Company Overview - STW Communications Group Ltd. is engaged in advertising and diversified communications operations. The Company provides advertising and communications services for clients through various channels, including television, radio, print, outdoor and electronic forms. It offers advertising, media, insights and research, branding, brand activation, digital, and field and shopper marketing. The Company operates in two segments: Advertising, Production and Media; and Diversified Communications. The Advertising, Production and Media segment provides advertising services, television and print production services and media investments for Australia, New Zealand and other international brands. The Diversified Communications segment covers the full gamut of marketing communications services. The Diversified Communications segment offers clients a solution to their marketing needs, well beyond their traditional advertising, production and media requirements.

Analysis - With this report, we bring your attention to STW Communications Group (SGN) which reported its revenues of about $190.3 million for the period ended 30 June 2014. The revenues rose by 9% compared to the prior year. The profit for said period was $19.0 million, which was up 1.2%. Diluted earnings per share of 4.72 cents were reported which indicated a rise of 0.9% in comparison to the prior year.

Group Profit And Loss $M (Source – Company Reports)

Group Profit And Loss $M (Source – Company Reports)

The Company’s cash and gross debt balances were $27.2 million ($43.3 million as at 31 December 2013) and $183.2 million ($172.4 million as at 31 December 2013), respectively. As at 30 June 2014, the Company has access to debt facilities totaling $235 million, of which $177.4 million is drawn. With the end of the half-year, SGN has entered into new debt facilities totaling $35 million and has also received a credit approved term sheet for the extension of $100 million of debt facilities to August 2017. SGN’s cash flows were clearly a result of timing of media payments and the improvement in working capital balances at 30 June 2014.

Highlights (Source – Company Reports)

Highlights (Source – Company Reports)

As per the 2014 half year results, full year organic EPS and NPAT guidance remained unchanged. There were ups and down with the Australian economy remaining weak, soft media market, and client spend under pressure. Nonetheless, New Zealand’s performance, market share gains in digital, healthy performance in design and PR, momentum in geographic expansion, growing influence in the shopper marketing and data space, and business model supporting performance in strained market, were of importance.

Interim Dividend (Source – Company Reports)

Interim Dividend (Source – Company Reports)

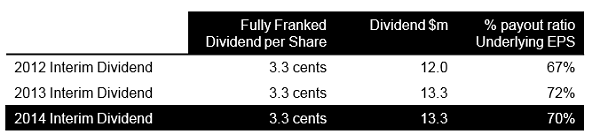

Since the end of the half-year at 30 June 2014, the Company announced the payment of a fully franked ordinary dividend of $13.3 million (3.3 cents per fully paid ordinary share) while indicating a payout ratio of 70%. SGN also announced for introduction of a dividend reinvestment plan for shareholders to reinvest their dividends in the Company’s shares. A 2.5% discount is applicable to shares issued under the plan. The Company also entered into a sale and lease back arrangement of plant and equipment. The profits from sale were $5.9m which will be repaid over a period of 5 years.

6 Months to June ‘14 Growth on Prior Year (Source – Company Reports)

6 Months to June ‘14 Growth on Prior Year (Source – Company Reports)

The Company has identified two reportable segments, namely, Advertising, Production and Media; and – Diversified Communications. The Advertising, Production & Media witnessed a weaker than expected operating result. Diversified Communications also witnessed softer operating results than otherwise anticipated. Nonetheless, other key highlights reported by the Company appear to balance the situation towards a positive direction.

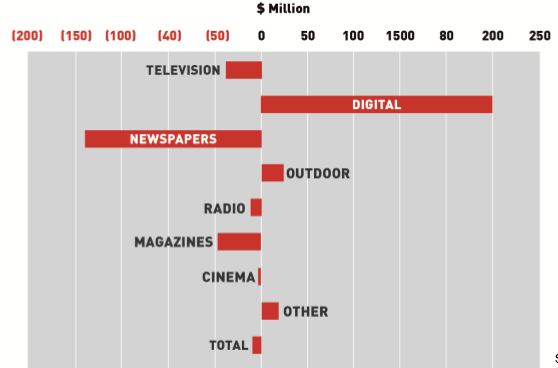

Forecast 12 Months to Dec Growth on Prior Year (Source – Company Reports)

Forecast 12 Months to Dec Growth on Prior Year (Source – Company Reports)

As part of other key highlights for the first half 2014, the Company intends to have a comprehensive data action plan entailing about 51 operating company data action plans. The STW Datahub is also established accompanied by formation of data pods. The Company believes that the opportunity lies in the interpretation and application of data to create, deliver and optimize targeted and personalized communications for the clients instead of data

per se.

SGN’s shopper marketing includes a number of specialist shopper companies that are able to offer a classic range of complementary services to enable clients plan, create and deliver innovative shopper programs. Although the Company reported a challenging marketing environment, SGN’s market position is still supporting continued growth. The Company’s strategy and model remain on track. The Company is also emphasizing on sprouting its business model in view of fluidic conditions. SGN reports that opportunities at New Zealand and other offshore regions look appealing. In terms of training and development, SGN’s campus strategy investment is enduring. SGN’s 2014 organic guidance also remains the same as earlier. The Company expected mid-single digit growth in EPS and NPAT in view of the benefits from ADG acquisition.

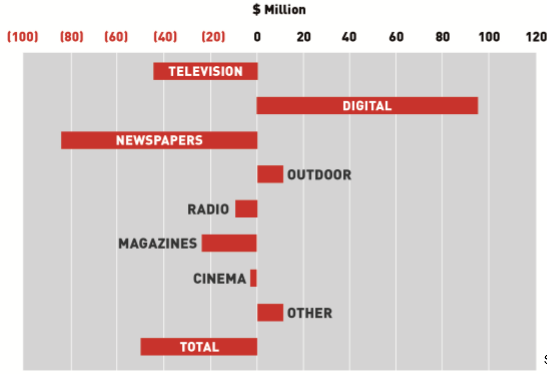

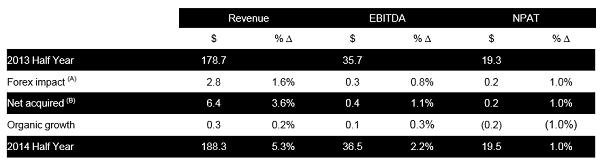

Half Year 2014 – Components of Growth $M (Source – Company Reports)

Half Year 2014 – Components of Growth $M (Source – Company Reports)

The offshore expansion is also progressing well. The Company is operating its businesses beyond Australia and New Zealand. SGN is also investing in new partnerships.

Business Expansion (Source – Company Reports)

Business Expansion (Source – Company Reports)

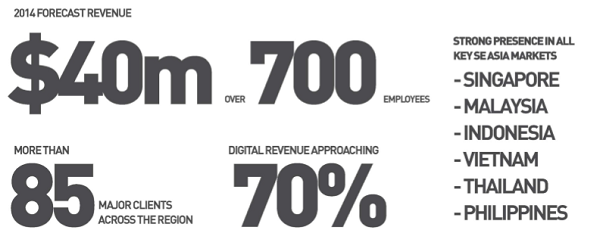

As per the first half 2014 Asia business updates, the Company witnessed a top notch performance and full-year outlook from Aleph. The Edge Asia model is servicing key clients in multiple markets and is winning market share regionally. Alpha Salmon Indonesia alignment into Edge Asia is forecasting 80% revenue growth in CY14 and is no. 2 digital business in Indonesia. Buchanan Group’s Home Tester Club JV launch in Indonesia is moving ahead. The Company aims to consolidate and expand regional landscape of Edge, Aleph and CPR Vision. Further, SGN’s DT and Designworks are servicing client demand in Asia while leveraging regional network and footprint.

The Company, however, needs to be cautious of the risks related to key offshore economic conditions, weakening in industry advertising expenditure, and employee base along with any acquisition pricing and integration related risk.

SGN Company Chart (Source - Thomson Reuters)

SGN Company Chart (Source - Thomson Reuters)

The Company stated that CY14 has been a little harsh with regards to various conditions, the company has still been able to put efforts to manage gains irrespective of declining consumer confidence and soft advertising spending.

Nonetheless, the second-half FY14 profits have indicated about two-thirds of annual profits. The Company’s client pitch pipeline also looks strong. Nonetheless, SGN may need to win new accounts in order to achieve its guidance. The digital, design, and public relations operations have been performing well along with strong performance from the Company’s Asian business. The company thus expects a much stronger second half in view of maintenance of its guidance. The second half is expected to be furthered by the ADG acquisition. SGN aims to maintain dominance in Australia and New Zealand with plans to invest in digital communications and increase footprint into south-east Asia. In view of the fact that the digital companies back a larger proportion of revenue, hence there is a possibility that the margins increase further. Other key attributes such as the Company’s one-stop shop offer, growth prospects and expansion beyond Australia and New Zealand, and robust full franked dividend yield add to its momentum.

The overall scenario thus looks interesting. Accordingly, we put a

BUY recommendation for this stock at the current price of $1.165.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...