Company Overview: The Citadel Group Limited is engaged in the development and delivery of technology and education solutions to federal and state government departments and the private sector. The Company's principal activities consist of professional and managed services provision in the technology and education sectors throughout Australia. Its segments include Technology, which sells professional and managed services to government agencies and private enterprises; Education, which focuses on the delivery of a range of nationally-accredited business qualifications (including Advanced Diploma level) that enable students to articulate into second year university or to gain practical skills for employment, and Other, which includes corporate assets, such as investments in subsidiaries. The Company is engaged in providing vocational education, and training and supporting technology applications to empower learners (typically 17-24 years old) to achieve their individual education or employment goals.

.png)

CGL Details

Decent Contribution from SaaS to Revenues: Citadel Group Limited (ASX: CGL) is engaged in the provision of software and managed services in the technology sector throughout Australia. Majority of the company’s revenues are derived from long term managed services, software-as-a-service, and high quality strategic advisory services. The year ended 30 June 2018 was marked by multiple long-term contracts signed with government agencies for new cloud SaaS platform, Citadel-IX. The company continued to expand its capacity in e-health information management through acquisition of Charm Health International and Anaesthetic Private Practice, which involved a cost of $9.15 million and $2.08 million, respectively. In addition, the company also secured new significant projects due to the quality of work delivered. Revenue during the period was reported at $108.5 million, up 10% on the prior year. The company declared a fully franked final dividend of 9.0 cents per share, bringing total FY18 dividend to 13.8 cents per share.

Looking at the performance over the period covering FY14 to FY18, the company witnessed 21.4% top-line CAGR growth with FY14 revenue amounting to $49.93 million and FY18 revenue amounting to $108.52 million. Bottom-line CAGR growth over the same period stood at 36.4%, with FY14 and FY18 profits valued at $4.13 million and $14.30 million, respectively.

Going forward, the Management expects momentum from SaaS products to be continued ahead of a strong pipeline of opportunities. The second half period is likely to witness higher revenue flows on account of opportunities won in 1H period. With higher investment in SaaS and other facts, we are optimistic about the long-term prospects of the business.

.png)

Statutory Results (Source: Company Reports)

1HFY19 Performance Driven by SaaS: During the first half, the company reported total revenue amounting to $49.1 million, up 5.5% on prior corresponding period. EBITDA for the period amounted to $13.2 million, up 3.2% on prior corresponding period. Net profit after tax was reported at $6.7 million, representing an increase of 5.4% on prior corresponding period. During the period, the company witnessed an increase of 8.3% in earnings per share at 10.4 cents.

.png)

Key Financial Metrics (Source: Company Reports)

Factors Contributing to Change in Revenue: During the first half, the company provided its SaaS solutions to multiple clients, with SaaS revenue amounting to $16.8 million, up 39.1% on prior corresponding period. Increase in revenue was also attributable to benefits from cross selling to existing clients as well as implementation of new solutions. A reduction in revenue was also seen due to the impact of one-off projects and immaterial impact of the adoption of AASB15 on restatement of H1FY18.

Strong Balance Sheet Position: The first half was also characterised by a strong balance sheet supporting business investment and growth initiatives. As at 31 December 2018, the company had total cash of $16.0 million. Payments during the period comprised of total dividends of $5.7 million, $2.6 million in repayment of loans and $1.2 million paid in December 2018 for the acquisition of Gruden, with $0.4 million payable in March 2019. The period also witnessed a decrease in debt following amortisation of debt facility.

Cash Flow Position: Operating cash inflow during the first half increased by $1.5 million. Operating cash increased in comparison to prior corresponding period owing to more consistent tax instalments during 1HFY19. Net cash outflow from investing activities amounted to $4.3 million, representing payment made for the acquisition of Gruden. Financing cash outflow was reported at $8.4 million, representing payment of dividend and repayment of borrowings.

.png)

Cash Flows (Source: Company Reports)

Insight into SaaS: Growth during the first half was directly attributable to increased SaaS revenue and new product growth. The period saw increased investment in the SaaS platform to drive long-term sustainable growth. Along with progressing on growth in the domestic market, the company secured its first international client for Citadel-IX platform. In addition, the company developed vResponder, a product established to provide bureau services to first responder agencies, domestically and worldwide. SaaS revenue during the first half came in at $16.8 million, up 39.1% on prior corresponding period. The proportion of SaaS revenue was 34.2% in H1FY19 as compared to 16.3% in H1FY16.

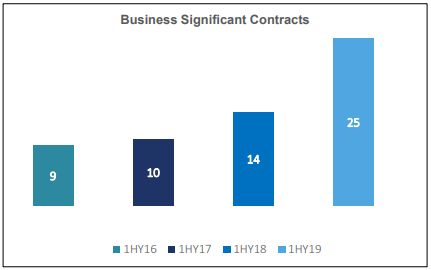

Significant SaaS Contracts Growth (Source: Company Reports)

Significant SaaS contracts have grown continuously, with 9 contracts in 1HFY16 to 25 contracts in 1HFY19 with an average tenure of contracts being more than 4 years.Customer and product base for SaaS expanded during the period through acquisitions of Anesthetic Private Practice (APP) and Gruden.

Acquisition of APP:In April 2018, the company completed the acquisition of Anaesthetic Private Practice, a cloud-based SaaS practice management and billing solution for the anesthetist market.

Acquisition of Gruden: The company acquired Gruden in December 2018, bringing in Procurement-as-a-Service as a new offering, with access to additional key government and telecommunications panels.

The company is now targeting to achieve 1 new customer per month for Citadel-IX, with a total of 200,000 users in FY20.

Recent Updates:

a. Shareholder Update: The company updated that the voting power of Montgomery Investment Management Pty Ltd increased from 5.03% to 6.06%.

b. Acquisition of Noventus: The company recently completed the acquisition of Noventus Pty Ltd, placing itself as a leading supplier to the Defence and National Security vertical. The transaction was funded from cash available with the company.

c. Appointment of Director: The company appointed Sam Weiss as an Independent Director on the Board. His tenure as a Director began on 15 May 2019. Sam holds 20 years of Board experience in Australia and Europe with exposure to technology, consumer products and education sectors.

d. Appointment of Company Secretary: Upon the resignation of Vanessa Chidrawi, the company appointed Spencer Chipperfield as the new Company Secretary. He has a total experience of 20 years working in complex organisations ranging from financial services to commodities trading.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 41.41% of the total shareholding. Jakeman Enterprises Pty. Ltd holds the maximum interest in the company at 13.69%, followed by Mcconnell holding 12.20% of the shares.

.png)

Top Ten Shareholders (Source: Thomson Reuters)

Key Metrics: During 1HFY19, the company reported an EBITDA margin of 22.2%, which improved in comparison to the prior corresponding period margin of 19.9%. Net margin for 1HFY19 fell slightly in comparison to pcp, from 13.8% in 1HFY18 to 13.7% in 1HFY19. Debt to equity ratio decreased in comparison to pcp from 0.27x to 0.19x.

.png)

Key Metrics (Source: Thomson Reuters)

FY19 Guidance: As per the recent trading update provided by the company, FY19 revenue is expected to be in the range of $97 million and $104 million. EBITDA for the year is expected to be in the range of $22 million and $24 million. The company expects gross profit margins to be around 46%. The provided guidance came in as a result of two factors, including, customer-controlled project extensions, which are now expected to commence after H1FY20 as compared to the timeline of H2FY19 provided earlier. The second factor was a lower increase in customer spend in Q4FY19 as compared to prior years.

Outlook: Despite the disappointing short-term results, the medium and long-term performance outlook remains decent on the back of consistent expansion of qualified sales pipeline, especially in the SaaS business. The company expects recurring revenues from SaaS products to witness continued growth, with the strongest ever pipeline of opportunities for SaaS products. This has placed the company in a strong position, which is expected to reflect in the second half of the year. Revenue from opportunities won in the first half is expected to flow H2FY19 onwards. In addition, the company is well-placed to support business investment and growth initiatives on the back of a strong balance sheet position. The company aims to drive long-term sustainable growth through increased investment in SaaS platform. The company is also expected to benefit from the ongoing and active M&A program in both domestic and international markets. The company is adding to its traditional consulting and managed services revenue base with a diversified portfolio of SaaS and other software revenue streams.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: P/E Based Approach:

.png)

P/E Based Valuation(Source: Thomson Reuters)

Method 2: Price to Cash Flow Approach:

.png)

Price to Cash Flow based Valuation (Source: Thomson Reuters)

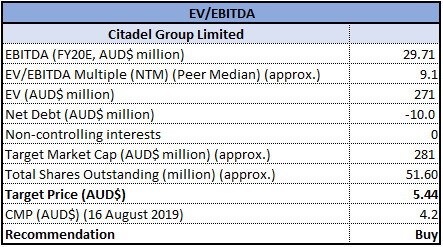

Method 3: EV/EBITDA Multiple Approach (NTM):

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated negative returns of 8.78% and 33.38% over a period of 1 month and 3 months, respectively. In 1HFY19, the company delivered another strong half year result supported majorly by accelerating growth in SaaS solutions. The period was characterised by a record level of recurring revenues from highly scalable SaaS solutions. To drive further growth, the company increased its investment in the development of SaaS platform. The company signed additional SaaS contracts across its key verticals of Government, National Security and Defence, Health and Education. The recent acquisition of Noventus is expected to be EPS accretive for the company, pre-synergies. Although, the company expected gross margins in FY19 to fall as a result of a delay in projects, the medium and long-term outlook remains decent with growth across the SaaS business. A combination of a diversified SaaS portfolio and other software revenue streams, coupled with new clients in Australia and overseas, set stage for the business to flourish in the future. With the above scenario in place, the Board expects to see strong growth momentum in FY20 across all areas of the business. Considering the above factors, we have valued the stock using three relative valuation methods, Price to Earnings, Price to cash flow and EV/EBITDA multiple and have arrived at a target price upside in the range of $5.21 to $5.58 (double-digit growth (in %)). Hence, we recommend a “Buy” rating on the stock at the current market price of $4.20, down 3.226% on 16 August 2019, ahead of its full-year results which are to be released on 20 August 2019.

.png)

CGL Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...