Company Overview: The Citadel Group Limited is engaged in the development and delivery of technology and education solutions to federal and state government departments and the private sector. The Company's principal activities consist of professional and managed services provision in the technology and education sectors throughout Australia. Its segments include Technology, which sells professional and managed services to government agencies and private enterprises; Education, which focuses on the delivery of a range of nationally-accredited business qualifications (including Advanced Diploma level) that enable students to articulate into second year university or to gain practical skills for employment, and Other, which includes corporate assets, such as investments in subsidiaries. The Company is engaged in providing vocational education, and training and supporting technology applications to empower learners (typically 17-24 years old) to achieve their individual education or employment goals.

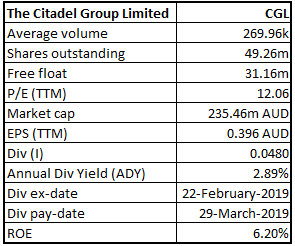

CGL Details

Growth Trajectory with Unique Offerings: The Citadel Group Limited (ASX: CGL) is engaged in the development, marketing, contracting and implementation of integrated knowledge management and enterprise software. The company has its core clients from varied industries including defence, immigration, health, education and government. Some of the offerings in its Software-as-a-Service (SaaS) product suite include Citadel-IX, vResponder, Kapish Productivity Suite, Evolution, CHARM, Anesthetic Private Practice (APP), and Gruden.

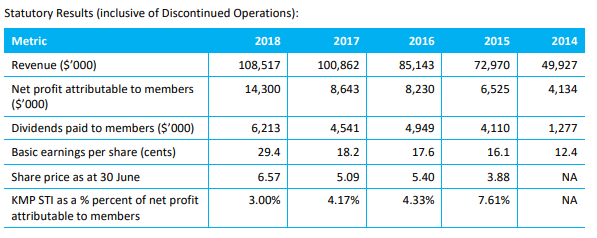

Looking into the growth trajectory of financial performance over a period of FY14 to FY18, it can be inferred that revenue generation increased from $49.93 million in FY14 to $108.51 in FY18. Net profit over the same period also increased from $4.13 million in 2014 to $14.30 million in 2018, reporting more than double growth over the period. Analysing the above data, the company witnessed a CAGR growth of 21.4% in top-line over FY14-FY18. And, the bottom-line witnessed a CAGR growth of 36.4% over the same period. Over the period, the company’s basic earnings per share increased from 16.1 cps in 2015 to 29.4 cps in 2018.

As charted in the second half of the year, the group intends to become a global Software and Services company, under the Citadel 2.0 strategy. It will mean an inevitable shift in the mix of margin as the change in the revenue model is embedded. The company now is combining its traditional consulting and managed services revenue base with a diversified portfolio of SaaS and other software revenue streams. The Management believes that the change in revenue mix along with the introduction of new clients both in Australia and Overseas, is likely to set the business up for success in the future. The management also expects the company to witness strong growth momentum in FY 2020, across all segments of the business.

FY14-FY18 Snapshot of Statutory Results (Source: Company Reports)

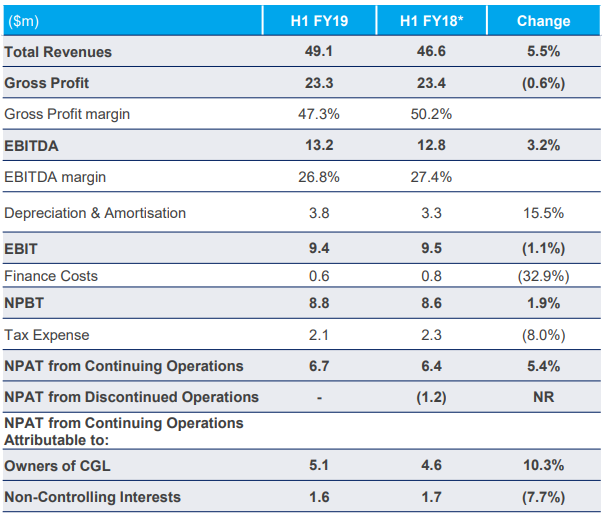

Accelerated Growth in SaaS Revenue in 1H19: For the six months ended 31 December 2018, the company generated total revenue amounting to $49.1 million, up 5.5% on prior corresponding period revenue of $46.6 million. SaaS revenue during the period amounted to $16.8 million, up 39.1% on pcp SaaS revenue of $12.1 million. The company reported a 3.2% increase in EBITDA at $13.2 million in 1HFY19 as compared to $12.8 million in the prior corresponding period. Net profit after tax attributable to members amounted to $5.1 million, up 10.3% on pcp. Considering the earnings profile, cash position and ongoing investment in growth initiative, the Board paid a fully franked interim dividend of 4.8 cents per share on 29 March 2019.

1HFY19 Income Statement (Source: Company Reports)

The period was marked by signing of new SaaS contracts in key verticals of Government, National Security and Defence, Health and Education. The contracts supported the development of secure cloud-based software solutions. The company witnessed new clients wins and cross-selling opportunities that led to a rapid increase in SaaS revenue. Proportion of revenue from SaaS increased from 16.3% in H1FY16 to 34.2% in H1FY19 and is anticipated to rise further. The company now has over 8 clients and 26,000 users for Citadel-IX with a target of 200,000 users in the financial year 2020.

Some of the major contracts signed during the period included:

(a) A 5-year contract with Queensland Health for chemotherapy management information system (CHARM).

(b) A 5-year eDRMS support agreement with a government client with 1,500 seats.

(c) A 9-year contract with the Queensland Department of Transport and Main Roads.

In December 2018, the company acquired Gruden that brought in Procurement-as-a-Service as a new offering in the portfolio, providing access to additional key government and telecommunications panels. The deal was closed at a consideration of $1.2 million.

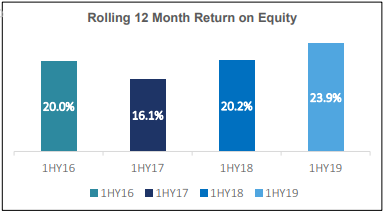

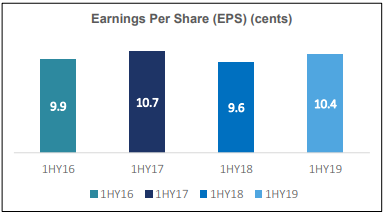

Ongoing Strong Returns: Over the period from 1HY16-1HY19, the company has witnessed a growth in earnings per share whilst investing in the business for future growth. EPS increased from 9.9 cents in 1HY16 to 10.4 cents in 1HY19. The company also depicted a rise in rolling 12-month return on equity to 23.9% in 1HFY19. These factors in conjunction reflect a strong cash position that underpins a strong dividend distribution profile.

Strong Returns During 1HFY16-1HFY19 (Source: Company Reports)

Overall, the half-year ended 31 December 2018 was characterised by a record level revenue generated from SaaS solutions. The company saw strong growth in new product deployments and associated managed services. 1H19 saw significant investments for the development of the SaaS platform for long-term sustainable growth. In addition, the company continued to expand its customer base across all key verticals.

Key Updates and Developments:

i.) The company recently updated the exchange that it had released 6,478 fully paid ordinary shares from voluntary escrow on 30 June 2019.

ii.) Key Personnel Changes: Citadel recently announced the appointment of Sam Weiss as an Independent Non-Executive Director on the Board, effective 15 May 2019. Meanwhile, Miles Jakeman resigned from the Board as a Director after serving a term of over four years. In March 2019, the company updated on Vanessa Chidrawi’s resignation from the position of Company Secretary and subsequent appointment of Spencer Chipperfield to the role.

iii.) During the financial year ended 30 June 2018, the company sold its Citadel Information Exchange (Citadel-IX) product to new government clients in New South Wales, Victoria and Queensland. The period also saw new contracts coming in as a result of continued quality of delivery in present engagements. Overall, the financial year 2018 was another year of record growth with strong margins and a pipeline for strong organic growth in the future.

iv.) Acquisitions of Noventus: Recently, Citadel acquired Noventus which was completed in May 2019. Noventus provides specialist capability with security clearances across systems engineering, integrated logistics support, project management, and systems integration and software development. The acquisition significantly increases the scale of Citadel’s Defence and National Security offerings. The acquisition involved a payment of $5.7 million as consideration.

v.) Acquisitions of Charm and Anaesthetic: In May 2018, the company acquired the business assets of Anaesthetic Private Practice Pty Ltd for a consideration of $2.1 million. The company owns a cloud-based practice management tool for the Australian Anaesthetic sector In September 2017, the company made another acquisition of Charm Health International Pty Ltd and its subsidiaries on payment of $9.1 million. Both the deals helped Citadel to align its existing offerings in electronic content management and cloud-based computing, which in turn, will help it to expand its current operations to support the growth strategy.

Key risks: Some of the material business risks that might adversely affect the financial performance of the company include – (a) loss or failure of key contracts to win new contracts, (b) claims for indemnities or damages in connection with key contracts, (c) failure to commercialise R&D expenditure, (d) disruption due to technological advance or product failures and, (e) inability to attract new talent with the increase in operational scale.

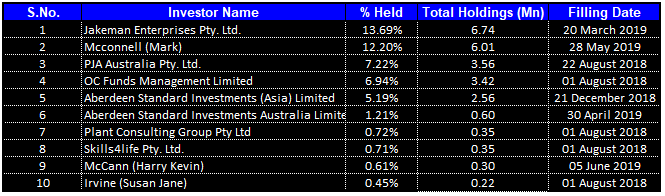

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table which together form around 48.92% of the total shareholding. Jakeman Enterprises Pty. Ltd and Mcconnell (Mark) hold the maximum interest in the company at 13.69% and 12.20%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

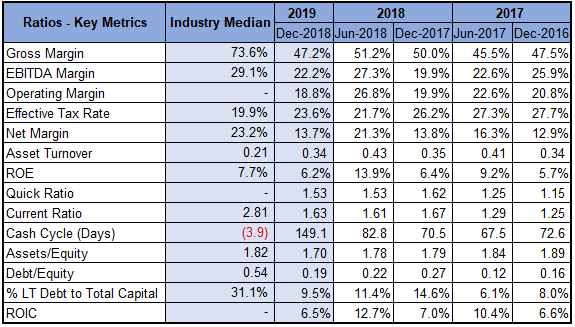

Key Metrics: The company posted an EBITDA margin of 22.2% in 1HY19 as compared to 19.9% in the prior corresponding period. Net margin for the period was broadly in-line with pcp at 13.7%.

Key Metrics (Source: Thomson Reuters)

Delay in Customer-Control Project Extensions led the Revised Guidance: The Board recently updated the expected range of revenue and earnings for the financial year 2019. Sales revenue for FY19 is now expected to be between $97 million to $104 million. The expected gross profit margin was reduced to 46% and EBITDA is anticipated to be in the range of $22 million and $24 million. The company changed the expected values for revenue and earnings as customer expenditure in the fourth quarter is not expected to rise as much as the previous years. In addition, the customer-controlled project extensions, planned for the second half of the financial year 2019, are now expected to begin after the first half of the financial year 2020. While the short-term results reflected a slowdown, medium-term and long-term outlook for the company’s performance remains decent.

Outlook: The company expects recurring revenues from SaaS products to experience continued growth. With a strong balance sheet, the company has the potential to make further business investments in the SaaS platform for long-term sustainable growth. The company expects the revenue from opportunities won in H1FY19 to be skewed to H2FY19. With a strong pipeline of opportunities for SaaS products with ongoing M&A program in domestic & international markets, the company expects to deliver strong results in the second half of the financial year 2019.

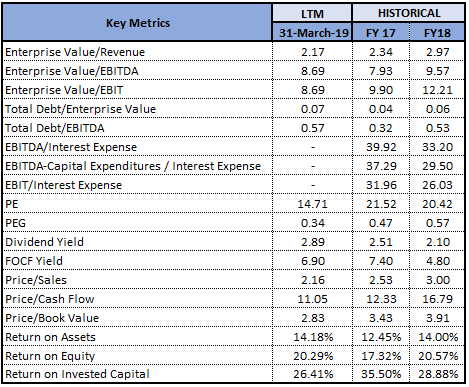

Key Valuation Metrics (Source: Thomson Reuters)

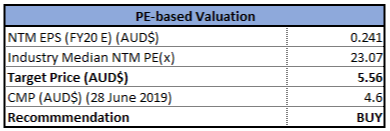

Valuation Methodology:

Method 1: PE- Based Multiple Approach (NTM):

P/E-Based Valuation (Source: Thomson Reuters)

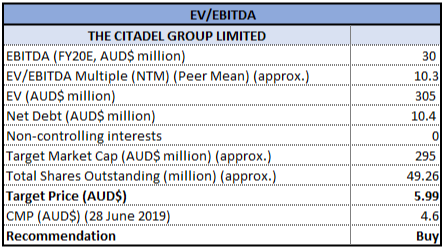

Method 2: EV/EBITDA Multiple Approach (NTM):

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated returns of 10.39% and -33.52% over a period of 1 month and 3 months, respectively. As depicted by the performance in 1HY19, the company is progressing well towards growth through investment for the development of the SaaS platform which helped to drive the financial performance in 1HY19. Over the period, customer base for Citadel-IX also increased rapidly with over 26,000 users in 1HY19 and a target of 200,000 in the next financial year. The recent acquisition of Noventus helped to boost the Defence and National Security offerings, which is a key strategic focus for Citadel. The company depicted a strong balance sheet and cash position with earnings per share rising from 9.6 cps in 1HY18 to 10.4 cps in 1HY19. Moreover, the company executed various acquisitions to further expand its offering and support its growth strategy. The returns from new opportunities taken up by the company in 1HY19 are expected to bring further growth in the future.

The recently revised guidance given by the management hit the stock price sharply. However, going forward, we are of the view that the forward-looking statements are already priced in at the current market price. Considering the business growth, product development, client addition, we have valued the stock using two relative valuation methods, PE and EV/EBITDA multiple and arrived at the target price of the stock in the range of $4.6 to $5.9 (double-digit upside (%)). Hence, we recommend a “Speculative Buy” rating on the stock at a current market price of $4.600, down 3.766% on 28 June 2019.

CGL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...