Australian Pharmaceutical Industries Ltd

.png)

API Dividend Details

Ongoing Retail Growth: Australian Pharmaceutical Industries Ltd (ASX: API) reported a solid revenue increase of 3.3% year on year (yoy) during FY15, driven by strong retail network sales with priceline which rose by 10.4% yoy to $1.05 billion during the period. The Comparable store retail sales and volumes rose by 4.5%, while the group’s retail network reached over 420 stores as of August 2015. Australian Pharmaceutical EBIT rose 13.7%, while NPAT surged 37.6% to $43.1 million, against prior corresponding period (pcp). However, Pharmacy Distribution revenues decreased to $2,476 million during FY15 affected by Price deflation as well as competitor banner acquisitions, but delivered revenue growth of 6.5% during the period eliminating PBS reforms. Meanwhile, New Zealand segment is showing better revenue and gross profits post the FY14 restructure, which rose by 17.5% and 12.9%, respectively, during FY15. Australian Pharmaceutical also improved its balance sheet, by decreasing its average net debt to $145.5 million while cash conversion rose by 12%. The group also enhanced its return on capital equity to 13.45%, while generated an ROE of 8.62% during the period. Management targets to grow its Priceline Pharmacy network by over 20 stores in 2016 as well as intends to derive better benefits from oneERP completion.

.png)

Retail sales performance (Source: Company Reports)

On the other hand, the shares of API delivered outstanding performance this year, generating year to date returns of 136.31%, and rallied over 31.46% in the last four weeks alone (as at 02, November 2015). The stock is trading at relatively higher valuation with expensive P/E of 22.5x, and is at its 52 week high price. API’s dividend yield is also just 2.27%. We believe that the shares are fully valued and do not shape-up for a buying opportunity. Based on the foregoing, we give an “Expensive” recommendation to API at the current price.

API Daily Chart (Source: Thomson Reuters)

Harvey Norman Holdings Ltd

.png)

HVN Dividend Details

Delivered strong growth: Harvey Norman Holdings Limited (ASX:HVN) reported that the total sales from its franchised complexes, commercial divisions as well as further sales outlets in Australia, New Zealand, Slovenia, Croatia, Ireland and Northern Ireland (excluding Singapore) increased 6.1% to $1.50 billion during the first three months ended on September 2015 against prior corresponding period. The group reported that it’s like for like global sales improved by 7.0% yoy during the period. Meanwhile, HVN’s global sales had positive currency impacts during the period (a 6.9% increase in the Euro and an 18.3% increase in the UK Pound). However, 1.5% devaluation in the NZ$ negatively affected the global sales. Profit before tax and minority interests, and excluding property revaluation adjustments, for the consolidated entity (unaudited preliminary accounts) surged by 27.8% to $91.8 million during the first quarter of 2015 against $71.9 million in the first quarter of 2015. The shares of Harvey Norman delivered a year to date returns of over 18.21% during this year to date (as at 02 November 2015). However, the stock fell over 11.01% in the last three months partly due to slight weakness in consumer outlook (based on instances such as the recent online sales glitch) and we believe this might continue further. Moreover, we expect a challenging outlook with regards to FY17 and 2H FY16 in view of the housing cycle to undergo modest correction.

.png)

First quarter 2016 highlights (Source: Company Reports)

HVN also acquired a major stake of a 49.9% interest in Coomboona Holdings, which is into dairy farm operations and has a pedigree breeding and genetics division for around $34 million. This move by HVN is also raising investors’ concerns over the potential group’s bottom line impact and synergies of the acquisition. Moreover, the first quarter of 2016 results were also driven by currency appreciations and any fluctuations in the currencies might pose pressure on HVN. We believe that the stock is trading at an expensive valuation and accordingly, we give an “Expensive” recommendation on the stock at the current price.

HVN Daily Chart (Source: Thomson Reuters)

1-Page Ltd

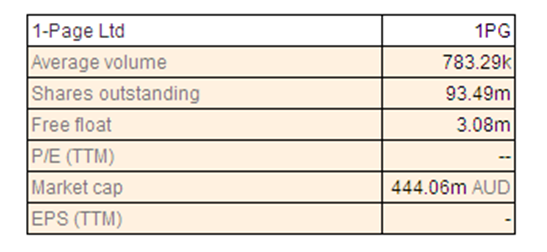

1PG Details

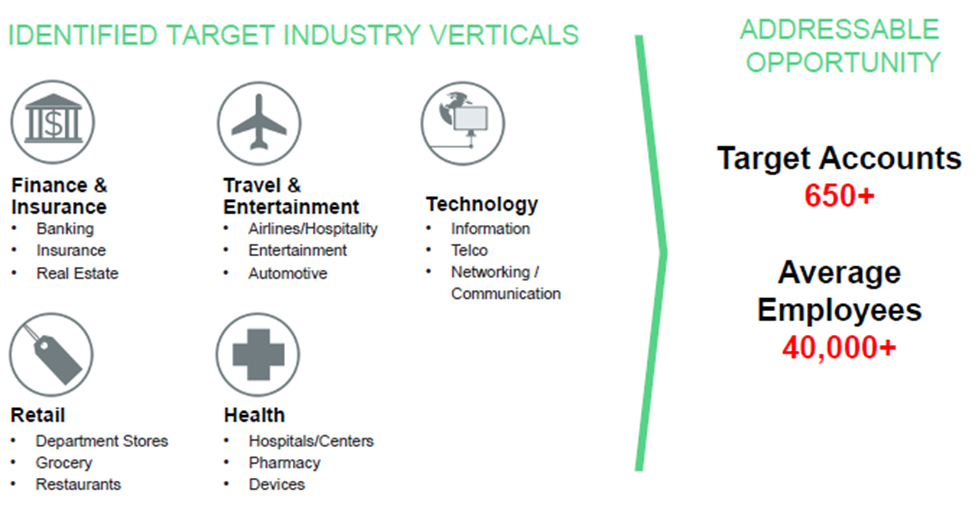

Raising funds for potential growth and acquisitions:1-Page Ltd (ASX: 1PG) recently announced for completion of the institutional equity placement for raising over $50 million. This was through a fully underwritten institutional placement of 11.1 million shares at $4.50 per share, and 1PG intends to use these proceeds for commercialization of its recruitment platform as well as for potential acquisition (already under negotiations) to boost its top line. The group also intends to expand its sales teams to cater to the customer needs as well as enhance distribution partner network. The company recently announced addition of three new industry leading clients to its sourcing platform, which include a fortune 500 financial intelligence company, a global provider of healthcare and pharmaceutical consulting and a blue-chip software company.

Investment in Direct Sales (Source: Company Reports)

1-Page generated revenue growth by 70% to $158,900 in the half year ended on July 2015 as compared to pcp. Given the market cap of the company which is about $450 million, the aforesaid revenue for six months seems to be little low. The shares of 1-Page generated solid year to date returns of over 270.37% (as of November 02, 2015). Based on the foregoing, we give an “Expensive” recommendation for the stock at the current price, and would review the stock at a later date.

1PG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...