Company Overview - Suncorp Group Limited is engaged in the provision of general insurance, banking, life insurance, superannuation products and related services to the retail, corporate and commercial sectors in Australia and New Zealand. The Company's segments include Personal Insurance, which provides home and contents, motor, boat and travel insurance products; Commercial Insurance, which provides commercial motor, commercial property, marine, industrial special risks, loan protection insurance products and others; General Insurance New Zealand, which provides motor, marine, business, rural, travel insurance products and others; Bank, which provides personal and commercial banking, property and equipment finance, home, personal and small business loans and others; Life, which provides superannuation administration services, financial planning and funds administration services, and Corporate, which includes investment of the Company's capital, business strategy activities and its shared services.

.png)

SUN Details

Softness in bottom line due to raise in claims:Suncorp Group Ltd (ASX: SUN) has reported a weak NPAT of $1,038 million in FY 16 as compared to $1,133 million of the same period of last year. This is due to the lower returns from investment markets and a reduction in reserve releases. The underlying profit included the positive lapse and claims experience of $21 million. Additionally, the General Insurance underlying ITR is of 10.6% due to the increased cost of settling claims and lower investment returns while the total GWP increased by 1.8% to over $9 billion. On the other hand, the group’s Bank segment reported a net profit after tax growth of 11.0% due to continued home lending growth, improved net interest margins and ongoing improvement in credit quality. Suncorp Life segment net profit after tax grew 13.6% and the underlying profit increased by 9.7% to $124 million. SUN has included in these numbers, a significant contribution of $182 million from New Zealand. Moreover, in FY 16 on an-after tax basis, the impact of natural hazards was $237 million which is lower than FY 15.

The investment earnings in General Insurance and Life was $138 million lower while the Reserve releases were still well in excess of the long term average, wherein the after tax benefit was $56 million lower in FY 16. SUN has created a $55 million provision for restructure or $39 million after tax which would generate at least $80 million of recurring benefits in the coming year. The Home, Motor and Commercial were $156 million after tax is higher.

.png)

FY 16 Financial Performances (Source: Company Reports)

New Operating Model: SUN has completed the organizational restructure in July 2016, and accordingly delivered over $80 million in annualized savings at a one-off pre-tax charge of $55 million. The new model is the ‘One Suncorp’ operating model which is aimed to drive the customer strategy. SUN’s Marketplace approach would connect more customers to SUN by providing access to all products, all services and all brands through any channel.

This would enable them to select their own solutions based on prior product purchases. SUN has elevated the customer focus, as well as aligned the cost base to deliver a more resilient business. The stability and momentum of SUN is of high priority for the company.

.png)

Organizational Restructure (Source: Company Reports)

Marketplace strategy: The group’s Marketplace strategy breaks the customer’s needs into four groups. These are self which is health and wellbeing, Mobility which means buying and protecting your car, Property that is buying and protecting property assets and the Money that is liquidity, longevity and transactions.

Moreover, SUN offers access to the customers through stores, contact centers, digital and through the brokers and advisers. Additionally, the key enablers for the Marketplace are the leading technology, their people and the way SUN works, data and analytics expertise and SUN’s trusted brands. In addition, SUN’s solutions are insurance, banking and wealth, third party products and services and the new alternatives.

.png)

SUN’s Marketplace Strategy (Source: Company Reports)

New Offerings:SUN has made good progress in introducing new solutions and propositions into the target markets. SUN has launched Trov in April, launched the Shannons Club app in June, and would shortly be launching the new health offer.

Moreover, SUN has launched the 9Spokes solution for small business, which is a third party annuity offering for mature customers, and launched AAMI Smartplates for Learner drivers. One third of customers are connected, the retention rate of Connected Customers is 96% versus 75% for non?connected and the company’s goal is to increase the number of Connected Customers.

.png)

Customer Strategy (Source: Company Reports)

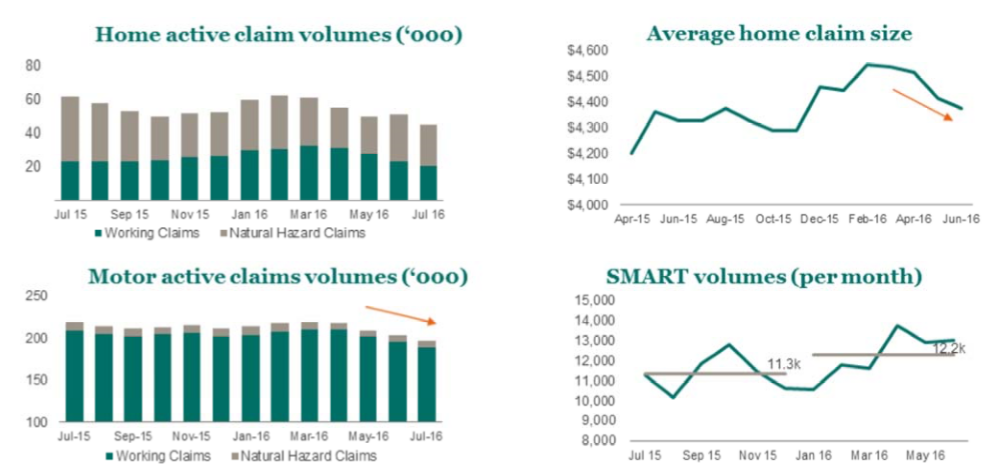

Restoring UITR:SUN is working hard to achieve improvements in working claims as the group has moved towards restoring underlying insurance trading ratio (UITR) to 12%. The home claims volumes and average claim costs have reduced since December 2015. In motor, the active claims volumes have also reduced, with an increase in the number of vehicles repaired in the SMART shops each month.

SUN has now 36 SMART facilities and a further five are planned to open in FY17. Additionally, SUN is reducing the working claims cost to improve the customer experience and the company is expecting further improvements in margins in the coming year.

Improving Working Claims to Restore UITR (Source: Company Reports)

Enhanced reinsurance program for FY 17:To reduce the potential volatility related to future natural hazards, Suncorp has purchased additional reinsurance protection for the 2017 financial year. The Natural Hazards Aggregate cover would offer Suncorp with $300 million of protection after the retained portion of natural hazard events which is greater than $5 million, reaching a total retained cost of $460 million. The upper limit on Suncorp’s main catastrophe program, which covers the Group’s Home, Motor and Commercial Property portfolios for major events, would remain unchanged at $6.9 billion. The maximum event retention is $250 million. Additional cover has also been purchased to reduce the maximum event retention for a second Australian event to $200 million while the group has $50 million for a third and fourth event. For New Zealand risks, multi-year cover is in place which reduces the first event retention to NZ$50 million while the second and third event retentions have NZ$25 million.

The enhancements to the reinsurance program have led to a net reduction in the natural hazard allowance for the 2017 financial year to $620 million. With this move, SUN is building a more resilient business through managing the impact of natural hazards via additional cover for the coming year.

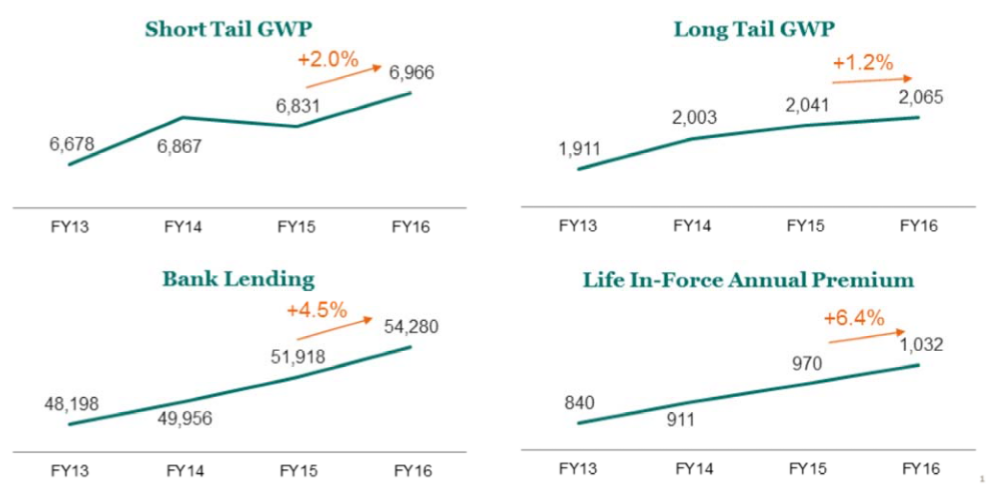

Growth across all Business Lines: In FY 16, SUN has delivered a growth of 2.9% across the group despite a period of significant change.

There is a positive top line momentum, particularly in motor at 2.9% and home at 1.8%. Bank lending has grown 4.5% while maintaining the credit quality and margin. Life in?force business has increased by 6.4%. The positive growth would position SUN for a strong year ahead.

Growth across all business lines ($m) (Source: Company Reports)

Strengthening Balance sheet:At 30 June 2016, the General Insurance CET1 was reported to be 1.21 times the PCA, slightly above its target of 0.95 to 1.15. Similarly, the Bank CET1 of 9.21% is above its target level of 8.5% to 9%.

The group has $146 million of franking credits available after the payment of the dividend. Despite making the dividend payment, SUN is well capitalized with about $346 million in CET1 capital, which is above its operating targets.

Favorable medium term targets: Suncorp’s key targets in the medium term are broadening of customer relationships, maintaining a flat cost base in FY17 and FY18. Moreover, the group is aiming on improving underlying NPAT, delivering a sustainable ROE of at least 10%, which implies an underlying ITR of at least 12%. The group intends to maintain its dividend payout ratio in the range of 60% to 80% of cash earnings. Meanwhile, SUN has given a dividend of 68 cents per share fully franked in FY 16, which reflects a payout ratio of 80% of cash earnings.

Stock Performance:The shares of SUN stock rose over 5.22% in the last three months (as of September 16, 2016) and we believe there is potential for positive momentum going forward. SUN’s new operating model would enable them to improve their solid earnings growth over the next few years. Additionally, SUN is well positioned to withstand the rising claims concerns. SUN has proven its ability to deal with the change and volatility in the Australian and global economies. Based on the foregoing, we give a “Buy” recommendation on the stock at the current price of $12.39

SUN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...