Company Overview - Spark Infrastructure Group is an Australia-based company, which is engaged in investment in regulated electricity distribution and transmission businesses in Australia. The Company operates through four segments: Victoria Power Networks, SA Power Networks, TransGrid and Other. Victoria Power Networks holds interest in two electricity distribution businesses in Victoria, which include CitiPower and Powercor. SA Power Networks holds interest in the electricity distribution business in South Australia and supplies energy to approximately 847,000 customers. TransGrid holds interest in the electricity transmission business in New South Wales, which include NSW Electricity Networks Assets Holdings Trust (NSW Electricity Networks Assets) and NSW Electricity Networks Operations Holdings Trust (NSW Electricity Networks Operations). Other represents the economic interest in DUET Group. The Company also invests in regulated water and sewerage assets.

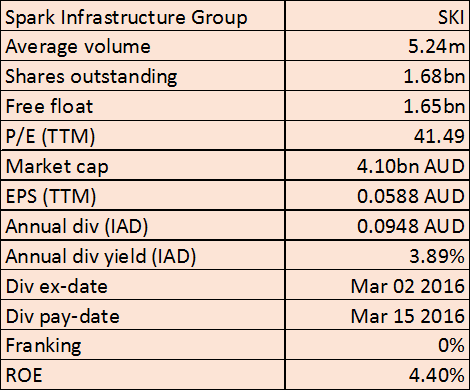

SKI Details

Organic growth to expand business: Spark Infrastructure Group (ASX: SKI) is focusing on organic growth apart from its growth from acquisitions. SKI has been improving its efficiency, productivity and managing costs along with positioning with the changing business condition and new technology. Meanwhile, the Group would also consider external growth and diversification if the opportunity provides attractive yield and cash flow accretion in a reasonable timeframe. SKI has built diversified high quality regulated assets base over the years. The Group has 49% holding in each businesses of SA Power Networks, CITIPOWER, and Powercor while 15.01% in TransGrid. SA Power Networks (SAPN) is the only operator of South Australia’s electricity distribution network, for over 852,000 residential and commercial customers in all regions and the major population. CitiPower operates the distribution network providing electricity to about 326,000 customers in Melbourne’s CBD and inner suburbs.Powercor is a major distributor of electricity in Victoria, which serves about 768,000 customers in central and western Victoria and the western suburbs of Melbourne. SKI acquired stake in TransGrid on December 2015 for a consideration of $735.3 million. TransGrid is a major high-voltage electricity transmission network in the National Electricity Market (NEM) by electricity transmitted, with connecting generators, distributors and major end users in NSW and the ACT and forms the backbone of the NEM connecting QLD, NSW, VIC and the ACT.On the other side, each of SKI’s investment portfolio has embraced new technologies and is focused on innovative solutions to emerging business challenges. SAPN has Network Innovation Centre, VPN has Energy Solution Business unit and TransGrid has iDemand Pilot Project catering customer focus innovative solutions. However, Spark Infrastructure has divested 8% of economic interest in DUET Group at a price of $2.25 per security on May 30, 2016. With the divestment, SKI would fully exit all of its derivative position held under contract with Deutsche Bank. The decision has been taken after the investment in TransGrid.

Performance overview of the group’s investments (Source: Company Reports)

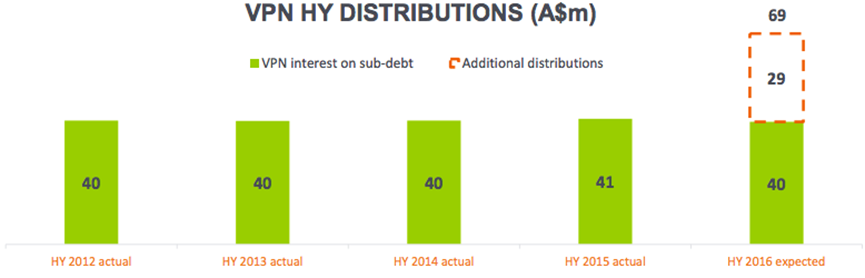

Reliable long-term distribution growth: SKI’s ability to provide reliable long-term distribution growth coupled with the ability to deliver its estimates is central element in company’s investment proposition. SAPN and VPN are at a satisfactory finalization of their regulatory reset processes and successfully de-gearing their balance sheet. Moreover, as per company’s releases, AER has confirmed the rankings of SAPN, CitiPower and Powercor together known as Victoria Power Networks (VPN) in its Benchmarking report published in November 2015. The AER has ranked these three businesses in the top five electricity distribution networks for operational efficiency, with CitiPower ranked first for both operational and capital efficiency while South Australia is ranked as the most efficient State on a State-by-State comparison. Accordingly, the group generates most of its growth from VPN which is now paying ordinary distributions (further to the non-discretionary sub-debt interest) for the first time since 2011. SKI would also be adding contribution from the new investment in TransGrid. VPN is forecasted to distribute $69 million to Spark Infrastructure for the first half of 2016, which is $29 million (68%) more than the recent prior periods (based on agreed business plans). In addition to this, a further $69 million is scheduled to be paid in the second half of 2016. The group reported that they have included the forward distributions to Spark Infrastructure from VPN and SAPN to 2020 into their relevant 5-year business plans. Meanwhile, Transgrid distribution to SKI is expected to be ~$45 million for FY16.

VPN distributions projections (Source: Company Reports)

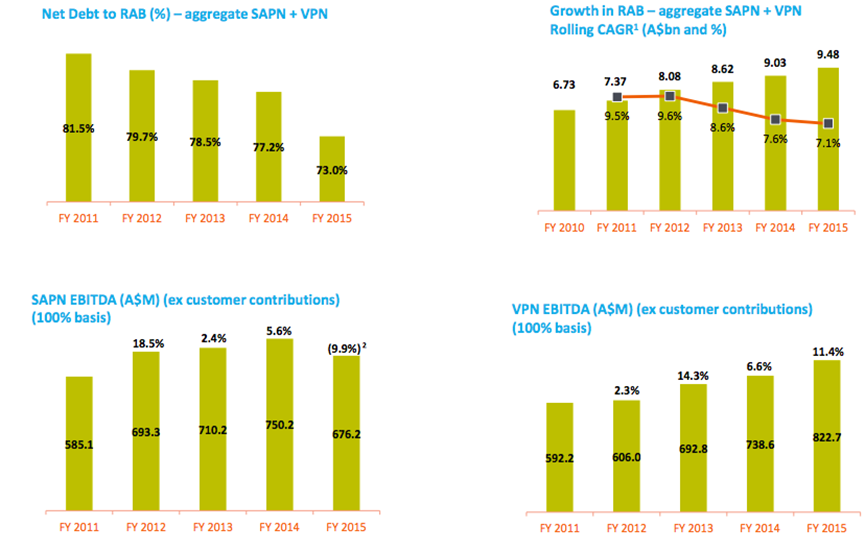

Fiscal year of 2015 performance: The group generated overall distributions growth of 3.1% yoy to $229 million in fiscal year of 2015. Accordingly, the standalone operating cash flow rose by 0.2% yoy to $207.4 million in fiscal year of 2015. Spark Infrastructure dividend per share rose by 4.3% on a yoy basis to 12 cents per share in fiscal year of 2015. Standalone payout ratio enhanced by 4.1% to 85.6% in FY15 from 81.5% in FY14. VPN distributions to Spark rose 1.2% yoy to $82.2 million in FY15. Standalone Operating cash flow improved by 0.2% yoy to $207.4 million while Lookthrough OCF per security (post Spark Infrastructure costs) enhanced by 14.7% yoy to 28.9 cents per share in FY15. VPN EBITDA rose to $822.7 million in FY15 as compared to $738.6 million in FY14. VPN (distribution growth is significantly contributing to SKI’s standalone cash flows along with the new investment in TransGrid. Meanwhile, the group’s recent capital raising would add strength to the balance sheet after its TransGrid transaction. The balance sheet and future visibility of operating cash flows enables the group to weather any short term uncertainty. The company has guided a total dividend of 12.5 cents per share for FY16.The group reported a net debt to RAB of 73.8% as of December 2015 and has a BBB+ credit rating from S&P.

SKI track record performance (Source: Company Reports)

Fund raising through bond issue: Recently, TransGrid’s funding entity, NSW Electricity Networks Finance Pty Ltd have placed US$700 million and A$75 million of bonds into US private placement market to four tranches which includes US$ 200 million maturing in September 2026 (10- year), US$ 250 million maturing in March 2029 (12.5 year), US$ 250 million maturing in September 2031 (15 year) and A$75 maturing in September 2033 (17 year). These funds would be used to repay for full bank debt bridge facility, which is due for expiry reducing debt from balance sheet. The group’s investment in TransGrid is forecasted to be value accretive and offer long term cash generation growth opportunities while the delivery of the consortium’s business plan is on track. The group estimates TransGrid to get a secured near term solid investment grade credit rating.

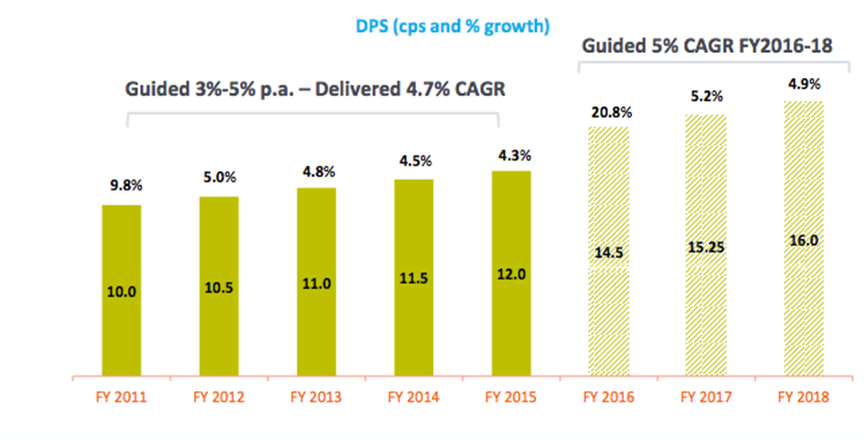

Positive guidance: Management guided that their distribution would reach 14.5 cents per share in FY16, 15.25 cents per share in FY17 and 16 cents per share for FY18, which is a revision by 15% from its earlier guidance. The true-up of revenue reflecting SPAN’s final determination has commenced from July 01, 2016 with an additional $630 million to be recovered in 2-5 years of regulatory period. For VPN, true-up of revenue would commence from January 01, 2017 with an additional $180 million to be recovered in 2-5 years of the regulatory period.SKI forecasts an additional real growth in RAB over next 5 Year Regulatory Period. Gearing of 75% net debt to RAB through to 2015 has been achieved in SAPN and VPN and management estimates the similar level, as agreed between partners. Meanwhile, the group expects no equity injections for SAPN and VPN in current regulatory periods (2015-20). TransGrid gearing is forecasted to remain around current range over the medium term, as agreed between partners.

Guidance for dividend per share (Source: Company Reports)

Stock performance: The shares of SKI surged 32.74% in the last six months (as of July 08, 2016) driven by strategic investments. SKI estimates its SAPN and VPN to continue deliver strong performance with management of regulatory appeals for SAPN and potentially VPN. The group is focusing on growth and development of Energy Solutions business unit in VPN and other innovations and trials in SAPN. For the TransGrid investment, the group is focusing on embedding transformation program and implement the NSWEN Consortium business plan based on operational productivity and efficiency. The group is preparing for its next regulatory proposal due for submission in January 2017 for TransGrid while Enterprise Agreement negotiations were said to start in the third quarter of 2016. Given the strong prospects, we give a “Buy” recommendation on this dividend yield stock at the current market price of $2.45

SKI Daily Chart (Source: Thomson Reuters)

Disclaimer The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

.png)

Please wait processing your request...

Please wait processing your request...