Kalkine has a fully transformed New Avatar.

Company overview - T.F.S. Corporation Ltd is principally engaged in the manufacture, sale, distribution, management, ownership and promotion of sandalwood plantations. The Company's segments include Plantation Management, Finance, Sandalwood Products and Pharmaceutical. The Plantation Management segment is responsible for the promotion and sales of Indian sandalwood lots to investors, called growers. The Plantation Management segment is also responsible for the establishment, maintenance and harvesting of Indian sandalwood plantations on behalf of the growers and group owned plantations. The Finance segment is responsible for providing finance to growers to purchase sandalwood lots. The Sandalwood Products segment is responsible for the manufacture of sandalwood oil and products for resale both domestic and internationally. The Pharmaceutical segment is located in the United States and is responsible for research and development of pharmaceutical and biopharmaceutical products for commercializing.

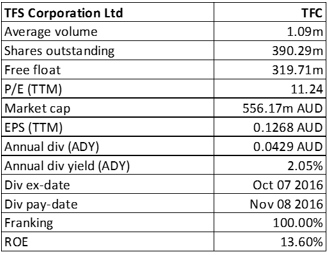

TFC Details

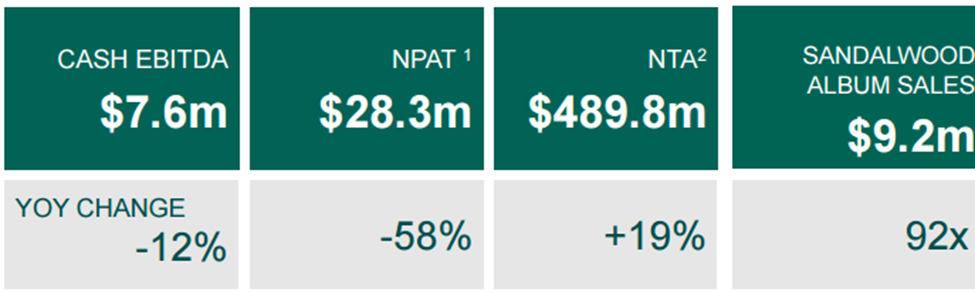

Robust growth in Indian sandalwood sales: TFS Corporation Limited (ASX: TFC), which is the world's largest owner and manager of commercial Indian sandalwood plantations, had a significant ramp-up in sales of processed Indian sandalwood oil and wood. The sales grew exponentially to 92x in 1H 17 on 1H FY16. The cash revenue surged 7.4% to $65.2 million during the period as compared to $60.7 million in the prior corresponding period. This growth was due to the commencement of deliveries of processed wood and oil from TFC’s major 2016 harvest to the company’s customers in China, the US, and Europe. These product sales commenced in late September and ramped up in Q2 FY17, with sales expected to accelerate further in H2 FY17. The revenue grew on the back of the plantation management services offered to plantation owners coupled with the ongoing growth (up 8%) in the average plantation establishment fee per hectare. The plantation sales grew 32% during the period. However, the non-cash revenue fell 12% to $87.4 million during the period from H1 FY16 ($99.3 million). This is due to a lesser tree valuation gain, because of a less favorable exchange rate gain, and an increased tree maturity with a shorter period to harvest, and larger directly-owned estate and deferred plantation management fees that grew by 28% to $19.7 million due to the larger managed estate. Moreover, in the first half of 2017, the net profit after tax was $28.3 million as compared to $67.4 million in H1 FY16. The fall in the profit was driven by lower non-cash foreign exchange gains on tree valuations, the absence of a $17.2 million accounting gain on the Santalis acquisition that had increased the H1 FY16 result, and a $10.6 million one-off early call premium in H1 FY17 associated with the successful refinance of the company’s senior secured notes. Meanwhile, TFC has also experienced higher operating costs in relation to its larger plantation estate and harvest, from which the TFC would benefit through the increased wood and oil sales in future years.

1H 17 Financial and Operational Performance (Source: Company Reports)

2017 expected to be a transformational year: The group believes that this year would be a transformational year as the company sold commercial quantities of Indian sandalwood oil and wood from the first large scale commercial harvest. The benefits of that transformation are now starting to be realized by TFC. The harvest of the own sandalwood completed in August 2016 and the tender to buy grower-owned wood was secured in November 2016. The company’s focus has been firmly on executing the sales and distribution strategy to monetize the huge rise in available wood and oil. Moreover, TFC has booked $2.0 million of album (Indian sandalwood) sales in Q1 FY17 and $7.1 million of sales in Q2 FY17, and the company expects H2 FY17 to easily outpace those figures as TFC is ramping-up sales to existing customers, optimizing the supply chain and start delivering on new contracts signed last year. Furthermore, the addition of a supply contract with the world’s largest natural oil company, Young Living, to the company’s stable of oil customers, as well as the wood buyers in China and the Middle East, ensures the vast majority of oil and wood from the harvests for the next five years are forward sold to the multiple markets.

Considerable progress at Santalis: TFC’s US-based pharmaceutical subsidiary, Santalis, is awaiting allowance from the FDA to enter the Phase 3 trials for their HPV wart product, as well as is progressing with four Phase 2 trials of other products, which treat skin conditions using sandalwood album oil. The studies of the ongoing Phase 2 trials are expected to be completed from mid calendar 2017. Additionally, TFC’s Board and management are currently assessing how to unlock best value for TFC shareholders from the considerable progress that Santalis is achieving.

Capital Management efforts: TFC’s cash balance was $89.8 million as at December 31, 2016, which is a 72% growth on $52.1 million at December 31, 2015. Moreover, at December 31, 2016, TFC owned biological assets were valued at $685.0 million, which grew 10% on June 30, 2016. The valuation methodology for TFC’s biological assets has remained unchanged. To enhance its efficient capital management, TFC has negotiated Heads of Terms, which are subject to contract, for a new working capital facility with one of the world’s largest banks. This includes the facility size of A$35 million, with a two-year tenor, at favorable terms to lower the existing cost of debt and the minimal maintenance covenants. The new facility will not be utilized for cash drawings during FY17 but would add a further lever to enhance the efficient management of capital. This agreement is a significant milestone and the first banking support for TFC since the GFC and the collapse of the MIS industry. In addition, the multi-option revolving capital facility would assist the group to efficiently manage its cash-flow (without retaining excess cash on its own balance sheet) as most of the plantation sales occur in a small window, late in Q4 FY 17.

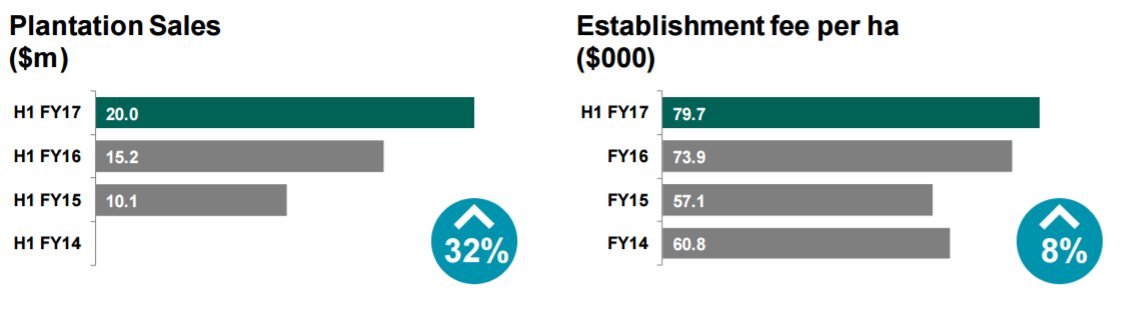

Plantation Sales (Source: Company Reports)

Rebranding of TFC as Quintis Limited: TFC intends to rename to Quintis Limited, as part of the process approved by shareholders at the AGM in November 2016. The new Quintis brand and website is expected to be launched on March 22, 2017; and, from March 23, 2017, Quintis Limited will trade under the ASX code “QIN”. Furthermore, the launch of Quintis will mark a major juncture in the evolution of the company from a forestry company to a global producer of one of the world’s most-rare and valuable super-ingredients. In addition, TFC would launch the Quintis ingredient mark, which will be a guarantee of the world’s purest and most potent sandalwood album.

FY 17 Outlook: TFC has reaffirmed its guidance for FY17 cash EBITDA to increase by at least 25% on FY16, as plantation and product (wood and oil) sales continue to gather pace in the second half of the year. TFC has recently commenced its first sales to the Middle East, and later this financial year 2017 would finish first sales to India and increase volumes to China. Additionally, TFC expects the total product sales (wood and oil) to be in the range of $45 million to $55 million for the full financial year 2017, which is a significant increase on the prior year (FY16: $29.9 million). The product sales include the sales of the sandalwood spicatum oil (Australian sandalwood), which the company processes and sells pursuant to a supply contract with the West Australian state government. However, the sales of spicatum were down by 43% to $6.3 million in H1 FY17 mainly hurt by the market disruption related with the delayed finalization of a new 10-year (to 2026) supply contract. Meanwhile, spicatum sales are expected to return to traditional sales levels later in calendar 2017, while they are expected to remain subdued during the remainder of FY17. Additionally, TFC also expects to establish a further 1,400 hectares of plantings in FY17, which is to be finished in the northern Australia dry season and that would grow the total TFC-owned and managed estate to over 13,000 hectares. This would further cement the company’s position as the largest owner of Indian sandalwood plantations in the world.

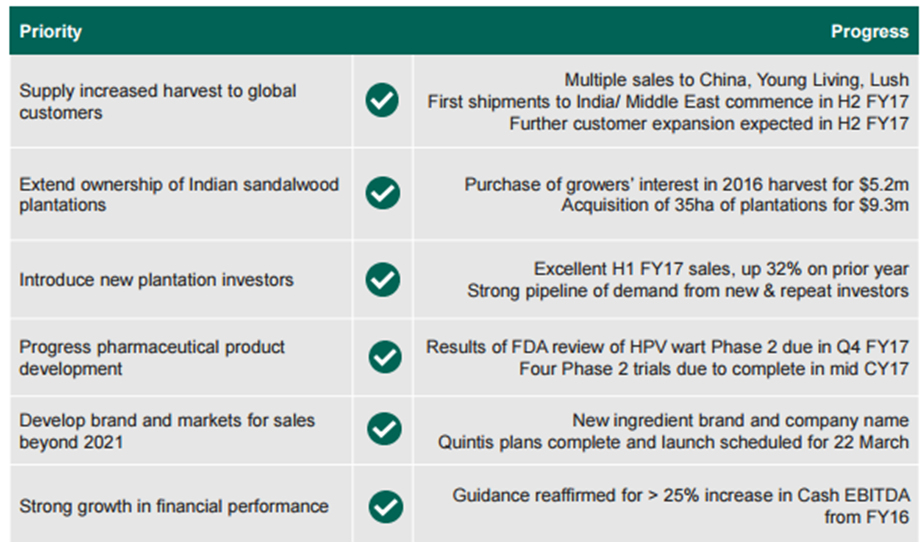

Progress against FY17 priorities (Source: Company Reports)

Stock Performance: TFC stock fell about 12% in the last three months (as of March 06, 2017) and now trades at a reasonable level. The company expects positive operating cash flows for the full year FY17, consistent with FY14, FY15, and FY16, reflecting the seasonality of the business as plantation are heavily weighted to the second half. Moreover, the strong ramp-up in product sales is expected to continue in the second half of 2017 and would contribute to a transformational FY17 result for TFC. The group continues to grow its plantation estate and is successfully realizing on the tenfold increase in harvest size. We give a “Buy” recommendation on the stock at the current price of – $ 1.46.png)

TFC Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...