Company Overview - Sundance Energy Australia Limited is an onshore oil and natural gas company. The Company is focused on the exploration, development and production of oil and natural gas in the United States of America, and expansion of its portfolio of oil and gas leases in the United States of America. The Company's oil and natural gas properties are located in the United States oil and natural gas basins. The Company's operational activities are focused in south Texas targeting the Eagle Ford formation (Eagle Ford) and north central Oklahoma targeting the Mississippian and Woodford formations (Mississippian/Woodford). As of December 31, 2014, the Company had production of 2.4 million barrels of oil equivalent (MMBOE). The Company has an active two-rig drilling program targeting the Eagle Ford Formation in northeast McMullen County, Texas, onshore Texas Gulf-coast Basin. As of December 31, 2014, the Greater Anadarko Basin produced 532,916 barrel of oil equivalent (boe).

Analysis -

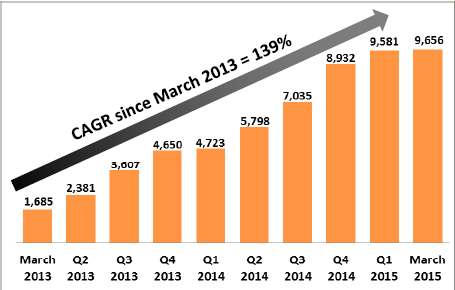

Sundance Energy Australia Ltd (ASX: SEA) continues to report strong results even for the first quarter of 2015, despite commodity price fluctuations. The firm’s overall oil, natural gas and natural gas liquids (“NGLs”) production (including flared gas), rose 7% to 862,281 BOE. Sundance average production per day surged 102% to 9,581 BOE as compared to 4,723 BOE per day during the first quarter of 2014. This increase is led by the production from new horizontal wells within the Eagle Ford.

Production growth since last eight quarters (Source: Company Reports)

Production growth since last eight quarters (Source: Company Reports)

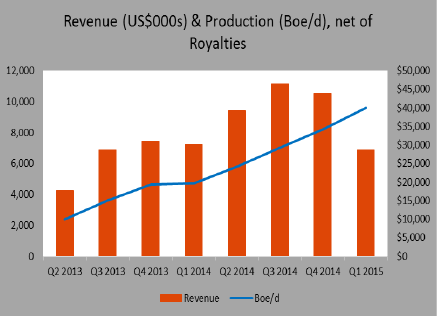

However, the company’s revenues witnessed pressure declining 4.9% on year over year terms to $28.7 million during the quarter. Although production growth of over 4,121 Boe/d added $31.6 million to the revenue, the decrease in the oil and natural gas prices offset this increase by over $33.1 million. Sundance could realize just $49.46 per bbl for oil during the quarter, which is 47.3% lower as compared to the price during the same period of 2014. The firm realized $2.97 per Mcf of natural gas (net of transportation and marketing fee) during the quarter, a decrease of 42.4% as compared to first quarter of 2014. Meanwhile, the firm’s facility for hydrogen sulfide (H2S) in Eagle Ford which is under development might improve the flared gas production from the second quarter of 2015. Sundance generated over 1,142 Boe/d of flared gas out of a 9,581 Boe/d during the first quarter of 2015.

First Quarter Performance (Source: Company Reports)

Cost Cutting Measures Drove Margins

First Quarter Performance (Source: Company Reports)

Cost Cutting Measures Drove Margins

In spite of pressure, Sundance strived to keep the falling oil and gas prices low on its overall performance by decreasing costs and maintaining its cost structure. As a result of its cost savings initiatives, the firm was able to decline its lease operating expenses (LOE) by 47.1% to $5.17 during the quarter from $9.78 in 2014. Sundance could achieve this by replacing its employees instead of contract operators and decreasing head count in the entire field. However, Production tax expense rose to 6.5% in the first quarter of 2015, as 86% of the firm’s first quarter production in 2015 was mainly in Texas, which demands 4.6% oil production tax rate and 1.9% ad valorem rate. Meanwhile Cash general and administrative costs (G&A) reduced 37% to $5.05 per Boe during the quarter, as compared to the first quarter in 2014.

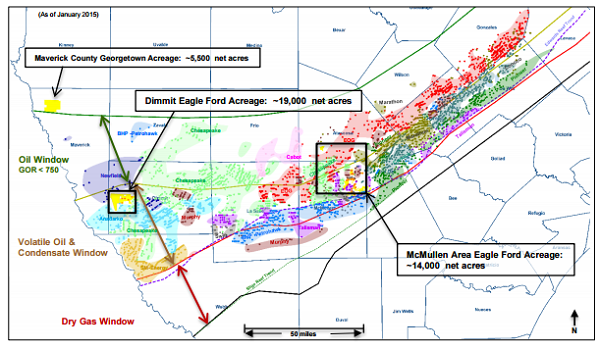

Eagle Ford Core Assets (Source - Company Reports)

Eagle Ford Core Assets (Source - Company Reports)

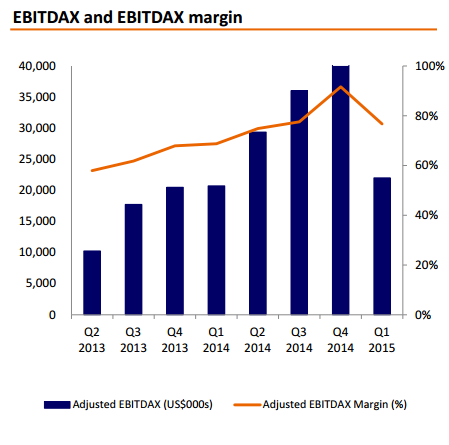

Subsequently, the firm was able to decrease its cash costs/BOE (including cash paid for LOE, production taxes, G&A) to $12.68/boe during the quarter, as compared to $15.13/boe during 2014. Over $1.49 per Boe reduction was contributed by LOE and production taxes, while $0.96 per boe was decreased in G&A. Consequently, the firm’s Adjusted EBITDAX increased to $22 million in first quarter 0f 2015 from $20 million during the same period in 2014, while the Adjusted EBITDAX margin improved to 76.7% from 68.7% in the first quarter of 2014.

EBITDAX Performance (Source: Company reports)

Raised Capital to maintain strong cash position

EBITDAX Performance (Source: Company reports)

Raised Capital to maintain strong cash position

With regards to the balance sheet, the firm’s cash and cash equivalents stood at $13.1 million as of 31

st March, 2015. Around $143.9 million were borrowings under the credit facility. During May, Sundance rose over $300 million Senior Secured Revolving Credit Facility (RBL) from Morgan Stanley bank and group, which helped the firm to retire its previous credit facilities. Sundance drew $150 million and paid off its earlier credit obligations. Over $25 million was drawn while closing among $75 million approved borrowing base. Out of $175 million senior term loan facility, $125 million was drawn during closing, while $50 million was committed with some obligations and not drawn. RBL has a term of five years while term load is for over five and a half years. Post this transaction, Sundance’s proforma liquidity rose to $63 million (which eliminates $50 million of undrawn contingent commitment) as of March 31

st, 2015. Having less than 1.1x debt to Adjusted EBITDAX as of March quarter, Sundance intends to maintain its balance sheet flexibility with low leverage profile.

Major Contribution from Eagle Ford Assets

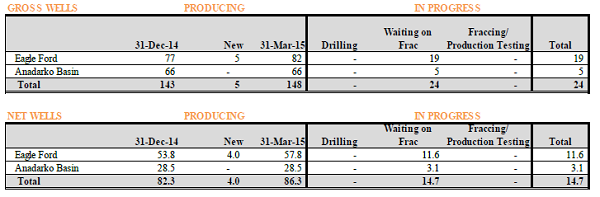

As per the exploration and development highlights during the quarter, the firm is on track adding 5 gross (4 net) producing wells from Eagle Ford wells as well as an extra 24 gross (14.7 net) wells during the first quarter of 2015. Moreover, Sundance witnessed a development and production additions of $31.4 million during the quarter, in line with its guidance of $32 million. The exploration and evaluation additions were $15 million (net of $46.4 million), slightly better than its earlier guidance of $14 million (a total of $466 million). Sundance expects its capital expenditure of $20 million -$25 million to be funded mainly from the operating cash flows during the period during the second quarter of 2015. In addition, Sundance expects to finish its 8 gross (8 net) of these wells by 2015, and might complete the remaining wells during 2016.

Exploration and development highlights (Source: Company reports)

Exploration and development highlights (Source: Company reports)

Meanwhile, Sundance expects its 11 gross (3.6 net) non operated wells to be delayed to 2016. The average costs per well decreased over 30% to $6.1 million, against $8.5 million of average costs per well in 2014. Sundance production during the quarter increased mainly due to Eagle Ford production of 8,269 Boe/d (86%) of total production, against 2,612 Boe/d (55%) in 2014. Moreover, Sundance achieved 99.6% of its Eagle Ford Production, during March quarter. As per the Greater Anadarko Basin, the firm has delayed 3 gross (2.6 net) operated wells to 2016. Meanwhile Anadarko’s contribution to the overall production decreased to 1,312 Boe/d (14%) during the first quarter of 2015, against 1,412 Boe/d (30%) in first quarter of 2014. Sundance achieved 60.6% production from Anadarko during the quarter. Meanwhile, Sundance completed all rigs by first quarter of 2015, and has no intention for further service commitments for the rest of the fiscal year.

Hedging Activities

Sundance entered into oil as well as gas derivative contracts to hedge against commodity prices fluctuations, Sundance entered into 140,000, 100,000 and 96,000 bbls oil derivative contracts during April 2015 with a floor price of $50 and weighted average ceiling at $73.9. After this move, Sundance has now hedged over 28% of its total oil production for 2015.

Conclusion

Sundance has very limited drilling obligations for the rest of the year. The firm need to develop only 1 net drilling program. This drilling can be entirely funded from operating cash flows. With no current service commitments, we believe that the company will be able to decrease its costs and is on track to achieve its cash operating costs target to $12.68 per boe.Sundance has alsoimproved its full year production guidance to the range of 7,850 and 8,500 barrels of oil or equivalent, which is a rise of 13%-17% as compared to 2014. The growth in production is expected to be mainly contributed by Eagle Ford.

Sundance Energy Daily Chart (Source - Company Reports)

Sundance Energy Daily Chart (Source - Company Reports)

The shares of Sundance has gained around 18.67% over the last three months, as compared to a negative returns of 6.3% of S&P/ASX 200. Although the stock has corrected over 6.9% over the last four weeks, we believe this correction to be a buying opportunity given the enormous potential the stock has in this space. The firm’s cost cutting initiatives, efforts to improve margins despite oil price fluctuations, huge hedging activities and major production boost coming from its top quality Eagle Ford asset is expected to drive the stock’s performance going forward. Based on the foregoing we give a “BUY” recommendation to Sundance at the current price of $0.515.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...