Kalkine has a fully transformed New Avatar.

Company Overview: SRG Global Limited, formerly Global Construction Services Limited, is primarily involved in engineering, mining, maintenance and construction contracting. The Company operates through three segments: Construction, Asset Services and Mining. Its Construction segment consists of supplying products and services to customers involved in the construction of infrastructure, including bridges, dams, office towers, shopping centers, hotels, car parks, recreational buildings and hospitals. Its Asset Services segment consists of supplying services to customers across the asset life cycle. It provides services across multiple sectors, including oil and gas, energy, infrastructure, offshore, mining, power generation, water treatment plants, commissioning, decommissioning, shutdowns and civil works. The Mining segment services mining clients and provides ground solutions, including production drilling, ground and slope stabilization, design engineering and monitoring services..png)

SRG Details

New Contract Wins to Drive Top-line Growth: SRG Global Limited (ASX: SRG) delivers a suite of engineering-led specialist construction, maintenance, and mining services throughout the entire asset lifecycle. The company is generally into bridge construction, dam strengthening, refractory services, etc. The market capitalisation of the company stood at ~A$167.17 Mn as on 6th December 2019. Over the 5-year period covering FY15 to FY19, the company’s revenue witnessed a CAGR growth of 34.08%, with FY15 and FY19 revenue amounting to $486.4 million and $150.5 million, respectively. Over the period, revenue has seen a continuous upward movement. Bottom-line of the company grew at a CAGR of 2.0% over the last five years, with FY15 and FY19 profit after tax amounting to $8.7 million and $9.4 million, respectively. Gross profit over the 5-year period witnessed a CAGR growth of 20.48%, with FY15 and FY19 gross profit amounting to $114.3 million and $240.8 million, respectively. This reflects that the company is possessing decent capabilities to garner revenues and is managing its direct costs in an effective way. SRG’s total assets stood at A$430.6 million in FY19 and witnessed a CAGR growth of 28.81% during the span of FY16 to FY19.

During FY19, the company’s total receivables stood at A$118 million, reflecting a rise from A$51.2 million in FY18. It looks like that the cash levels of the company might rise in the upcoming period and it could help SRG in gaining decent levels of growth as it could make deployments towards growth objectives. Resultantly, it might provide the company with a strength to gain strong traction among the industry. As per the key personnel of the company, the financial year 2019 has been a year of significant transformation for the business. The company has made significant progress to establish itself as the most sought-after engineering-led construction, maintenance and mining services business despite experiencing some significant challenges in the last 12 months. The company recently announced that Mitsubishi UFJ Financial Group, Inc. has made a change to their substantial holdings in the company on 29th November 2019 and the current voting power stands at 9.72% as compared to the previous voting power of 8.71%.

The company has the expertise to self-perform and provide a complete end-to-end solution which is very important to its clients which happens to be key differentiators in the industry. During FY19, the company reported underlying EBITDA amounting to $32.0 million even though there were challenging business environment and market conditions. The company has a record work in hand which amounted to $708 million that increased 36% in last six months with the number of significant contract wins as well as further $5.2 billion pipeline of opportunities in the positive growth sectors. Around 70% of its work in hand is generated from recurring revenue streams which lays the foundation for its long-term sustainable success.

There are expectations that recurring revenues, decent liquidity standing, lower Debt/Equity ratio as compared to broader industry, decent cash position and focus towards revenue diversity are expected to act as tailwinds for long-term growth.

.png)

Record Work in Hand (Source: Company Reports)

Overview of Margins: The company’s gross margin stood at 49.5% in FY19, which is higher than the industry median of 12.9% while SRG’s EBITDA margin stood at 3.5%. The company’s current ratio stood at 1.35x in FY19, which is higher than industry median of 1.14x and, therefore, it can be said that SRG has better capabilities to meet its short-term obligations. Also, decent liquidity footing provides the company with the sufficient headroom for further deployments towards growth objectives.

The company’s Debt/Equity ratio stood at 0.18x in FY19, which is lower than the industry median of 0.46x and, therefore, it can be said that SRG is possessing less leveraged balance sheet as compared to broader industry. Generally, lower debt on the balance sheet reflects stability and the company might focus towards its growth prospects. .png)

Key Metrics (Source: Thomson Reuters)

Strong Cash Position Might Support Growth Prospects: During FY19, the company reported revenue amounting to $506.4 million from $431.6 million in FY18. The increase in revenue has been driven via the acquisition of TBS in New Zealand in March 2018 and acquisition of the remaining 49% of Gallery Facades in June 2018. The company’s EBITDA and EBIT margins have been primarily impacted by (1) challenging market conditions, (2) delayed awards of targeted large-scale construction projects, and (3) associated carrying costs of maintaining capability.

The company possesses a strong cash position from which the business can target future project and growth opportunities. SRG has significant tax assets, which are related to divested business, within Australia, which would result in minimal cash payments related to income tax expense for future financial years. The company has strong net cash position of $12.2 million, which is because of disciplined capital management practices. This focus continues into FY20 with additional capacity in borrowings amounting to around $54.2 million. SRG Global Limited has additional issuing capacity of $120.7 million in surety bond facilities..png)

Financial Position (Source: Company Reports)

A Quick Look at Construction Segment: The construction segment of the company provides a revenue and EBITDA contribution of 57% and 30%, respectively. This segment has two key focus areas of civil and building. In the civil sector, the company’s focus is on the specialist markets of dams, bridges, LNG tanks, and windfarms. In the building sector, SRG focuses on securing a vertically integrated structure and facade projects of scale with repeat, tier-one clients. During FY19, the construction segment delivered revenue amounting to $268.0 million as compared to $120.0 million of FY18 and EBITDA stood at $8.9 million against $5.2 million of FY18. In the construction segment, a new business unit was also established to aim the emerging flammable cladding market. While the market is in its infancy, the company’s expertise in the complete supply chain for engineered facades places the business in a strong position to secure works in this market.

Asset Services Segment: In FY19, the Asset Services Segment has maintained a disciplined focus on securing recurring and term revenue contracts with tier-one clients. The company made it possible through the enhanced and combined offering of SRG Global such that the business can leverage existing site presence with a ‘One Stop Shop’ model. When it comes to contribution to the group, this segment delivered revenue amounting to $135.8 million, and EBITDA stood at $15.5 million in FY19.

Mining Segment: The Mining Services segment of the company has delivered a solid financial performance with the help of a strong asset utilisation throughout its production drill fleet. The segment’s primary focus is on partnering with targeted clients in specific commodities and driving operational efficiencies and innovation in asset utilisation. In FY19, two long-term strategic partnerships with tier-one customers were renewed. SRG Global’s operations with Evolution Mining were extended for the span of 5 years via Umbrella Agreement valued at $115.0 million. Additionally, SRG Global’s over 20-year relationship with ‘superpit’ in Kalgoorlie was extended when Kalgoorlie Consolidated Gold Mines extended the specialist geotech contract for the span of further 5 years.

Decent Dividend Paid during the Year: During the financial year 2019, the company declared total fully franked dividends amounting to 1.5 cents per share totalling to $6.609 million. This includes a fully franked final dividend of 0.5 cent per share, which was paid on 23rd October 2019 and fully franked interim dividend of 1.0 cent per share totalling to $4.407 million.

What to Expect: The company would continue to remain disciplined in its working winning, operational execution and delivery against long-term strategic objectives. SRG is well-placed for sustainable growth in FY20 and beyond supported by record work in hand as well as a significant and growing recurring revenue base. The company is planning to maintain a conservative net cash balance sheet and to leverage site presence to deliver an expanded offering to the client base.

The company is encouraged by the level of activity and potential investment in sectors where it can apply its expertise to solve complex problems throughout the entire asset lifecycle. The company also stated that the market would continue to be demanding, and it is building clear momentum with significant contract wins and record work in hand. This places the company well in the medium and longer-term, underpinned by having the capability to successfully deliver for its shareholders on an ongoing basis..png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1:EV/Sales Multiple Approach.png)

EV/Sales Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

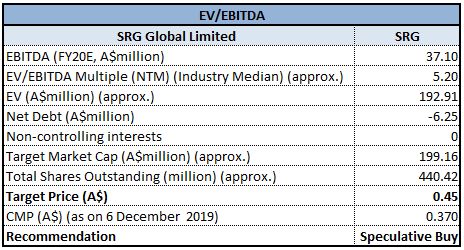

Method 2: EV/EBITDA Multiple Approach

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: The company has significant balance sheet strength which supports the foundation of future growth, and backed by tangible assets of $115.2 million. The group has an exceptionally diverse capability and skill set. Resultantly, the company could be involved in the entire lifecycle of an asset or project, from initial value engineering, through construction and then into ongoing maintenance. The company’s revenue base is becoming more and more diverse in geography and segment and the company has been maintaining focus towards revenue diversity in order to balance the earnings profile. Currently, the stock is trading at the lower band of its 52-week trading range of $0.285 to $0.620, proffering a decent opportunity for accumulation. Given the backdrop of decent fundamentals and growth prospects, we have valued the stock using two relative valuation methods, i.e., EV/Sales and EV/EBITDA multiples and arrived at a target price of lower double-digit upside (in percentage terms). Hence considering the aforesaid facts, valuations, and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current price of A$0.370 per share (down 1.333% on 06 December 2019).

SRG Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...