Company Overview – As Australia’s leading provider of telecommunications services, Telstra offers services across voice, mobile, data and internet products, with dominant or significant market share in each service category. Telstra will withdraw from running the infrastructure in wholesale fixed line voice and broadband after the fibre rollout and will be compensated accordingly. It has a growth strategy incorporating mobiles, network applications and services, and digital media, leveraging superior networks and strategic digital media assets. The Company operates in nine segments: Telstra Consumer and Country Wide (TC&CW); Telstra Business (TB); Telstra Enterprise and Government (TE&G); Telstra Wholesale (TW); Telstra Media Group; Telstra International Group; TelstraClear; Telstra Operations and Other.

Analysis – TLS’s recent outperformance was due to asset sales. Now sitting on a cash war chest, the debate turns to capital allocation. We think an increased dividend and acquisitions will result, but caution investors about any potential acquisition in network application space, as it would be dilutive for TLS’s returns.

The telecommunications sector is highly dependent on the regulatory environment and technological change. Fixed line revenue decline continue to be driven by lower voice usage and fixed to mobile substitution. In addition fixed line margins and profitability will come under pressure from NBN, offset by disconnection/lease/other government payments TLS will receive under the current $11 Billion NBN deal. Despite mobile voice penetration peaking, industry growth should benefit from 3G-4G migration and an explosion in mobile data traffic. However a future lift in mobile pricing competition remains a risk.

Telstra has signed a non-binding memorandum of understanding with Telkom Indonesia to create a joint venture or JV that will provide network services in Indonesia. The proposed JV will be the exclusive provider of network application and services or NAS, in Indonesia for both companies. Although in isolation this is a small event for Telstra, the deal highlights one of the ways Telstra can deliver on its Asian growth strategy. Partnership with local players could provide Telstra a lower risk alternative to acquisitions which are also likely to form a part of the expansion strategy. That said these partnerships are slow burn opportunities that are unlikely to deliver a material earnings contribution in the short to medium term.

Telstra has significant balance sheet capacity with the ability to fund new investment in Asian as well as capital management initiatives. National broadband network or NBN payments over the, medium term will bolster Telstra’s cash reserves, adding to proceeds from asset sales that are expected to complete in late fiscal 2014.althoughg acquisitions and investment in Asia may lower cash return to investors in the short term, additional cash flow from new investments could help fund a sustainable increase in annual dividends payments in the long term. Securing Telkom Indonesia as a JV partner is a positive outcome for Telstra in our opinion. Telstra has significant experience and a strong track record delivering NAS technology and cloud services in Australia but lacks a footprint and customer base in Asia.

Telstra announced the sale of CSL New World to HKT Ltd for US$2.425Billion on 20 December 2013. It said its 76.4% stake would realize around A$2.0 billion depending on currency movements between now and likely completion around the end of 3Q14. CSL performed well in FY12 and FY13 and set to improve in FY14 on the basis of good subscriber growth and LTE coverage with reported results boosted by a falling AUD. As well CSL is a world leading 4G carrier on the doorstep to china, just as china has issued 4G licenses to its three incumbent mobile carriers and opened the mobile market to Chinese owned mobile virtual network operators (MVNO’s). We think it is the right time for Telstra to sell CSL. From its current position the company will find it more difficult to maintain high levels of domestic revenue growth in a circumscribed market.

Telstra also noted the listing in the US of Autohome Inc (“Autohome”), a Chinese online site for automobile sales to consumers and one of Telstra’s key Chinese digital media assets. Telstra is the majority shareholder in Autohome, with a 71.5% stake pre IPO and around 66.2% post IPO. Telstra did not sell any of its shares into the initial public offering.

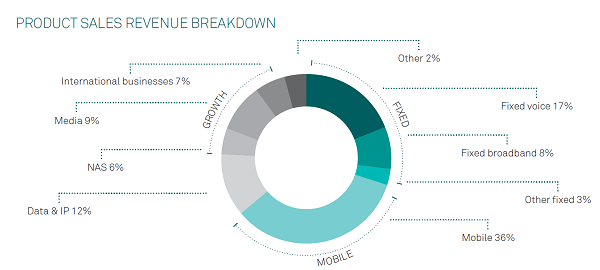

Source - Company Reports

|

Price |

Price % Change |

|

Close: |

5.01 (06-Feb-2014) |

3M: |

(2.72%) |

|

52 Wk High: |

5.30 (07-Jan-2014) |

6M: |

0.00% |

|

52 Wk Low: |

4.44 (13-Mar-2013) |

1Y: |

7.97% |

Telstra also announced the sale of 70% of Sensis excluding voice based directory services and the Trading Post. The sale to Platinum Equity, a US based private equity firm realized A$454 Million implying a value of Sensis of A$649 Million. As with CSL the sales of Sensis adds to Telstra’s medium term revenue growth and margin enhancement. Telstra has retained aspects of advertising, including mobile advertising where it has potentially better synergy and prospects for growth and margin. We consider both sales reflect positively on the company in part because of the good value realized by CSL. Both remove businesses that were likely to dilute earnings growth on a medium term outlook and inhibit the company’s ability to grow ordinary dividends.

|

Dividend |

|

|

|

|

Yield |

5.870021 |

FY |

Payout Ratio |

91.24049 |

FY |

|

|

7.782101 |

5yr Av |

|

94.42543 |

5yr Av |

Source - Company Reports

|

TLS (AUD, Millions) |

2013 |

2012 |

2011 |

2010 |

2009 |

|

Total Revenue |

25,980 |

25,503 |

25,304 |

25,029 |

25,614 |

|

Total Operating Expense |

20,498 |

20,569 |

20,747 |

19,491 |

19,956 |

|

Operating Income |

5,482 |

4,934 |

4,557 |

5,538 |

5,658 |

|

Net Income After Taxes |

3,865 |

3,424 |

3,250 |

3,940 |

4,076 |

|

|

Industry Median |

2013 |

2012 |

2011 |

2010 |

2009 |

|

Profitability |

|

|

|

|

|

|

|

Gross Margin |

66.2% |

75.0% |

75.5% |

75.3% |

78.4% |

79.1% |

|

EBITDA Margin |

29.5% |

41.7% |

41.0% |

39.7% |

44.2% |

42.9% |

|

Operating Margin |

13.7% |

21.1% |

19.3% |

18.0% |

22.1% |

22.1% |

|

Pretax Margin |

10.1% |

21.5% |

19.5% |

18.2% |

22.3% |

22.3% |

|

Earning Power |

|

|

|

|

|

|

|

Pretax ROA |

7.5% |

14.0% |

12.7% |

11.8% |

14.0% |

14.5% |

|

Pretax ROE |

15.4% |

45.5% |

41.9% |

36.8% |

44.1% |

46.3% |

|

Liquidity |

|

|

|

|

|

|

|

Quick Ratio |

0.79 |

0.99 |

0.91 |

0.80 |

0.79 |

0.77 |

|

Current Ratio |

0.81 |

1.05 |

0.93 |

0.83 |

0.83 |

0.80 |

|

Leverage |

|

|

|

|

|

|

|

Assets/Equity |

2.10 |

3.06 |

3.44 |

3.14 |

3.09 |

3.22 |

|

Debt/Equity |

0.31 |

1.19 |

1.33 |

1.17 |

1.17 |

1.39 |

Protection is built into the agreement between NBN and Telstra which should limit downside risk to compensation payments if the roll out is restructured. Any share price weakness as a result of uncertainty could provide an opportunity to enter the stock. The premium mobile network supports a robust mobiles business and well supported by network, application and services and digital media. Solid operating and free cash flow will be generated from the operating businesses and defined compensation payments. We will be putting a HOLD on TLS.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...