Company Overview - STW Communications Group is Australia’s largest local marketing communications group. SGN also has operations based in New Zealand and a small but emerging footprint in Southeast Asia. SGN’s service offerings span across a broad range of communication disciplines, including advertising, production and media, digital, brand design, public relations, research and insight as well as a range of niche specialities. These disciplines fall under the umbrella of two divisions: Advertising, Production and Media; and Diversified.

Analysis – The first four months of 2014 have started more slowly than SGN would have liked. Management now expect mid-single digit NPAT growth in FY14 to be the upper end of what they can achieve. We note that SGN’s earnings are weighted to 2H. Management are looking at revenue and cost levers to support growth. We believe this is a contributor to the SGN’s more subdued outlook, with ad market momentum slowing YTD vs the run rate in 2HCY13. 9-10 months ago SGN had won a significant amount of new business. While SGN have won some smaller accounts there have been missed opportunities and notably its IKON agency has lost some accounts.

STW Awards Dashboard (Source - Company Reports)

STW Awards Dashboard (Source - Company Reports)

Global ad agency peers generally had a stronger 1Q14. In the Q1 results for Havas, Publicis and IPG, Australia was identified as having reasonable growth, with Publicis notably achieving more than 5% organic revenue growth. Australia was not specifically mentioned by WPP or Omnicom. We believe SGN’s revenue growth was in line to modestly below its global peers over the quarter and expect it to have been below the 5% mark achieved by Publicis.

STW New Clients (Source - Company Reports)

STW New Clients (Source - Company Reports)

At the full year result in February management provided the following earnings guidance and outlook statement. Guidance of FY14 Net Profit after Tax growth of 5%, with Colmar Brunton only expected to make a small contribution. Momentum is building in the business with the management encouraged by the new business pipeline. The NZ and offshore markets are delivering good growth and momentum is solid into 2014. SGN provided the following update at its AGM on 16

th May. The first four months of 2014 have started more slowly than the management would have liked. The first quarter reforecast by SGN and its companies still supports EPS growth in FY14, however mid-single digit is now the upper end of likely outcomes. Management is continuing to focus on the cost base.

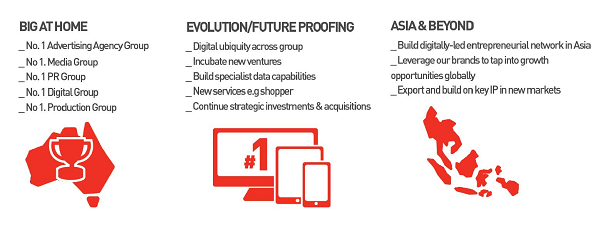

STW Strategy (Source - Company Reports)

STW Strategy (Source - Company Reports)

Over January and February, the Australian ad market was only down modestly CYTD according to Standard Media Index (SMI) ad agency data (Source – www.adnews.com.au). This trend continued in March, with SMI data indicating the total market fell 2.5% year on year. Radio, Outdoor and Pay TV were weak in March, however metro TV was up 3.2% (Source: ww.adnews.com.au). April was notably weak for the Australian ad market, with SMI data indicating it fell 9.2% year on year. This was in part attributable to the combined Easter/ANZAC holidays as well as general hesitancy ahead of the Federal budget. While SGN’s revenue are not directly correlated to the ad market, it is still an important barometer for its clients and management will typically need to take a view on the ad market when setting earnings guidance.

Dividend + NPAT Growth (Source - Company Reports)

Dividend + NPAT Growth (Source - Company Reports)

The other important component of SGN’s revenue outlook is new business wins particularly from its larger agencies. After a strong run of large new business wins in mid-2013 the momentum has slowed. The following is a selection of SGN’s business wins/losses 2014 YTD, sourced from press reports. This is purely illustrative and by no means a comprehensive list:

Wins – La Trobe University, The Smith Family, Officeworks and Transport Accident Commission.

Losses – Vodafone, Coca Cola, SPC Ardmona and Tetley

Potential Missed Opportunities – RACV, Pacific Brands and BUPA

Of the account losses, Coca Cola is clearly the trophy account but we suspect it was relatively low margin, as can often be the case with large media buying accounts. SPC was estimated to have $8m in billings so we wouldn’t expect it to have significant earnings impact. Ikon one of the ad agencies owned by SGN has had a significant churn in senior/executive staff for the past 12 months including a new CEO and we believe this is partly reflected in it losing some of its accounts and not sustaining its momentum in winning new clients. The new CEO James Greet comes with a solid reputation in the industry and we would expect this business to be back on track in the coming months. Ikon is 100% owned and SGN’s largest media buying agency. We note that Ikon recently also closed its Perth office.

STW Daily Chart (Source - Thomson Reuters)

STW Daily Chart (Source - Thomson Reuters)

Despite difficult markets we expect SGN will continue to grow organically and acquisitively. We believe SGN’s expanded platform and market share gains will provide leverage as the cycle strengthens. SGN’s Australian digital capability is broad and deep. SGN is well placed to benefit from the structural migration of advertising spend to digital. Southeast Asian expansion strategy offers growth potential to SGN. Rising wealth levels in this large region combined with rising online access and usage is expected to fuel growth in advertising and branding investment by corporations over the medium term. The balance sheet remains reasonable healthy and we note the potential for accretive acquisitions.

SGN is well positioned in a difficult and unrelenting industry that is characterised by continual and accelerating change. We believe that benefits of STW’s diversified model will continue to deliver results. SGN has a three pillared strategic growth focus: to drive growth out of their leadership positions in Australia and New Zealand; to continue to grow and evolve their digital offering; and to selectively and carefully expand their footprint into new markets beyond Australia and New Zealand. We see SGN as a lower risk way to obtain media sector exposure. In the current market we believe SGN’s ability to rapidly adjust its cost base in light of a bumpy ad market recovery is a key positive. We like the SGN story and reiterate a BUY on the stock at the current price of $1.39.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...