Company Overview – STW Communications Group is Australia’s largest local marketing communications group. SGN also has operations based in New Zealand and a small but emerging footprint in Southeast Asia. SGN’s service offerings span across a broad range of communication disciplines, including advertising, production and media, digital, brand design, public relations, research and insight as well as a range of niche specialities. These disciplines fall under the umbrella of two divisions: Advertising, Production and Media; and Diversified.

Analysis – SGN announced an underlying Net Profit after tax (NPAT) of 3.2% at $49.5m. The result was up 12.5% on the previous corresponding period which was marginally short of company guidance of 15% growth. Earnings per Share (EPS) grew 2.5% below SGN’s mid-single digit guidance. We believe the limited pick up in work opportunities post-election was the main reason for the short fall. Delays in sealing an acquisition earlier in the year also did not help. Media and larger agencies were the key drivers of organic growth. SGN noted positive momentum in its Australian business heading into CY14. With cash flow timing issues largely washed through in January, SGN’s balance sheet is also in better shape. While the macro backdrop currently remains difficult we believe this will improve as CY14 progresses on the back of improved business confidence.

Source – Company Reports

Further disclosure around the composition of SGN’s growth show that 75% of the organic Earnings before interest tax, depreciation and amortization (EBITDA) uplift in FY13 was acquisition driven largely from four main businesses purchased in late FY12. While organic growth was muted we not this was another year of challenging conditions with the anticipated post-election uplift in business activity yet to materialise. Operating cash flow of A$35.4m represented a very strong 2H rebound. With stronger than expected capital expenditure net debt finished the year at A$129m. SGN has provided initial FY14 guidance looking for NPAT growth in the mid-single digits. While January is a traditionally weak month, recent commentary has suggested that the company has made a solid start to the year. The one disappointment with their recent result was cash generation which is inconsistent with a solid track record built in the previous years. While the company finalised another purchase in the second half (Colmar Brunton), we are cognisant of the necessity around reinvesting in the business to ensure SGN’s offering adapts to a rapidly changing environment with regards to the marketing spend. SGN is focussing on big data opportunities with better integrating its capabilities across operating companies. We see this as an exciting organic growth avenue for SGN.

Source – Company Reports

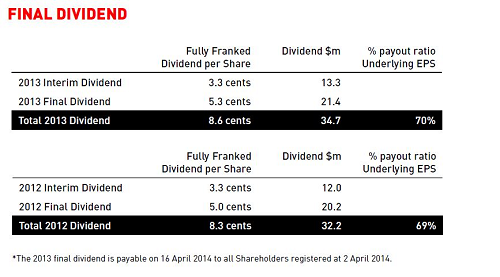

SGN has a strong momentum heading into 2014. NZ and the offshore markets are delivering solid growth. Management described the new business pipeline as encouraging. Management expect FY14 NPAT to grow mid-single digits. This is prior to any new acquisitions. It will include a small contribution from Colmar Brunton but the majority of the expected earnings growth is organic. Due to unfavourable cash flow timing issues with media related work at year end, SGN’s net debt position did not improve as anticipated vs mid year levels. SGN’s net debt position stood at $165.6m largely unchanged versus 30 Jun 2013 $164.5m and an increase on 31 Dec 2012 ($138.5m). We understand January saw strong cash inflow which has since reduced net debt and improved balance sheet metrics.

SGN Daily Chart (Source – Thomson Reuters)

|

Dividend |

|

Yield |

5.752508 |

FY |

|

|

6.641294 |

5yr Av |

|

Payout Ratio |

69.72081 |

FY |

|

|

67.64375 |

5yr Av |

Recent acquisitions are expected to drive reasonable growth over the next five years. The company has $45.8m to pay in earn outs over the next five years with peak settlements spread over the FY14 and Fy15 years. $22m in earn outs relates to put and call options and are tied to achievement of incremental earnings. Organically we see the potential for STW Communications to continue to win contracts as well as expanding revenue from existing clients. Traditional ad budgets that sit with the Chief Marketing officers whilst likely to remain the primary revenue source for advertising companies are no longer the only revenue source. We estimate ad budgets will contribute 70% income to STW Communications in five years. Chief Information Officers and Chief Technology Officers will become increasingly important for advertisers and may increase the overall size of the advertising pie especially as retailers increase spend on websites, data and loyalty programs and incorporate this cost into their cost of goods sold rather than cost of doing business. Owned and earned media where advertisers assist retailers or other clients to build content rather than the traditional paid model is likely to provide new revenue opportunities for media companies and we see STW Communications as being well positioned to benefit from this.

Source – Company Reports

The key downside risks to SGN include: - 1 – SGN is exposed to cyclical risks. A material deterioration in industry advertising expenditure would place pressures on revenues and margins. This in turn will have downside risks to dividends. 2- Further deterioration in key offshore economic conditions can have direct repercussions on advertising expenditure and brand investment by SGN’s international customers.

Revenue from operations increased 13.6% or $48m to $399m. The majority of this growth rate came from acquisitions in Australia and Asia which we estimate contributed $27m and $6m additional revenue. Although SGN is not the most leveraged business to an economic upturn we believe its earnings are relatively stable and its dividends are predictable. The combination of SGN’s leadership in digital, growth prospects in South East Asia, proven through the cycle growth capability plus a healthy fully franked dividend yield is attractive. We believe SGN’s expanded platform and market share gains over the past 2-3 years place SGN on solid footing as the cycle strengthens. SGN’s Australian digital capability is broad and deep. SGN is well placed to benefit from the structural migration of advertising spend to digital. Southeast Asian expansion strategy offers growth potential. Rising wealth levels in this large region combined with rising online access and usage is expected to fuel growth in advertising and branding investment by corporations over the medium term. We will be putting a BUY recommendation at the current price of $1.51.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...