Company Overview: The Star Entertainment Group Limited, formerly Echo Entertainment Group Limited, operates in the gaming, entertainment and hospitality industries. The Company owns and operates The Star Sydney (The Star Sydney); Treasury Casino and Hotel, Brisbane (Treasury Brisbane), and Jupiters Hotel and Casino, Gold Coast (Gold Coast). The Company's segments include The Star Sydney, Gold Coast and Treasury Brisbane. The Star Sydney comprises The Star Sydney's casino operations, including hotels, apartment complex, restaurants, bars and night club. The Gold Coast segment includes Jupiters' casino operations, including hotel, theatre, restaurants and bars. The Treasury Brisbane segment includes Treasury's casino operations, including hotel, restaurants and bars. The Company also manages the Gold Coast Convention and Exhibition Centre on behalf of the Queensland Government. The Company also owns Broadbeach Island on which the Gold Coast casino is located..png)

SGR Details

Decent Fundamentals: The Star Entertainment Group (ASX: SGR) is a mid-cap gaming and entertainment group with the market capitalisation of ~$3.86 Bn as of 13 February 2020. It is primarily engaged in the management of integrated resorts with gaming, entertainment and hospitality services. In FY19, the company’s portfolio of high-quality tourism, entertainment and gaming assets continued to expand in the attractive local destinations of Sydney, the Gold Coast and Brisbane. This continued expansion together with robust domestic results and reset of the organisational structure places SGR for the next stage of its growth and development. The Star’s growth strategy has been helped by the development of its strategic alliance with Hong Kong-based joint venture partners, named Chow Tai Fook Enterprises (or CTF) and Far East Consortium (or FEC).

The company’s statutory NPAT amounted to $198 million, reflecting a rise of 33.7% YoY (after significant items). Its statutory earnings before interest, tax, depreciation and amortisation (or EBITDA) rose 14.1% YoY to $553 million (before significant items). These results were helped by an actual win rate of 1.38% in International VIP Rebate business compared to 1.16% in the previous year. SGR’s FY19 returned strong domestic gaming results. The increases in domestic revenue were supported by the gains in the market share at the Gold Coast and Brisbane along with growth in Sydney throughout slots and tables. Notably, domestic private gaming rooms in Sydney, rose 12.4% and compensated the main gaming floor, which was affected by the capital works. Based on the decent performance in FY19, the Board of Directors declared a fully franked final dividend of 10 cents per share. This summarized a total dividend payment of 20.5 cents per share (fully-franked) for full-year, which represents a payout ratio of 95% of statutory NPAT.

The company’s Board is of the view that organisational changes and cost management measures which were implemented in 2H FY19 would be positioning SGR to deliver high-quality results in the context of unfavourable macroeconomic environment as well as challenging market conditions, domestically and internationally. Hence, we have valued the stock used two relative valuation methods, i.e., P/E multiple and EV/EBITDA multiple and 5-year average P/E market multiples of ~19.74x to FY20E consensus EPS of $0.259 and arrived at a target price of lower double-digit upside (in percentage term). At CMP of $4.180, the stock of the company is trading at P/E multiple 16.14x of FY20E EPS..png)

Key Financial Highlights (Source: Company Reports, Thomson Reuters)

Top 10 Shareholders: The following image provides a broader overview of the top 10 shareholders in The Star Entertainment Group:.png)

Top 10 Shareholders (Source: Thomson Reuters)

Key Margins: The company’s net margin stood at 9.2% in FY19, which reflects an improvement on the YoY basis as in FY18 the figure stood at 7.1% and, therefore, it can be said that SGR has decent capabilities to convert its top-line into the bottom-line. SGR’s operating margin stood at 14.5% in FY19, which reflects a rise from FY18 figure of 13.8%. The company’s RoE stood at 5.3%, which reflects an improvement from the prior-year figure of 4.2% and, therefore, it can be said that SGR has been delivering decent returns to its shareholders. The company’s Debt/Equity ratio stood at 0.31x, which is lower than the industry median of 0.43x and, therefore, it can be said that SGR’s balance sheet is leveraged as compared to the broader industry. Generally, lower debt on the balance sheet reflects that the company’s balance sheet is stabilised, and it can focus on long-term growth prospects.

.png)

Key Metrics (Source: Company Reports)

Unaudited Trading Update from July 1 to October 21, 2019: For the period from July 1 to October 21, 2019, group domestic revenue rose by 1.5% on pcp, and there was growth in Sydney and Queensland. The company added that de-risking initiatives had been implemented, which includes annualised cost reductions amounting to around $45 million by the end of 1H FY 2020. The Star values partnership with Queensland government developed over the past years. The Star provided the Queensland Government with an investment proposal which has the capability of creating substantial tourism drivers for the Gold Coast that delivers value to the shareholders. At the same time, it creates economic value along with employment growth in the region.

There are three elements to the proposal, involving commitments around The Star Gold Coast Masterplan, and upgrades as well as expansions to GCCEC and The Sheraton Grand Mirage upgrade.

Decent Domestic Performance in FY19: With respect to Sydney, the company witnessed continued domestic growth as there was an increase of 3.1% in revenues and 5% in EBITDA. Also, operating costs witnessed a fall of 2.9% on the YoY basis, and the increased domestic volumes and higher wages were compensated by lower international gaming volumes. Notably, domestic revenue and domestic EBITDA witnessed a total CAGR of 6.3% and 7.3%, respectively. .png)

Domestic Performance (Source: Company Reports)

Coming to Queensland, the company witnessed continued growth as there was positive momentum in normalised and statutory net revenue and EBITDA. However, the operating costs witnessed a rise of 4.9% in FY19 due to higher wages, increased domestic and international gaming volumes, newly commissioned assets and prudent investment in initial service levels at the Gold Coast.

Decent Capital Management: The company managed to declare a final dividend amounting to 10.0 cents (fully franked). The full-year dividend came out to be 20.5 cents per share which is same on YoY basis. Resultantly, the payout ratio stood at 84% of the normalised NPAT (95% of the statutory NPAT) for FY19.

Over the last five years, the company has a decent track record of paying dividends consistently with decent payout ratios in the ambit of 53.6% to 122%. The annual dividend yield of the company is around 3.45% on a five-year average basis (FY15-19). At CMP of $4.18, the annual dividend yield of the company is at 4.87%, which is higher than the industry median of 3.6% (Hotels & Entertainment Services). This implies that the company has been delivering better returns to its shareholders as compared to the broader industry. This might help in attracting the attention of dividend-seeking investors.

Annually, the company establishes a financial budget and 5-year plan that reflects the setting of performance targets. Also, financial performance is monitored continuously in order to determine any variations from annual financial budgets as well as market expectations. The company stated that core business produces robust cashflow, which enables SGR to maintain low to moderate debt levels while allowing the shareholders to be paid dividends.

.png)

Dividend (Source: Company Reports)

What to Expect from SGR Moving Forward: SGR plans to improve and de-risk the returns throughout the group. The company’s priorities revolve around executing on Centre of Excellence operating model, delivering on the investment strategy, managing the competitive environment and improving capital efficiency. The company’s vision is to become an Australiaʼs leading integrated resort company. To achieve this, significant deployments have been done to develop new or improved venue facilities in all the primary markets. Additionally, revenue sources have been diversified, which could further strengthen the company’s financial position. The company is expecting normalised group EBITDA for 1H FY 2020 in the range of $300 million- $310 million. .png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: P/E Based Relative Valuation.png)

P/E Based Relative Valuation (Source: Thomson Reuters)

Method 2: EV/EBITDA Based Relative Valuation.png)

EV/EBITDA Based Relative Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

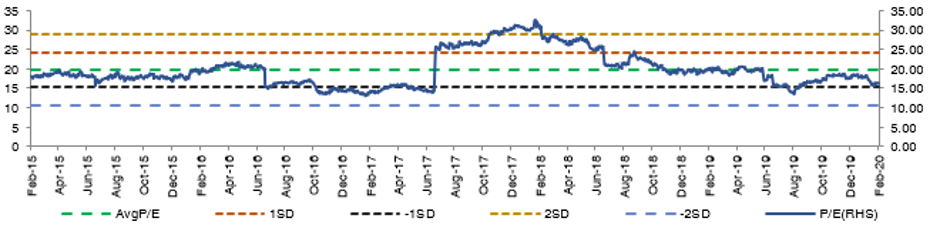

Historical PE Band (Source: Thomson Reuters)

Stock Recommendation: At the end of June 30, 2019, the group’s net asset position was in line with pcp and receivables were well managed. On July 3, 2019, the company refinanced the bank facilities, increasing total facility limit to $1.2 Bn and average drawn debt maturity to 5.3 years. Additionally, it was stated that the gearing levels help investment plans at 1.9 times FY2019 net debt to statutory EBITDA. This, along with refinancing the company’s bank facilities in the month of July 2019, places SGR well to continue to execute on the growth projects. The company’s operating cash flow before interest and tax amounted to $478.8 million, and an EBITDA to cash conversion ratio was 92%.

The company takes a structured approach for identifying, evaluating and managing the risks that have the potential to influence the achievement of strategic objectives. Therefore, there are expectations that SGR’s mitigations strategies might help the broader company and can help it to achieve long-term growth prospects. Hence, we have valued the stock used two relative valuation methods, i.e., P/E multiple and EV/EBITDA multiple and 5-year average P/E market multiples of ~19.74x to FY20E consensus EPS of $0.259 and arrived at a target price of lower double-digit upside (in percentage term). Based on the foregoing, we give a “Buy” recommendation on the stock at the current market price of $4.180 (down 0.713% on 13 February 2020).

.png)

SGR Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...