Kalkine has a fully transformed New Avatar.

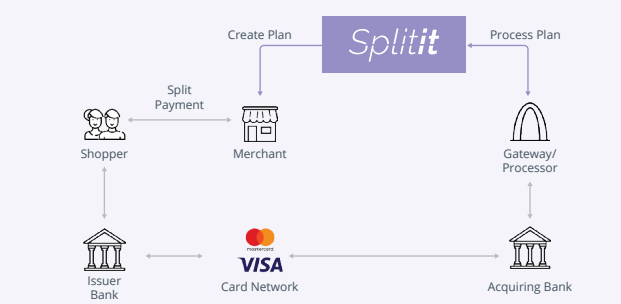

Company Overview: Splitit Payments Ltd. is an Israel-based company that offers payment solutions. It offers Splitit, a payment method solution enabling customers to pay for purchases with an existing debit or credit card by splitting the cost into interest-free monthly payments, without the need for additional registrations or applications. Splitit enables online retailers to offer their customers a way to pay for purchases in installments with instant approval, decreasing cart abandonment rates. The Company serves approximately 800 merchants in more than 20 countries.

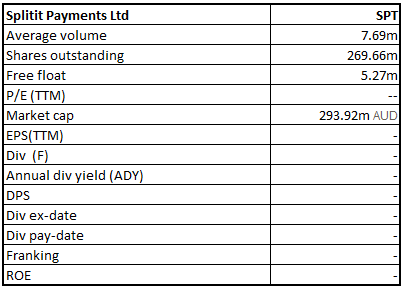

SPT Details

Unique Revenue Generation Model: Splitit Payments Ltd (ASX: SPT) has a unique revenue generation model. Revenues in FY18 were derived from transaction fees (Merchant fees) in relation to transactions processed through the Splitit Payment Platform. Merchant fees were generated on each approved order placed via the Splitit Payment Platform and are primarily based on a percentage of the end customer order value plus a fixed fee per installment.

The company operates into two business models to generate revenues, a Funded Model and a Basic Model. Under the funded model, merchants receive the full purchase price upfront. The full amount is transferred to the Merchant net of Merchant fees payable to Splitit and financing fees representing the interest cost payable to the funder (third-party financial institution). The fund provider provides the liquidity to the transaction and receives financing fees in return. The company collects amounts owed by the merchants to the fund provider but bears no credit risk. In case of default by the merchant, the funder will incur the credit losses without consequences to Splitit. Fees collected upfront are recognized on a straight-line basis over the funding period. Under the basic model, merchants provide the liquidity. The shopper pays directly to the merchant. Splitit will invoice the merchant on a monthly basis. Revenues are recognized on issuance of the monthly invoice. From the analysis front, the group has recorded Active Merchants growth at CAGR of 58.0 percent over the six quarters (Q4FY17-Q1FY19) and will continue to increase in years to come. We expect that the accelerated pace of Active Merchants additions and growth in payment solution business will support revenue growth in the upcoming years.

Splitit Use Case (Source: Company Reports)

An Insight into The Merchants & Partners: The company developed new merchant relationships in the US, UK, France, Italy, Australia and Singapore and others in 2018. Its pipeline of signed merchants in the process of integration is substantial which includes several large high-turnover merchants. These include merchants from several industry verticals including fashion, power tools, medical and jewellery, demonstrating the broad appeal of Splitit’s solution.

Additionally, the company has over 500 merchants currently engaged in various parts of the sales cycle including large global enterprise merchants. Most of these merchants come from the target markets of the US, Canada, Australia, UK, Italy, France and Singapore, with inbound enquiries and opportunities from many other countries. In our view, the rise in merchants will support to maximize its product fit, thus, resulting to revenue growth.

Merchants (Source: Company Reports)

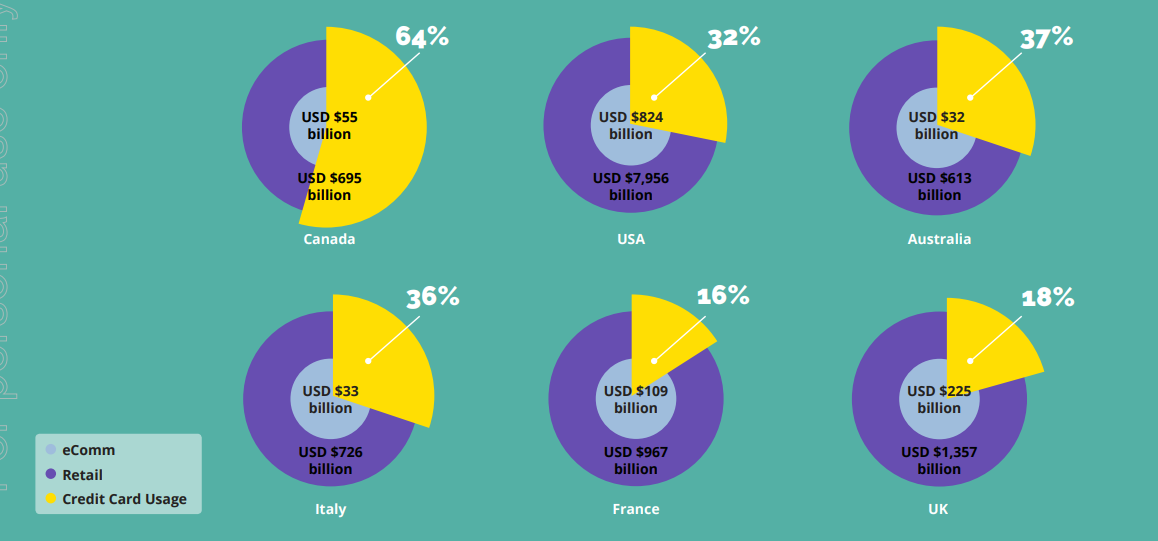

Untapped Addressable Opportunities: The company has a vast untapped market with addressable opportunities within its key markets of ~USD4.5 trillion. The credit card market has a huge exposure of ~64.0% in Canada followed by Australia, Italy, and the USA with 37%, 36% and 32% respectively.

Addressable Opportunities (Source: Company Reports)

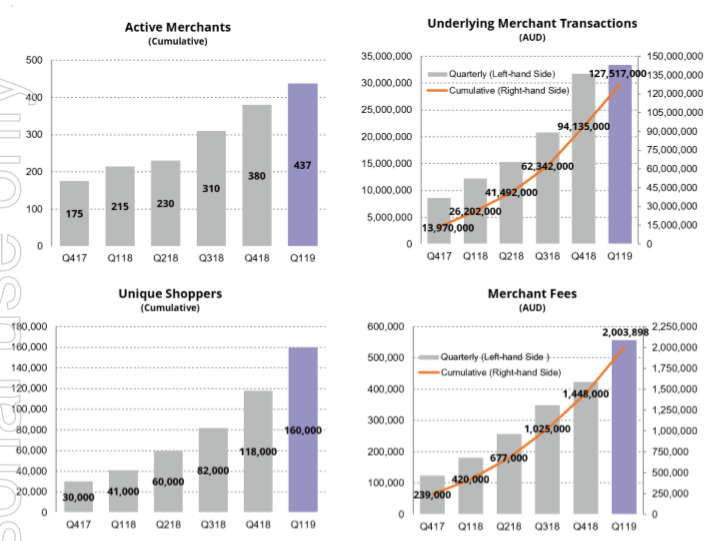

Significant growth in key performance metrics: As per the quarterly release as on 29 April 2019, the company currently has processed over 160,000 purchases and AUD$128 million of Underlying Merchant Transactions till the date without incurring any losses from bad debt during its operating history. It exhibits the business model and solution are robust and prone to lower risks. The company continued to experience strong growth across its key performance metrics during the first quarter of 2019. Given the seasonality with the March quarter typically being the slowest quarter for retail sales across the industry, the numbers look impressive for the company since it only completed the initial public offering on 29 January 2019.

The number of Active Merchants and shoppers continued to increase, delivering significant growth in Underlying Merchant Transactions and subsequently merchant fees. 57 new Active Merchants and 42,000 new Unique Shoppers started using Splitit in the March quarter, an increase of 103% and 290% year-on-year respectively.

Total Underlying Merchant Transactions since launch to the end of Q1 CY19 reached AUD$127 million, with the Q1 CY19 period alone delivering AUD$33 million, up by 3% on the previous quarter and 168% on a year-on-year. There has been an increase in total merchant fees since launch to Q1 CY19 and it stood at AUD$2 million with the March quarter being a record month for the company, reaching a total of AUD$556k. Merchant Fees are up 31% on the previous quarter and 207% year-on-year.

Key Metrics Performance Q1 2019 (Source: Company Reports)

Successful Funding Through IPO: In January 2019, the company completed an initial public offering in Australia, resulting in a capital raising of AUD $12 million. Until now, the company has only used third-party funding facilities to upfront merchants on the funded plans. It has established agreements with funding partners in the US and UK and a recently signed USD$25 million frameworks with a UK credit fund that includes some European countries.

Currently, the company is in advanced discussions with multiple additional third-party funding facilities, to enhance growth in demand for funded plans by new and existing merchants. Meanwhile, the company has established enough credit facilities with third parties to meet the current demand which cannot be fulfilled by its existing third-party credit providers. The company intends to maintain a Self-funding Arrangement by keeping a reserve up to USD$3 million for Funded Plans for approved merchants.

Key Financial Highlights: On the financial performance front, the company reported a net loss after income tax of ~USD$4.64 million as compared to ~USD$3.42 million in FY17. The sales income for the financial year stood at USD$789,920, up from USD$260,409 in FY17, exhibiting a substantial increase. The sales income was primarily comprised of merchant fees. Gross profit on sales revenue increased by 561% to USD$389,793 as compared to USD$58,914 in FY17. There was an increase in operating expenses by 29% to USD$3,899,387 as compared to USD$3,012,141 in FY17.

The company resorted to heavy debt funding evident by the substantial increase in financing expenses by 141% to USD$1,131,502 as compared to USD$468,409 in FY17. This is mainly due to the revaluation of convertible loans, share based payments expense of USD$378,921 as compared to USD$351,383 in FY17 representing the value attributable to the issue of options to employees.

On the cash flow front, the company reported net operating cash outflow of AUD$3.58 million during the quarter ended 31 March 2019, which included cash received from customers of AUD$454k on the back of fees and net repayment of upfronted purchase amounts under the Self-funding Arrangement. It has an outflow of AUD$792K for advertising and marketing, which included attending the global premier retail conference ShopTalk in Vegas and various media campaigns. The company had an outflow of AUD$696K in corporate and administration costs, which include higher than usual one-off legal and accounting costs associated with the initial public offering and preparation of the FY2018 annual report. The company expects it to come down to AUD$286K in the June quarter. The company received AUD$12.39 million in net financing cash flow driven by a successful initial public offering to list on 29 January 2019 raising AUD$12 million from warrants that were exercised. It had reported AUD$9.18 million in cash as at 31 March 2019.

Key Ratios: Current ratio in FY18 improved to 0.20x as compared to 0.10x in the previous year primarily on the back of higher growth in current assets. The asset-turnover improved by 17.2% to 0.35x as compared to 0.30x in the previous period along with fixed asset turnover ratio improving by ~28.8% over the period demonstrating the strong efficiency of the company to generate revenues utilizing its assets base.

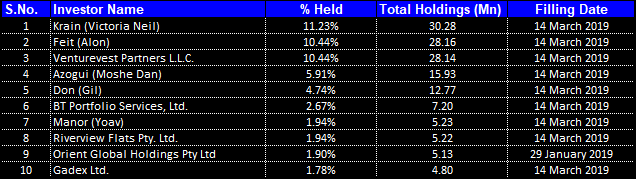

Top Ten Shareholders: The top ten stakeholders in the company forms ~53.0% of the total shareholding as highlighted in the below table. Krain (Victoria Neil) and Feit (Alon), Venturevest Partners L.L.C holds maximum interest in the company with individual stakes of 11.23% and 10.44% and 10.44% respectively, followed by Azogui (Moshe Dan) and Don (Gil) with 5.91% and 4.74% stakes respectively.

Top 10 Shareholders (Source: Thomson Reuters)

Outlook for the Business, Going Ahead: The company is seeking to accelerate its merchant acquisition strategy by identifying several target countries to focus its sales and marketing efforts, including, the US, Canada, UK, Italy, Singapore and Australia. The company will focus on specific areas like Medical, High-End Fashion, Sports Equipment, home-goods and Travel & Leisure. Medical will include cosmetic, dentistry, aesthetic and fertility medicine. Fashion will be including luxury clothing brands, jewellery and watches. Sports equipment will have a focus on electric skateboards, kite surfing, golf equipment and mountain bikes. However, home-goods and travel & leisure will have mattress & furniture and airlines & hotels respectively.

Moreover, the company focuses on leveraging on its partnerships and continue to invest and build strong partnership networks with eCommerce platforms, payment processors, technology services and point of sale providers along with banks and large multinational corporations. It will invest further in platform innovation by developing new advanced product features and continue to promote financial freedom and responsible spending for every lifestyle. Moreover, global expansion remains one of the key focus of the company.

The company has a strong sales outlook for FY19with focus on acquiring market share with high ticket merchants. It will continue with its strategy to win the customer first and will expand its activity within existing strategic merchants to spread greater awareness among industries. Lead generation from events and establish independent sales organizations with a strong history of success is among the key focus of the company to enhance sales.

Company Outlook (Source: Company Reports)

Stock Recommendation: The stock was volatile yielding a return of 60.29% over the past six months along with a negative return of 11.38% over the past month. It has a market capitalization of ~$293.92 million as on 3 May 2019. Although the business incurred losses in FY18, however it was able to improve its margins with respect to the previous years. The company evidenced significant increase in operational expenses comprising SG&A, labor related expenses underpinned by growth in operations. Moreover, the financial expenses increased substantially back of convertible loan revaluation. From technical perspective, on 29th April 2019, SPT made a gap up opening and shot up to more than 25% during the same session on account of March 2019 quarterly report. This massive rise was accompanied with exponential increase in the traded volume (~28.11 million), compared to the 20 days average volume of ~5.1 million. After the rise, the stock has been consolidating in a narrow range of A$1.13 – A$1.00 which is a sign of accumulation by the market participants, which generally is seen in such a scenario.

Strong revenue performance, backed by improving asset utilization along with several opportunities for expansion based on decent fundamentals, indicate for better prospects of the company. Further with significant growth in the key performance metrics over the last quarter, we believe the company has shown some signs of moving on track, although it is in early stages of the business. Hence, we recommend a “Speculative Buy” rating on the stock at the current market price of $1.075 (down 1.376% on 3 May 2019).

SPT Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...