Stock of the Day – Spark Infrastructure (SKI)

Despite strong regulated tariff increases. Spark infrastructure’s revenue increased just 1.7% in the first half 2014. The main detractors were soft volumes and lower unregulated revenue. Operating cost were relatively well contained at the underlying networks increasing just 1%. A cost reduction program should keep the cost under control. Proportionate EBITDA increased 2% to AUD 347 million, tracking below expectations on the softer than expected revenue.

EBITDA + RAB (Source – Company Reports)

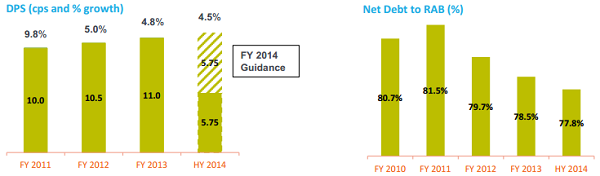

Regulatory asset base or RAB continues to grow at a good clip up 6% on June last year on elevated capital expenditure. With growth being funded by a relatively conservative mix of retained earnings and debt, balance sheet continues to improve. Gearing measured as net debt to RAB is 77.8% down from 78.5% in December 2013. The target is to reduce gearing in the underlying assets to 75% by 2015. We believe Spark’s balance sheet is sound and the target gearing will put them in good positions to weather tough regulatory settings.

DPS + Net Debt (Source – Company Reports)

The tough regulatory environment further reduces the potential for sustainable excess returns. Spark look overvalued at present. Likely tough regulatory resets in 12 to 18 months will be material headwinds tow earnings. This may not require distributions to be reduced as the currently conservative payout ratio provides a buffer but with capital expenditure likely to remain high a small cut can’t be ruled out.

SKI Daily Chart (Source – Thomson Reuters)

Volumes can be volatile and fluctuate with weather and other factors, causing earnings to jump around. In the current environment of falling demand as a result of increased solar penetration and more energy efficient homes and appliances, the regulator must increase tariffs to ensure utilities earn a fair return. Historically utilities could over or under earn for a while given the regulator only adjusted demand expectations every five years at regulatory resets. Unregulated revenue can be lumpy driven by large customer initiated projects. Completion of the Elaine Terminal station caused a 25% reduction in unregulated revenue at the Victoria Power Networks or VPN while reduced spending by customer Electranet caused an 8% reduction at the South Australia Power Networks or SAPN. Unregulated revenue was at elevated levels in recent years. We put a SELL recommendation on the stock at the current price of $1.87.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...