Kalkine has a fully transformed New Avatar.

.png)

Crude Oil prices, the second major reason for the ongoing economic distress after COVID-19, have been the most talked about issue in the news lately. As the disagreement between Saudi Arabia, a key member of OPEC, and Russia, a non-OPEC leader, kick-started an oil price war, the former decided to increase its production to more than 10 million barrels per day for gaining market share. The decision, however, didn’t turn out to be a favourable one, as the demand for oil went down heavily due to the hampered economic activities amid coronavirus pandemic. As a result, both Brent crude and West Texas Intermediate, the benchmarks for oil prices, saw significant roller-coaster ride in the recent times. Let us have a look at the events that have been shaping up the oil market recently..png)

Brent Crude Chart (Source: Thomson Reuters)

.png)

WTI Chart (Source: Thomson Reuters)

Saudi Aramco Goes Public: The very first in the row of events was the decision to sell off a part of Saudi Aramco, Saudi Arabia’s government-owned company, in an IPO. While the government had valued the company at $2 trillion, the process derailed a bit as international investors chose to agree on a value not more than around $1.7 trillion. The decision to sell a part of its ownership in Saudi Aramco was aimed at fulfilling the objective to raise funds for Saudi Arabia’s economic reform plans and invest in other non-oil industries to guard the economy against oil-price volatility. The government, however, could receive only a fraction of its expectations from the sell-off, as investors did not agree on the targeted valuation.

Proposed Peace Deal Sets Oil Producers on a War: The peace deal to cut oil production followed the above decision as the members of the Organisation of Petroleum Exporting Countries (OPEC) decided to take a co-operative step forward, to stabilize the turmoil in the oil markets and push prices up for the collective benefit of oil producing nations. Members of the cartel along with Russia, one of their oil producing allies, decided on a production cut of 500,000 barrels a day through the first quarter of 2020, to cope with the fall in demand for oil due to rising global tensions, especially the US-China trade war. As the situation aggravated due to the outbreak of COVID-19, oil-producing nations decided on a larger production cut to survive in the battle ground. The deal, however, failed to please Russia, which later refused to allow deeper cuts in production. In response, Saudi Arabia, the dominating member of OPEC, shot another arrow by breaking up with the member nations of OPEC and triggering a price war against Russia through increase in oil production, eventually leaving the oil producers and global oil prices in a worse shape. Oil prices saw a steep fall of around 30%, inducing global tensions. The price that went down to the lowest level in 17 years came as a shockwave for the already beaten down economies.

Will Saudi Arabia Settle for its Ally: On 2nd April 2020, oil prices rallied by 25% as US President, Donald Trump tweeted on a possibility of a co-operative production cut of 10-15 million barrels per day, by Saudi Arabia and Russia. Although, the tweet has temporarily healed the hardest hit oil prices and the sentiments of the market players, there are speculations about the viability of the information as a collective reduction in production by 10-15 mb/day by Saudi Arabia and Russia would mean shaving off a massive portion of their output. However, optimism remains regarding the price war ending on a good note as Saudi Arabia’s Mohammad Bin Salman called for an urgent multinational meeting to discuss oil markets, after a call with Trump. The oil price movement is keenly watched out for given the upcoming OPEC meeting.

Trump Leaves the Audience in Dilemma: There is uncertainty about whether the expected production cut, as tweeted by Donald Trump, will be solely on the part of Saudi Arabia and Russia, as the former has been of a view for a co-operative reduction in production by a group of countries. Although calling for an emergency meeting, Saudi Arabia did specify about having a fair agreement to stabilise the oil markets, stayed silent on any specific plan of action. While Trump’s expectation for a production cut remains a doubt for many, one cannot deny the possibility of an actual reduction as the price war has only brought an economic pain so far.

The Expected Settlement: What the price war actually means for the oil-producing nations has really been a matter of thought for the parties that took an egoistic inclination and reacted impulsively, while the underlying purpose to the peace deal was to revive together. The price war triggered by Saudi Arabia backfired as a result of a massive demand destruction due to coronavirus pandemic, that led the friend-turned-foes, Saudi Arabia and Russia, drowning in excess oil supply and sinking revenues.

As per media reports, the Saudi Arabian government announced a reduction in its budget spending which is expected to have an adverse impact on the already suffering private non-oil sector. The consequences of its own decisions have left the world pondering over the possibility of Saudi Arabia soon experiencing a pitfall.

Recent events in Russia are signaling the same fate for oil companies as the lack of demand weighs on its revenues and budget. Anton Siluanov, the Russian Finance Minister, has already warned regarding a drop in oil and gas revenues and anticipates a budget deficit if the war continues.

Saudi Arabia and Russia may not see the impact as bad as the US, which is suffering from a double whammy of a drastic drop in oil demand and an indebted oil and gas industry. As a result of increased pressure on oil prices due to the price war and COVID-19 impact, oil and gas companies in the United States would find it difficult to clear their dues and may land in a difficult situation.

Apart from the U.S, the price war has been the bad news for all other oil producing countries, which do not have a diversified economy and are dependent on oil revenues for survival. Countries like Algeria, Iraq and Nigeria are facing fiscal strains and are exposed to the risk of downfall if the war instigators fail to reach a settlement.

Impact on the Australian Stock Market: The Australian stock markets were also engulfed in the price war, as S&P/ASX 200 reported a historic decline of 7.4% as oil prices slashed in March 2020. Leading oil players listed on the ASX reported significant decline in prices, some of them being, Oil Search Limited, Woodside Petroleum Limited, BHP Group Limited, etc. As energy stocks comprise a large portion of the Australian Securities Exchange, the benchmark index is sensitive to changes in oil prices. Moreover, the indebted U.S energy companies being at a risk of default due to the fall in oil prices can have a spillover effect on US corporate and global debt markets.

If the situation reverses and the parties to the war reach a settlement, the stock market is ought to react in an opposite manner. This would mean a gain for the energy players listed on ASX, with profitability becoming a low-hanging fruit for the best performers. In light of the relief from the recent rise in oil prices, we suggest investors to have a look at the below energy players that depict a decent potential for long-term growth.

Latest Development: The meeting, which was earlier scheduled for Monday, 5th April 2020, has been delayed. The shift in dates has given rebirth to the pessimism surrounding the oil market earlier. As the U.S president intervened in the raging price war between Saudi Arabia and Russia, the oil market saw a temporary escape from the ongoing battle. However, there has been increased skepticism regarding any possible settlement after the meeting was delayed and Saudi Aramco decided to delay the release of its crude official selling prices for the month of May. This is the first time that Saudi Aramco has been compelled to delay OSPs, which has again left the stakeholders in a dilemma.

Amidst the scenario, this report brings in-depth analysis on 4 ASX listed stocks and highlight the potential of being diversified during market meltdown scenarios.

1. Woodside Petroleum Ltd (Recommendation: Buy, Potential Upside: high single to low double-digit)

WPL appears to be Well-Positioned to Ride the Growth Wave: Woodside Petroleum Ltd (ASX: WPL) is engaged in the management and operation, development, production, transportation and marketing of hydrocarbon, gas, oil and condensate reserves. During FY19, the company reported strong revenue and operating cashflow, reflecting soaring capacity of the base business to support growth. In FY19, WPL reported a solid annual production of 89.6MMboe and is well placed to execute spend with the liquidity of US$6,952 million and low gearing of 14.4%. The company delivered value for shareholders and achieved underlying NPAT of US$1,063 million and paid an annual dividend of 55 US cps, representing a payout ratio of 80% of underlying profit.

.png)

Valuation Methodologies: (1).png)

*1 USD = ~1.66 (as on 6 April 2020).png)

Brent Crude Price vs WPL Price (Source: Thomson Reuters).png)

A-VIX vs WPL (Source: Thomson Reuters)

Stock Recommendation: The above chart depicts that the stock price has followed the same pattern as Brent Crude Index. As prices slashed during March 2020, the stock price took the same path downwards. Also, as visible in the second chart, the price has also reacted to market volatility going down steeply as the markets reacted to coronavirus outbreak. In the most recent spike in crude prices, the stock price responded with an upward movement. Therefore, with WPL’s stock price completely aligned with the benchmark index, a recovery in price is expected as soon as the oil market stabilizes. The uncertainty in the world with the fallout of COVID-19 might pose some near-term challenges and could limit the upside, but the stock looks attractively priced at the current trading levels. The company has built a financial resilience for a growth period and has a well-balanced debt profile. WPL has taken steps to manage volatility and might benefit from the higher oil prices if they eventuate. It has also deferred some non-essential maintenance activity and is maintaining an appropriate level of activity to come out stronger once the storm is over. Considering the trading levels, financial strength and decent growth catalysts, we have valued the stock using EV/EBITDA multiple and price to cash flow multiple based relative valuation methods and have arrived at an indicative target price with an upside of high single-digit to low double-digit (in percentage terms). For the said purposes, we have considered, Oil Search Ltd, Beach Energy Ltd, Origin Energy Ltd, etc., as peers. Hence, we give a ‘Buy’ recommendation on the stock at the current market price of $20.950, up by 6.345% on 6 April 2020.

2. Beach Energy Limited (Recommendation: Buy, Potential Upside: Lower Double-Digit)

Decent Production and Strong Balance Sheet: Beach Energy Limited (ASX: BPT) is engaged in exploration, development and production of oil and gas and investment in the resource industry. During 1H20, the company reported a production of 13.0 MMboe and drilled 105 wells with a success rate of 83%. BPT reported a strong financial performance with sales revenue of $900 million and an underlying EBITDA of $622 million. The company has a strong balance sheet position which provides flexibility to continue growth investment. These results reflect the robustness of Beach’s portfolio of assets. The decent financial and operational performance enabled the Board to declare an interim dividend of 1 cent per share.

Future Expectations: Despite the uncertainty in the global market with the fallout of Covid-19, the company is in the front foot when it comes to mitigating any potential material supply issues. FY21 free cash flow break-even oil price is projected to be less than US$0/bbl before growth investment and has lowered its EBITDA guidance to be between $1.175 – 1.250 billion. It has also re-affirmed its production guidance and expects it to be in the range of 27 – 28 mmboe. BPT is well-positioned to manage an extended period of low oil prices, as well as the impact of COVID-19..png)

Valuation Methodologies:.png)

.png)

Brent Crude Price vs BPT Price (Source: Thomson Reuters).png)

A-VIX vs BPT Price (Source: Thomson Reuters)

Stock Recommendation: As per ASX, the stock is trading close to its 52-weeks’ low level of $0.920, proffering a decent opportunity for the investors to enter the market. While Beach’s strong balance sheet means the company is well placed to continue growth investment, taking on account the current downturn, it is targeting up to a 30% deferral in FY21 capital investment relative to its prior planning. As depicted in the charts above, the stock price has been beaten down due to the COVID-19 impact accompanies by global outbreak of coronavirus, that has led to a massive destruction on oil demand. The price follows the footsteps of the international benchmark and may see an uplift as soon as the oil market recovers from the shock. As a result of the above pressure, the company lowered its underlying EBITDA guidance for FY20 and expects its production at the lower end of the guidance. The balance sheet of the company is in good shape, and the revenues are making the business resilient, to survive the turmoil. Considering the trading levels, resilient financials and strong fundamentals, we have valued the stock using P/E and P/Sales based market multiple valuation methods and have arrived at a target upside of lower double-digit (in percentage terms). Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $1.430, up 10.425% on 6 April 2020.

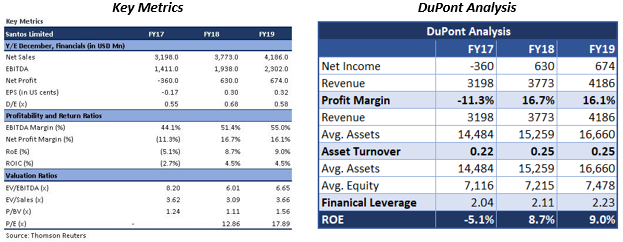

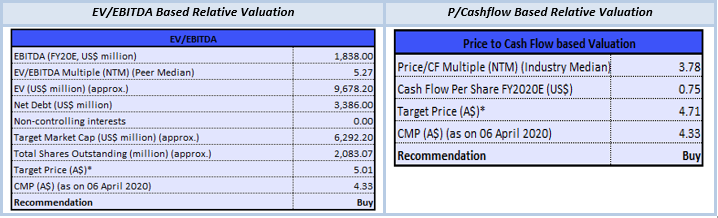

3. Santos Limited (Recommendation: Buy, Potential Upside: high single-digit to low double-digit)

Disciplined Operating Model and Increase in NPAT: Santos Limited (ASX: STO) is engaged in the exploration and the production of gas and petroleum, treatment and marketing of natural gas, crude oil, condensate, naphtha and liquid petroleum gas; transportation by pipeline of crude oil. The company supports the economic development of combined gas and renewable energy solutions. In 2019, the company has made significant investments for the deployment of renewable energy and recover waste heat across its operations. During FY19, the company reported record sales volume of 94.5 mmboe with a record production volume of 75.5 mmboe. In the same time span, the company witnessed a growth in revenue to US$4,033 million and an increase in net profit after tax to $674 million, up from US$630 million in FY18. The disciplined operating model of the company focused on low-cost efficient operations, has underpinned competitive advantage and framework for the continued generation of record and stable free cash flows of US$1,138 million.

What’s on the horizon: The company is confident in the business continuity and is focused on maintaining a strong balance sheet and increasing operating cash flow through improvements in productivity and discipline around capital expenditure. Whilst the current oil price dynamic is challenging, the eventual recovery in the market is likely to create opportunities for the company. The company is in control of its capex profile and has a liquidity of $3.1 billion.

Valuation Methodologies:

*1USD = ~1.66 AUD (as of 6 April 2020)

Brent Crude Price vs STO Price (Source: Thomson Reuters)

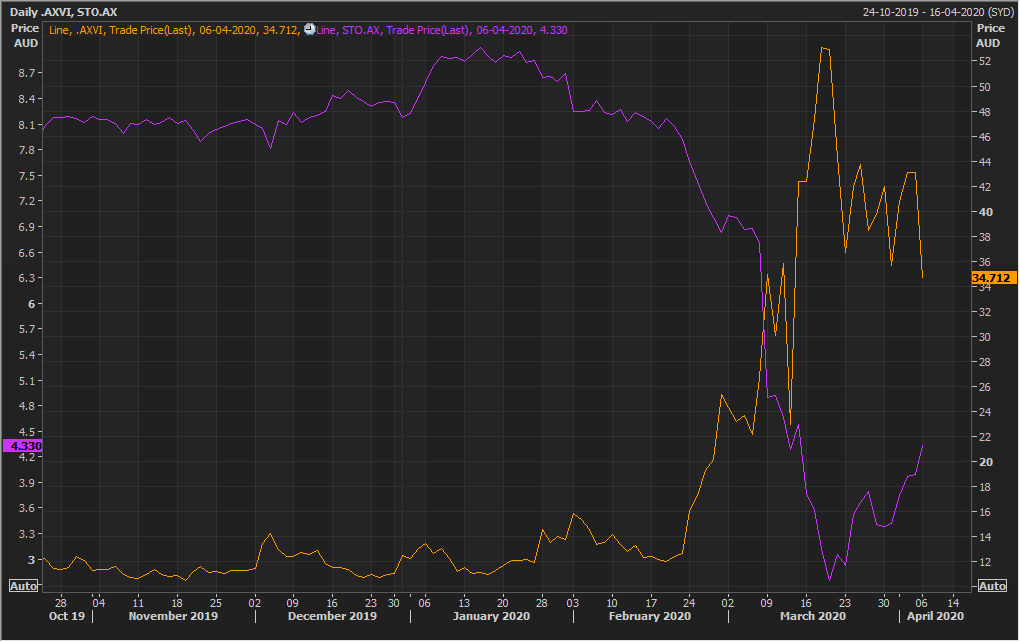

A-VIX vs STO Price (Source: Thomson Reuters)

Stock Recommendation: As per ASX, the stock of STO is attractively priced close to its 52-weeks’ low level of $2.730. The stock price is well aligned with the Brent crude price index, suffering equally from the latest damage to the energy sector. Moreover, the price has also reacted due to the highly volatile market due to COVID-19, going down at a high rate as the volatility index skyrocketed. However, a resilient business may support a speedy recovery as market conditions improve. The company is likely to benefit from the cash flows generated from the acquired business. It has sufficient headroom for debt covenants and is not under a major threat at current oil prices. Despite the uncertain economic impact of COVID-19 combined with the volatile oil price, STO is evolving rapidly with a resilient business position. Considering the trading levels, decent financial position and positive long-term outlook, we have valued the stock using EV/EBITDA multiple and price to cash flow multiple based relative valuation methods and have arrived at an indicative target price offering an upside of high single-digit to low double-digit (in percentage terms). For the said purposes, we have considered Senex Energy Ltd, Woodside Petroleum Ltd, Oil Search Ltd etc. as peers. Hence, we recommend a ‘Buy’ rating on the stock at the current market price of $4.33, up by 8.521% on 6 April 2020.

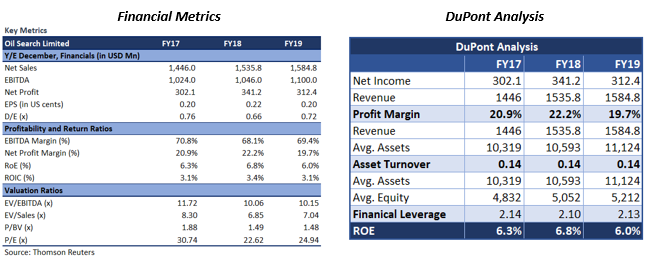

4. Oil Search Limited (Trading Halt)

Excellent Growth Opportunities and Ability to Create Shareholders’ Value: Oil Search Limited (ASX: OSH) is engaged in the exploration, development and production of oil and gas resources, with 98% of the Company assets in Papua New Guinea. The company has a PNG Biomass project, which is designed to provide domestic low-emission renewable energy to the Ramu Grid and is targeting a Financial Investment Decision for the project in mid-2020. The company has a PNG Biomass project, which is designed to provide domestic low-emission renewable energy to the Ramu Grid and is targeting a Financial Investment Decision for the project in mid-2020. During FY19, the company produced a total of 27.9mmboe, 11% higher than 2018, at an average realized oil and condensate price of US$62.86/barrel. This was driven by an excellent performance from the PNG LNG Project. Weaker realized oil and LNG prices, along with higher production costs, resulted in NPAT of US$312 million during the half-year. The company possesses a world-class asset base, excellent growth opportunities and a proven ability to create shared value. The decent financial and operational performance enabled the Board to declare a dividend of 9.5 US cents per share.

What to Expect: The company is analyzing more options for project financing for the LNG expansion development and is rationalizing its capital spending. It is focusing on the highest quality exploration prospects, including opportunities which have the potential to improve the economics of existing and planned LNG infrastructure.

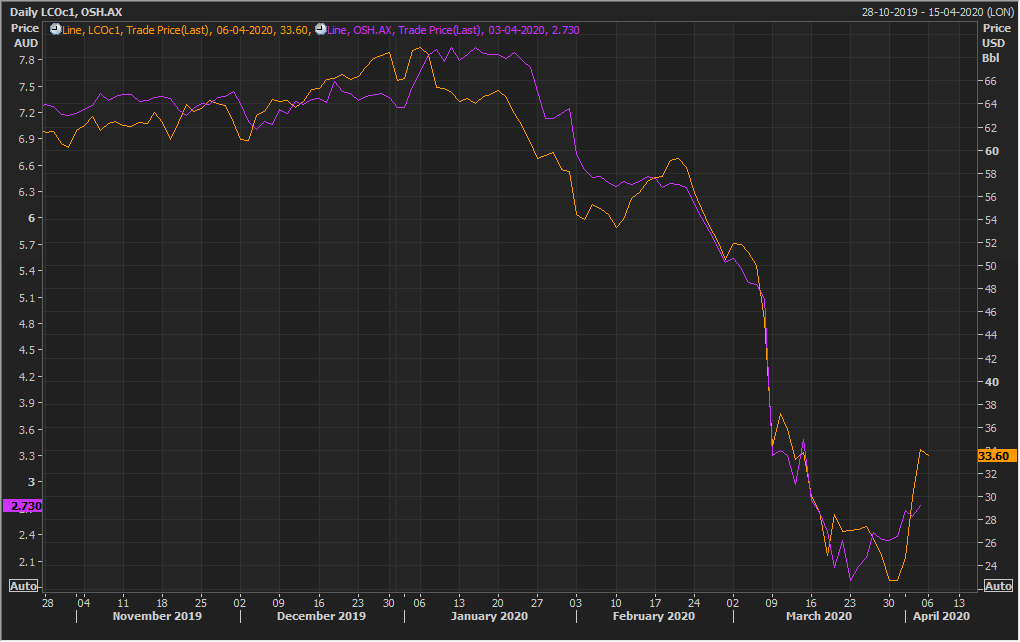

Brent Crude Price vs OSH Price (Source: Thomson Reuters)

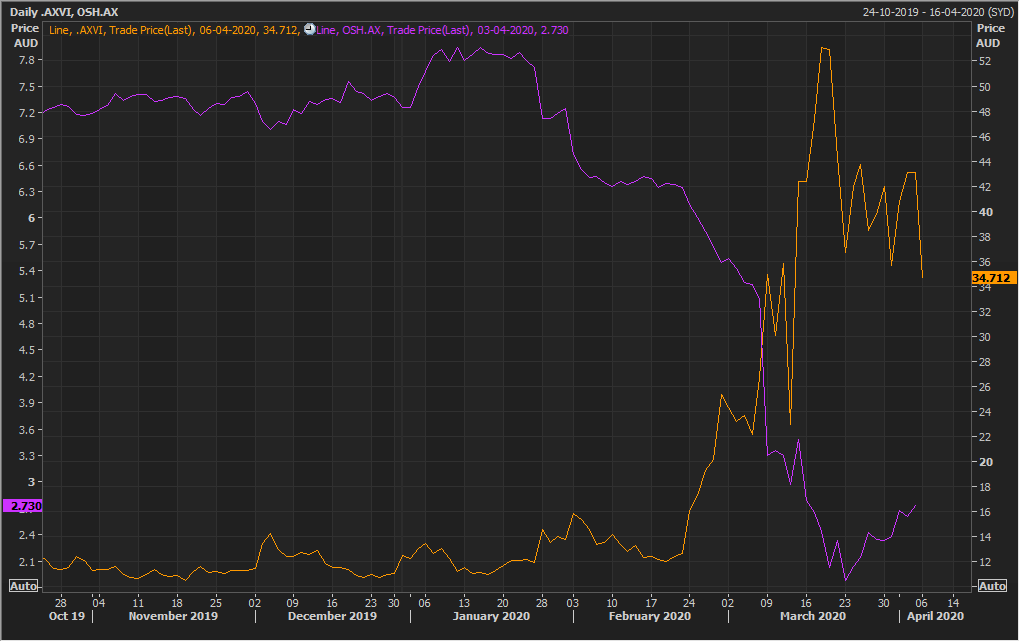

A-VIX vs OSH (Source: Thomson Reuters)

Stock Details: As per ASX, the stock of the company has been put on trading halt due to an awaited announcement regarding a capital raising. Trading is expected to commence on 14th April 2020 or on the release of the said announcement, whichever is earlier. The stock price witnessed a steep fall after the price war between Saudi Arabia and Russia left the oil market stuttering. Looking at the first chart, OSH’s stock price has been almost in line with the Brent crude oil benchmark index and is capable of a speedy recovery with a brilliant business profile. However, the stock has been sensitive to the recent market volatility and has borne the burden of a steep fall in price. Despite the bloodbath in the equity market across the globe, the fundamentals of the company are strong, which will help it sustain the blow.

Note:

The above relative valuation implies a target price incorporating the key factors driving the business and indicate long term potential of the stock. Prices, however, remain subject to any short-term movements due to the impact of oil price and covid-19 on the business fundamentals.

All the recommendations and the calculations are based on the closing price of 06 April 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...