Kalkine has a fully transformed New Avatar.

Company Overview: Tassal Group Limited (ASX: TGR) is primarily engaged in the farming of Atlantic Salmon and Tiger Prawns and the processing and marketing of salmon, prawns and other seafood. The company has a thriving and sustainable seafood business, supported by a strong management team and attractive market conditions. The company is continuously pursuing its salmon growth strategy and is focused on strategic investments in prawns, to deliver long-term growth in earnings and returns.

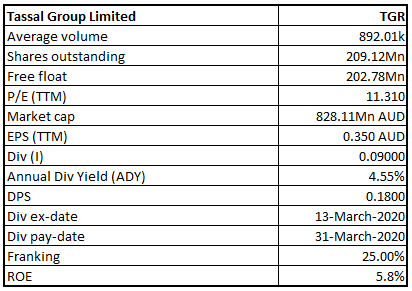

TGR Details

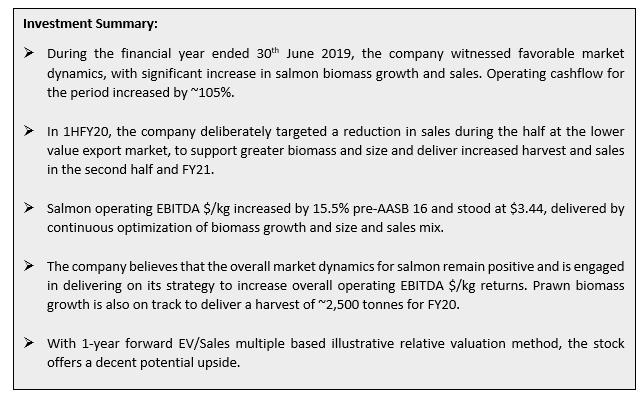

Continued Focus on Increasing Operating EBITDA $/kg for Salmon and Prawns: Tassal Group Limited (ASX: TGR) is primarily engaged in the farming of Atlantic Salmon and Tiger Prawns and the processing and marketing of salmon, prawns and other seafood. During the financial year ended 30th June 2019, the company witnessed favorable market dynamics, with significant increase in salmon biomass growth and sales, along with a positive pricing environment, delivering a robust increase in operating earnings. The period ended with another record result across key financial metrics, with salmon revenue and EBITDA rising by 19.9% and 14.5%, respectively. The company witnessed continued growth in the core salmon domestic market, along with attractive prospects in the export market for larger fish.

In FY19, the company reported an increase of 104.9% in operating cashflow to $89.9 million, on the back of a strong underlying business and operational strategy. This, in turn, backs the company’s strategic investment in salmon biomass and capital infrastructure to deliver continued long-term returns. Investing cashflow for the period amounted to $138.7 million, representing growth investment across salmon and prawns. During the year, the company declared a dividend of 18 cents per share.

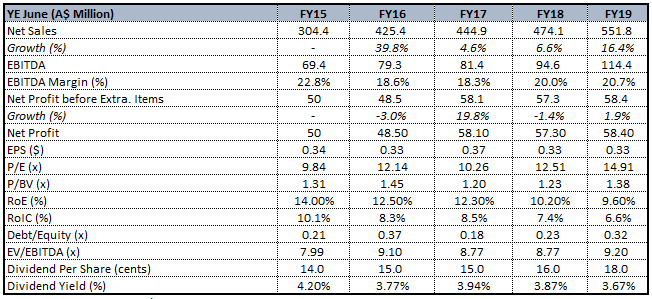

5-Year Results (Source: Company Reports; Thomson Reuters)

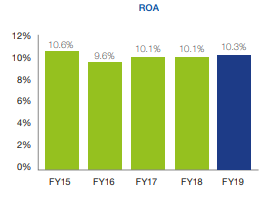

The company is focused on responsible working capital and capital spending to deliver sustainable long-term returns. Over the last five years, the company’s investments in growth have demonstrated stable financial returns. The company’s entry into prawns with the acquisition and redevelopment of Fortune Group in September 2018, marked the beginning of diversification and is expected to underpin strong earnings over the short to medium term. In FY19, operating return on assets stood at 10.3%, with earnings from prawns yet to materially flow through.

Return on Assets (Source: Company Reports)

In 1HFY20, the company continued to deliver on its core salmon operational strategy and progressed on its prawn growth strategy, for better earnings and returns in FY20 and beyond. The company was focused on increasing operating EBITDA $/kg for both salmon and prawns through optimising biomass growth to generate cost efficiencies, and optimising sales mix across higher margin markets and products. During the half, salmon EBITDA $/kg increased to $3.44, representing an increase of 15.4% on $2.98 reported in the prior corresponding half.

In 2HFY20, the company is focusing on capitalising on the greater biomass and size in 1HFY20, by delivering increased harvest and sales during the second half and FY21. While the company cannot predict the change in consumer behavior due to COVID-19, it believes that overall market dynamics for salmon remain positive. Early trends in consumer behavior have been favorable, which will help the company in driving consumption per capita of salmon and prawns with the right strategy in place.

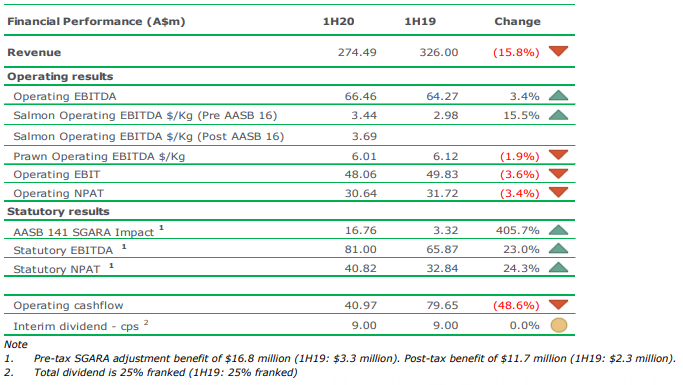

Highlights for the Half Year Ended 31st December 2019: During the half, revenue stood at $279.49 million, down 15.8% on pcp revenue of $326 million. The company deliberately targeted a reduction in sales during the half at the lower value export market, to support greater biomass and size and deliver increased harvest and sales in the second half and FY21. Operating EBITDA for the period amounted to $66.46 million, up 3.4% on pcp. Salmon operating EBITDA $/kg increased by 15.5% pre-AASB 16 and stood at $3.44, delivered by continuous optimization of biomass growth and size and sales mix. Operating NPAT for the period stood at $30.64 million, down 3.4%. Whereas, statutory NPAT went up by 24.3% and stood at $40.82 million. During the half, the company declared an interim dividend amounting to 9 cents per share, in line with the prior corresponding half.

1HFY20 Results Snapshot (Source: Company Reports)

Funding for Long-Term Growth: During the half, operating cash flow went down by 48.6%, as the company left salmon and prawns to grow in water to feed and drive harvests and sales in the second half. Cashflow was also impacted by lower salmon export sales of $36.7 million. However, the operating cashflow was enough to fund the company’s biomass capital and infrastructure for salmon and prawns. To strengthen its financial position and ensure continued delivery on its long-term growth strategy, the company raised $125.8 million through a placement and share purchase plan amounting to $108.4 million and $17.4 million, respectively. Out of the investing cashflow of $96 million, salmon growth capex amounted to $21.7 million and salmon maintenance capex came in at $17.2 million. Prawn growth and maintenance capex for the period amounted to $28.1 million and $1.5 million, respectively.

In the second half of the year, the company has witnessed positive trends for the business, with salmon biomass growth exceeding expectations and providing prospects for increasing overall operating EBITDA $/kg returns. The company is transitioning supply for the continuation of more sales into the domestic market and is focusing on more profitable product lines in the domestic market, keeping the export market as a destination for surplus volume. Moreover, it is considering the optimization of existing leases and cost of growing reduction initiatives over the short to medium term. This, in turn, will support the delivery of higher salmon returns in FY21 and beyond.

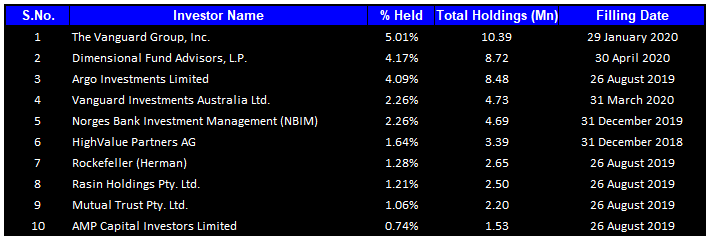

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 23.71% of the total shareholding.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

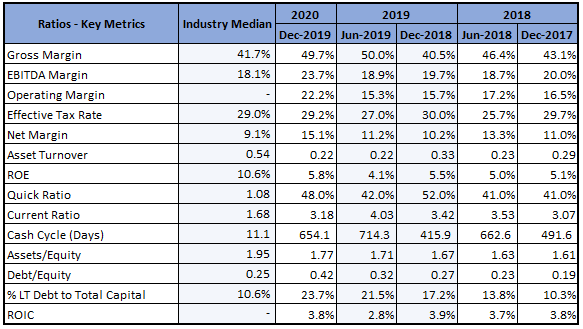

Key Margins:During 1HFY20, the company reported a gross margin of 49.7%, as compared to 40.5% in pcp. EBITDA margin stood at 23.7%, up from prior corresponding period margin of 19.7%. Net margin stood at 15.1%, as compared to 10.2% in 1HFY18. This indicates that the company has improved on its position to covert the top line into bottom line. Current ratio for the company stood at 3.18x, as compared to the industry median of 1.68x, depicting a better liquidity position in comparison to the industry.

Key Metrics (Source: Refinitiv, Thomson Reuters)

Growing Dividends: Over the four years period covering FY15-FY19, the company has delivered a CAGR of 6.5% in dividends, with FY15 and FY19 dividend amounting to 14 cents and 18 cents per share, respectively. In 1HFY20, the company declared an interim dividend of 9 cents per share, in line with pcp. Going forward, the company is focused on generating better returns by driving the consumption of farmed salmon and prawns in the restaurants and homes of Australia. A continued strategic focus coupled with a strong balance sheet position, is expected to deliver growth across earnings and returns in the years ahead..png)

Dividend Trend (Source: Company Reports)

Key Risk: The company has a focus on mitigating the operational risk of climate change in the marine and pond environment, which forms an essential element in salmon and prawn hatching and growing. Climate change, particularly summer water temperatures for salmon farming, play an important role in the company’s operations. To mitigate the above risk, the company has a selective branding program for salmon, along with an added focus on prawns. Other considerable options developed by the company for adapting to climate change, involve improved summer feed diets, modified farming strategies and technologies, species diversification with prawn operations and geographic diversification. In addition, the company also conducts broad scale environmental monitoring with the help of expert scientists.

Outlook: The company has witnessed positive consumer trends for its products and is currently aiming to underpin favorable domestic pricing and volume through agreements with domestic retailers. Despite the uncertainty regarding the long term impact of COVID-19 on its operations, the company believes that the overall market dynamics for salmon remain positive and is engaged in delivering on its strategy to increase overall operating EBITDA $/kg returns and provide better salmon returns for FY21 and beyond. Prawn biomass growth is also on track to deliver a harvest of ~2,500 tonnes for FY20, with the export market having greater potential than the domestic market. However, the company is still aiming for medium to long term growth in the domestic market, with export market offering risk mitigation from a sales perspective in the short term.

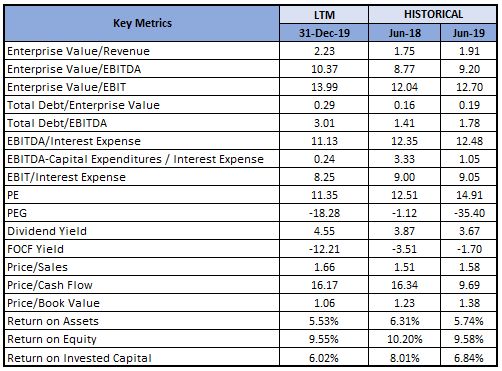

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

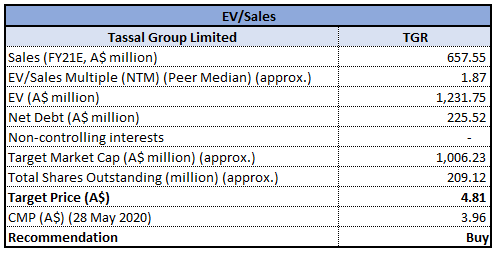

Valuation Methodology: EV/Sales Multiple Based Relative Valuation Approach (Illustrative)

EV/Sales Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock has corrected by 8.76% in the past six months and is currently trading close to the average of its 52-week trading range of $2.77 - $5.25, offering investors a decent opportunity to accumulate. The company’s performance in 1HFY20 was completely aligned with its strategy to support greater biomass and size for delivering increasing harvest and sales in 2HFY20 and FY21. Going forward, the company is eyeing further investment in salmon and prawn operations to promote long term growth. We have valued the stock using EV/Sales multiple based illustrative valuation method and have arrived at a target price with low double-digit upside (in % terms). For the purpose, we have taken peers like Freedom Foods Group Ltd (ASX: FNP), Select Harvests Ltd (ASX: SHV), Australian Agricultural Company Ltd (ASX: AAC), etc. Considering the performance in 1HFY20, optimistic trends in the salmon market, modest outlook for both salmon and prawns, focused growth strategy, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $3.96 as on 28th May 2020.

Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...