in expanding its network infrastructure.

Prospects for fiscal year of 2017 (Source: Company Reports)

Growth in the Dividends: The total FY 16 posted 26% growth in the dividends. There is an increased final dividend of 7.5 cents per share bringing the total FY16 dividends to 14.5 cents per share (fully franked). TPM also boosted their capital position by raising over $322.5 million with $300 million from institutional share placement and $26.9 million from a share purchase plan. Moreover, TPM also offloaded their stake in Vocus leading to proceeds of $60.0 million. TPM further invested $3.0 million in Covata Limited. On the other side, TPM capital intensive business led to a rise in capital expenditure by $127.2 million to $281.0 million for fiscal year of 2016 as compared to the same period of last year. This rise is mainly on the back of one-off payments for the acquisition of a data center property in Sydney of $27 million and for buying spectrum for $15 million. The group is constantly making investments to enable a better connect within corporate customers as well as for ‘fibre to the building’ (FTTB) project.

Consumer Broadband Subscribers (Source: Company Reports)

Stock Performance:TPM stock price fell 43.4% in the last three months (as of December 02, 2016), due to lower than estimated performance and guidance from the group. TPM’s high capital expenditure coupled with lower growth forecasts for FY17 as compared to FY16 also hurt the investors sentiments on the stock. Moreover, the group showed interest to bid for up to 75Mhz of spectrum in Singapore. Accordingly, there have been concerns around a further burden on the group to fund its Singapore operations. On the other hand, the group’s Monthly ARPU for broadband customers rose as expensive NBN services (ARPU ~$67) replaced DSL services (on-net ARPU ~$59). Moreover, the Corporate Division telco costs as a proportion of revenue declined to 39% in fiscal year of 2016 as compared to 42% in the prior corresponding period on the back of decrease in pricing in corporate business. Moreover, TPM’s investment in network infrastructure paid off leading to a better operating margin. The continued organic growth and the integration of iiNet into the business have resulted in further increases in revenue, profits and dividends for shareholders. iiNet integration drove the overall Corporate Division Net promoter Score (NPS) to over +70. The group’s Broadband has +38 NPS. TPM has also indicated interests towards the 700 MHz prospective auction by the Australian Communications and Media Authority. The group will be holding its Annual General Meeting on December 07, 2016. With the recent crash in the markets, we believe TPM stock is available at attractive levels. The stock is having a decent dividend yield and a reasonable P/E. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of – $6.83

TPM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...