Company Overview – Titan energy Services (TTN) is a provider of drilling, accommodation, equipment hire and catering to the coal seam gas (CSG) industry. The company has demonstrated a track record of diversification, via organic growth and acquisition, is exposed to growth in CSG industry and has a strong management team that is positioning TTN to expand further geographically.

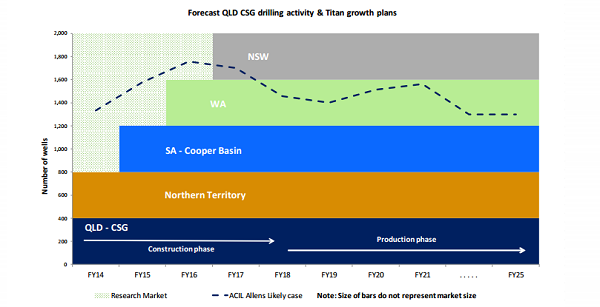

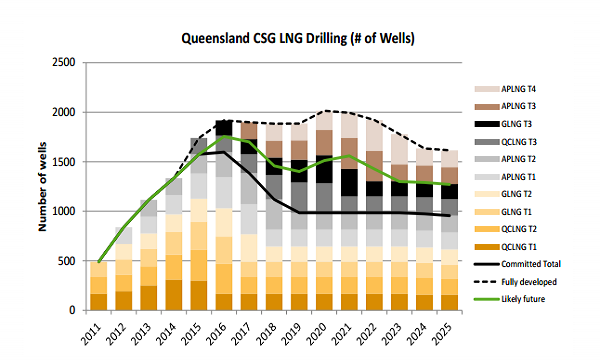

Analysis – CSG well numbers in Queensland are expected to increase from the 1021 reported in 2013 to peak around 1600 in FY16, excluding any Arrow Energy – related drilling. Including Arrow trains 1 and 2 the FY16 figure could be closer to 1900. We believe FY15 and FY16 will be very strong years for TTN and that any future decline is likely to be offset by acquisitions and an increase in revenue generated from reoccurring well maintenance that TTN is in the process of evaluating.

Unlike CAPEX exposed mining services companies, TTN has been aware that drilling demand may plateau or decline around FY17 for several years and has acted to diversify its revenue. TTN has expanded into new offerings (accommodation, equipment hire and catering) that should support revenue in new industries and geographies. TTN’s subsidiary, RCH has increased room numbers from 110 at the start of FY12 to 979 at the 1H14 results. 305 rooms were added in 1H14 and we expect utilization to increase following the rapid expansion. RCH is not capital intensive as the rooms are leased on 2-4 year terms that give TTN a favorable position should demand eventually ease.

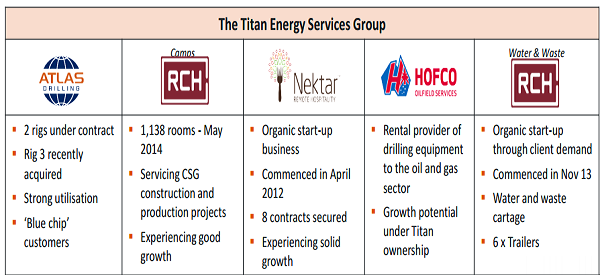

Group Segments (Source - Company Reports)

Group Segments (Source - Company Reports)

We believe TTN provides good exposure to the growing CSG services sector in Queensland whilst at the same time it has diversified its earnings profile to protect itself from the eventual decline in the annual number of wells drilled. We believe FY15 and FY16 will be very strong years for TTN and with its strong balance sheet we expect the expansion into new industries and geographies to support earnings in the medium to long term. TTN is often lumped with existing mining services companies that have experienced a decline in client capital expenditure that TTN is expected to begin to go through around FY17. We view the two situations as largely different as TTN’s industry has far greater visibility and the downturn is highly unlikely to catch the company by surprise. TTN has spent last two years preparing itself and we believe still has substantial earnings growth to come prior to any decline in wells.

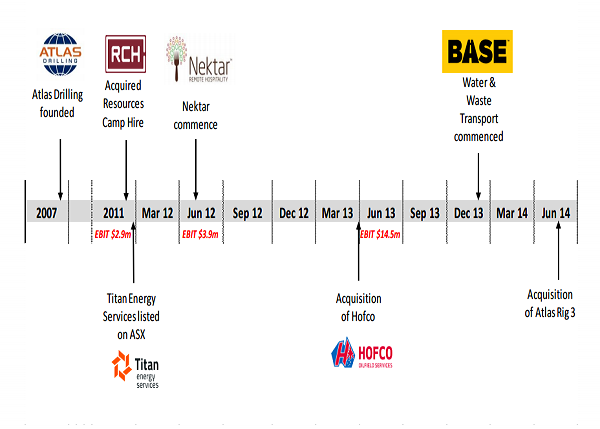

Group History (Source - Company Reports)

Group History (Source - Company Reports)

Titan Energy Services is a diversified services provider to the oil and gas, mining and infrastructure sectors. The company has four primary subsidiaries that operate across four divisions: Drill Rigs, Camps Catering and Equipment Hire. The operating companies are Atlas Drilling, RCH, Nektar and Hofco, respectively.

Forecast CSG Drilling (Source - company Reports)

Forecast CSG Drilling (Source - company Reports)

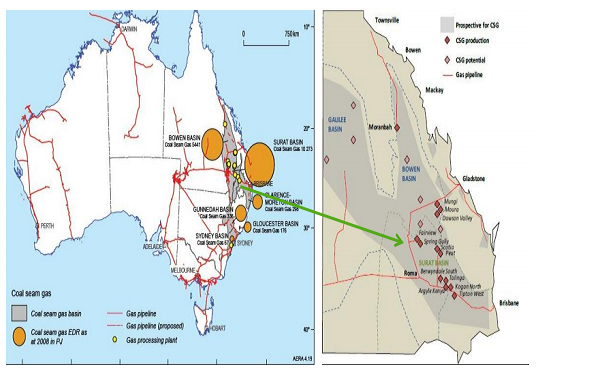

Atlas Drilling provides drilling services to the coal seam gas sector, predominantly around the Surat Basin area in Queensland. The business was established in 2007 and today owns and operates three rigs and leases an additional rig. Currently Atlas generates its revenue by drilling wells, casing them and moving onto the next one. Revenue is based on a daily rate. The company is exploring funding possibilities for future rig growth and we expect additions to the fleet. Resource Camp Hire (RCH) provides portable camp accommodation and as of December 2013 it has 979 rooms available. The rooms are based on shipping containers and are easily transportable. They include accompanying rooms such as kitchen, recreational rooms etc. The business was acquired in September 2011 and at the time had 110 rooms. RCH focuses on the CSG industry and rooms are acquired during both construction and production. RCH also provides accommodation to the road, civil and construction industries. Nektar provides remote camp catering and management and commenced operations in April 2012. At the 1H14 results Nektar was servicing nine contracts. The bulk of revenue was inter segment along RCH bit it is targeting standalone revenue. Hofco is a drilling equipment rental provider focusing on the oil and gas sector. Equipment is generally hired at day rates for durations varying from week to a year.

Quennsland CSG drilling areas (Source - Company Reports)

Quennsland CSG drilling areas (Source - Company Reports)

Most of TTN’s revenue is associated with drilling and as mentioned earlier the well numbers expected to increase from 1000 in 2013 to over 1500 in 2015 and 2016. There will very likely be a decline in upstream capital expenditure in the medium term, however we expect this to be partially offset by the anticipated increase in reoccurring operating expenses. The maintenance phase will clearly provide some opportunities for TTN. Regardless of the decline concerns comparing TTN’s CSG drilling to that of mineral exploration are inaccurate. We believe the amount of drilling will not cease it is more likely to plateau and eventually ease before settling close to or even higher than 1000 wells per annum. TTN has placed a large amount of focus in expanding its offering so as not to remain too exposed to a potential slowdown in Queensland CSG drilling.

Forecast Drilling (Source - Company Reports)

Forecast Drilling (Source - Company Reports)

TTN announced in May that it had purchased the only rig in its fleet that it did not own for $5.2m from its lessor, Pangaea Drilling. The price appears very reasonable given Rig 3 recently underwent a refurbishment and it should result in improved Atlas margins. We view the fact that Pangaea was happy to take stock in TTN favorably and believe it is appositive indicator in regards to the outlook for the industry and also a vote of confidence for TTN’s management.

TTN Daily Chart (Source - Thomson Reuters)

TTN Daily Chart (Source - Thomson Reuters)

TTN announced an unaudited FY14 EBIT result of approximately $18.5m. This is comfortably higher than FY13 EBIT of $14.5m but below the recently lowered guidance range of $19.5m - $21m. The result represents 28% growth on FY13 and half on half growth of 32% given the 1H14 result of $8.0m EBIT. The primary cause of the downgrade was the delay in the start of an important contract that covers camps, water, waste and catering. TTN expected to begin the contract in late May however it has only recently begun and TTN lost 37 operating days, which we estimate cost the company $1m in delayed EBIT. The earnings will move into FY15 and ensure a strong start to the year. In regards to FY15 no guidance was provided however the company stated that it was looking forward to another strong year of growth. TTN has grown via acquisition and investment and continues to flag further opportunities. The company also continues to tender for work outside of CSG in Western Australia, South Australia and Northern Territory. We put a BUY on the stock at the current price of $2.06.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...