Kalkine has a fully transformed New Avatar.

Company Overview - Spotless Group Holdings Limited is engaged in the provision of outsourced facility services, laundry and linen services, technical and engineering services, maintenance and asset management services, and refrigeration solutions to various industries in Australia and New Zealand. The Company's segments include facility services, which provides multi-faceted facilities management, cleaning, and catering and food services to a range of industries across Australia and New Zealand, and laundry services, which provides linen and uniform laundry services to a range of customers across Australia and New Zealand. Its geographical segments include Australia and New Zealand. It serves industries, including business and industry, education, defense, leisure, sport and entertainment, health, infrastructure, and laundries among others. It offers services, such as catering and hospitality, grounds and gardens, and cleaning, among others. Its brands include Spotless, AE Smith, EPICURE and MUSTARD.

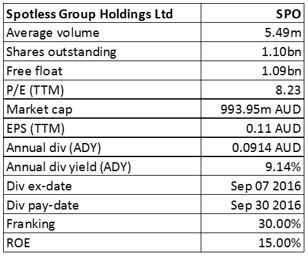

SPO Details

Fiscal year of 2016 performance highlights: Spotless Group Holdings Ltd (ASX: SPO) has reported 10.6% growth in the revenue for fiscal year of 2016 but EBITDA was down 1.5% for the same period. On the other hand, there is better growth in the underlying revenue and EBITDA which rose 17% and 6%, respectively. The revenue grew due to the stable performance of current business and the acquisition contribution. FY 16 results reflected the acquired revenue of $588 million as compared to FY15 figure of $185 million while acquired EBITDA reached $34 million against $8 million in fiscal year of 2015. Excluding the acquisitions, revenue and EBITDA in FY 16 include the benefit from contract wins and renewals offset of any impacts from the acquisition integration issues, mainly within Laundries business segment. Moreover, EBITDA is negatively affected by several items that include the large tender bid costs on two unsuccessful bids ($9 million) and the treatment change on bid costs ($5 million). SPO has maintained the underlying EBITDA margin in the Facilities Services business segment at 10.2% (which is 92% of revenue). However, the margins decreased from 31.0% to 24.2% during the period hurt by the underlying EBITDA margin in the Laundries business segment. Additionally, huge depreciation (largely due to increases from acquired businesses), mobilization costs and bid costs affected the underlying profit. The higher debt is on the back of the net Increase in finance costs. Meanwhile, the group reported a tax rate of 27% due to the effective tax rate of the 30% adjusted for deferred tax accounting movements.

.png)

Fiscal year of 2016 Performance (Source: Company Reports)

Business Investment: SPO from the last two years has been investing in the business significantly. SPO has committed $200 million to six acquisitions, invested in the working capital in the acquired businesses and invested the capital required to support delivery of the long-term contracts including PPP’s. The investments are done in the security, mechanical and electrical services, as well as water, power, lighting and other utility services. Further, SPO will continue to consider bolt on acquisition opportunities in the future and will focus on stimulating organic growth and managing down debt. In addition, SPO’s underlying operating cash flow is lower than FY 15 due to the one-off items, working capital funding and onerous contract impacts related to the recently acquired businesses, exit of a national food & beverage supply contract that has led in a one-off $14 million net outflow and the timing of year end payment cycles. Hence, to address this decrease in cash flow, SPO intends to have a greater focus on the free cash flow in the future.

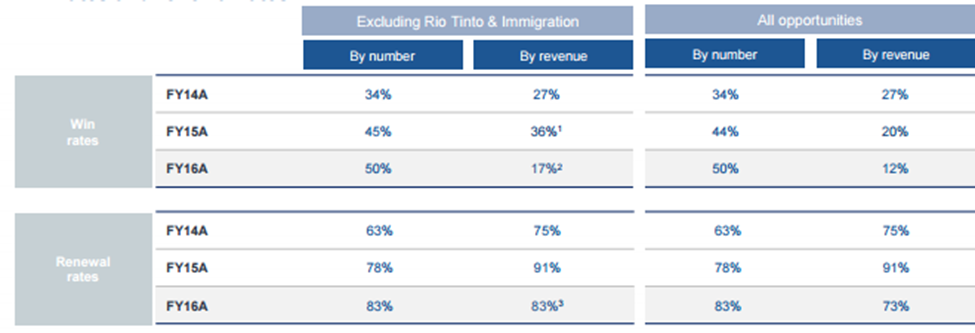

Negotiated solid renewals: In 2016, Spotless Group Holdings has negotiated over $480 million of renewals and built a $130 million of new contracts including the three further PPP contracts. Overall, SPO now has sixteen PPP contracts, seven of which are mobilizing in 2017. After the contracts are mobilized, these contracts would offer a great source of long dated stable earnings for SPO. On the other hand, FY16 was also impacted to a lesser degree by some major contract losses that include the Rio Tinto, Suncorp Stadium and the Western Properties contracts. The full year impact of these losses will carry into even fiscal year of 2017. On the other hand, Spotless Group is also enhancing the key account management to focus on renewals by implementing a customer centricity program focused on top 200 existing accounts.

Win rates and renewal rates (Source: Company Reports)

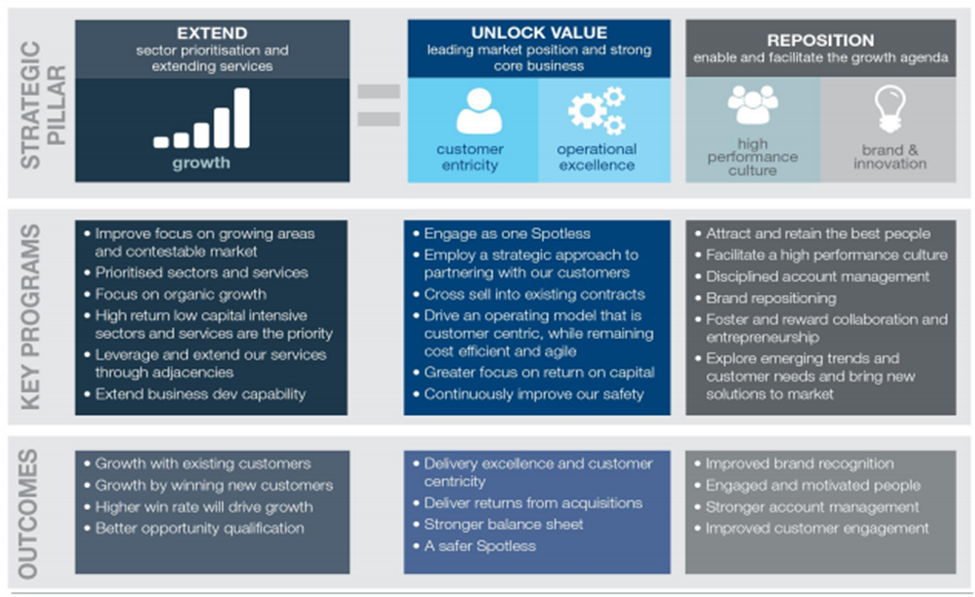

Strategy Reset: Spotless Group Holdings has completed the resetting of the strategy. The strategy is now focused on extending the breadth of SPO’s offer, unlocking the value and repositioning of the brand and employee value proposition to enable and facilitate the growth agenda. Moreover, SPO has prioritized cost reduction to improve the margins and acquisitions to build capability and drive growth for the company. For organic growth, Spotless Group is targeting sectors with the highest growth over the next five years and where appropriate margins could be achieved. The group is targeting decent growth sectors like health, aged care, education government and defense while Spotless Group Holdings would pursue long-dated, multi-service contracts that require comparatively low levels of capital relative to returns. Health, Education and government comprises 35% of the group’s business, while Commercial and Leisure accounts for 37%. Base and Township represents 19% of the group’s business and Laundry and Linen comprise 9%. SPO’s government segment continues to be strong and won a five-year renewal to maintain social housing for the NSW Land and Housing Corporation. Moreover, the group also got renewed and extended services at several District Health Board (DHB) contracts in New Zealand, including Capital & Coast DHB, Central Alliance and Canterbury DHB. Additionally, the growth strategy includes the innovation programs wherein technology would drive growth and enhance the customer experience. In fiscal year of 2016, SPO had introduced smarter solutions to the marketplace, which included automated guided vehicles in healthcare, food and drink ordering apps, as well as other data, lighting and electrical technologies into the service offering. Spotless had also reported about Mr Simon McKeon AO joining them as a non-executive Director from December 2016. By appointing Simon, the group aims to leverage his vast experience in several areas in business, academia and the not-for-profit sector.

Strategy Reset Complete (Source: Company Reports)

Outlook for fiscal year of 2017: The group’s growth is expected to come through the improved performance of the Laundries business, and from the recently acquired businesses, which started to win PPPs recently. Growth is also expected from seven PPPs that are currently mobilizing, price escalations in current contracts and greater focus on free cash flow conversion. Moreover, there would be growth from the new wins in a steadily growing contestable market and by the conversion of the current pipeline of more than $1.3 billion of opportunities. Additionally, there are no significant contract renewals that would materially affect fiscal year of 2017.

Stock Performance: The shares of Spotless Group Holdings stock fell over 17.33% in the last six months (as of December 05, 2016) due to their lower than estimated guidance for fiscal year of 2017. Investors were expecting for better contracts win while the group lost major contracts. On the other hand, the short-term issues outlined in the December trading update and reflected in this result have been resolved. Since the IPO in 2014, the earnings have increased at a compound annual growth rate of 10.8%. Moreover, the heavy fall in the stock placed them at lucrative levels wherein the stock is trading at a very cheap P/E and a high dividend yield. SPO’s underlying business is strong and the pipeline of opportunities has the potential to re-stimulate organic growth going forward. SPO is focusing on defense sector while implementing several cost-efficient and innovative solutions across their cleaning and food businesses. Despite facing some pressure in the integration, we believe that their acquisitions would contribute to their performance further. Moreover, the rate of growth of SPO would be driven by the success and timing of the strategy of their reset initiatives, and from the recent investment in business development resources. Even though, investors were disappointed with the guidance, SPO still has a solid pipeline of more than $1.3 billion. Although there are risks relating to impacts from a tight fiscal policy, the group is well positioned to benefit from the outsourcing market with a solid growth as more and more organisations are expected to seek services to improve their productivity and lower operational costs. Long-term contracts are also expected to add to earnings. We give a “Buy” recommendation on the stock at the current price of – $ 0.95

SPO Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...