Company Overview - Spark Infrastructure Group is an Australia-based company is engaged in the investment in electricity distribution businesses in Victoria and South Australia. It operates in two segments: Victoria Power Networks, which represents the 49% interest in two electricity distribution businesses in Victoria (i.e. CitiPower and Powercor) and SA Power Networks, which represents the 49% interest in the electricity distribution business in South Australia. The Company’s controlled entities include Spark Infrastructure (Victoria) Pty Limited, Spark Infrastructure (South Australia) Pty Limited, Spark Infrastructure SA (No 1) Pty Limited, Spark Infrastructure SA (No 2) Pty Limited and Spark Infrastructure SA (No 3) Pty Limited.

Analysis – With continued investment in the regulated asset base Spark Infrastructure increased proportional revenue 9% to AUD 1.03billion. Proportional earnings before interest, tax, depreciation and amortization or EBITDA increased 8% to AUD 679 million and earnings increased 15% to AUD 226 million. The overall result was in line with expectations but regulated earnings were a little soft because of warm winter weather while unregulated earnings were higher than expected because of expansion of services in New South Wales. In our view the key take away from the CY13 result was the greater resolve of management to solve the asset tax disputes with the ATO as early as possible. SKI’s comment that it does not see risks tor its dividend to 2015 accords with our view. Resolution of the tax disputes offers further re-rating potential. While not quite as strong as we had hoped the cash flow generation of the assets is strong despite softer electricity volumes and remains a feature of the SKI investment proposition.

Spark infrastructure owns 49% of three major Australian regulated electricity distribution networks. We like its secure earnings, material regulated operations and internal management. Citipower and Powercor are two of five electricity distributors in Victoria while SAPower Networks is the sole electricity distribution in South Australia. The Victorian networks contribute just under half of revenue and earnings before interest, taxes, depreciation and amortization EBITDA with the rest coming from South Australia. Regulated distribution tariffs accodu4nt for 80 to 90 % of group revenue with unregulated and semi regulated services accounting for the balance. Unregulated includes services on other owner’s networks, asset rentals and facilities access. These operations are generally higher margin and more volatile. Semi regulated include public lighting and meter reading. Regulated revenue is highly secure and predictable between regulatory resets. Volume risk only exists insofar as volumes differ from the regulator’s forecasts. While not a major risk in the past rising utility bills could cause volumes to serially miss expectations. In future regulatory periods volume risk may be eliminated by switching to a revenue cap system that changes tariffs to offset volume fluctuations. Unregulated and semi regulated revenue can be lumpy particularly as a result of externally initiated projects. Overall group revenue is considered to be highly secure. Diversification is minimal as all regulated operations fall under the jurisdiction of the Australian Energy Regulator. Regulatory resets generally occur every five years in Australia and are staggered for different assets smoothing the impact of major changes.

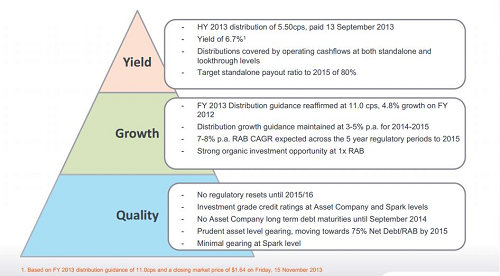

SKI Outlook (Source – Company Reports)

SKI Outlook (Source – Company Reports)

Revenue in South Australia grew 2.8% as solid tariff increases were mostly offset by soft volumes. Residential volumes fell 6% while business posted slightly higher volumes. Soft residential volumes can be attributed to warm winter weather and the ongoing reduction in energy demand caused by rooftop solar panels, high electricity prices, improved energy efficiency of appliances and improved home insulation. Victoria performed well with revenue up 15% on regulated tariff increases, strong growth in the unregulated services business and some one off items. These positives comfortably offset weak volumes across residential and business customers. Operational performance remains good resulting in financial bonuses. Following regulatory resets in coming years, Spark’s regulated businesses are likely to move to a new tariff setting system to remove exposure to positive and negative volume fluctuations. This will result in greater revenue stability and predictability.

SKI Daily Chart (SOurce - Thomson Reuters)

SKI Daily Chart (SOurce - Thomson Reuters)

|

Dividend |

|

Yield |

6.63% |

FY |

|

|

8.14% |

5yr Av |

Spark’s tax audit is ongoing and no material new information was provided. The impact on the South Australian business is not expected to be material. The impact on the Victorian business is greater and this business has nearly run out of carried forward tax losses, suggesting further tax claims will require cash payments. Spark’s balance sheet is robust. Gearing is higher than some peers but spark’s financial position is helped by material unregulated revenue. Gearing is 78.5% down from 79.7% at the same time last year and expected to fall to 75% by the end of 2015 because of retained earnings.

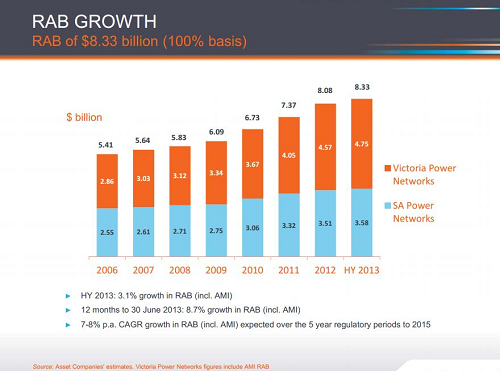

Regulated Asset Base Growth (Source – company Reports)

Regulated Asset Base Growth (Source – company Reports)

Spark is a solid company with investments in Australian electricity distribution networks generating highly secure cash flow under a transparent regulatory regime. Capital expenditure on upgrading and expanding networks adds to the regulated asset base (RAB) and will drive revenue higher in the long term. EBITDA margins are solid (66%in 2013) and are likely to improve in the near term. Profitability can fluctuate with volumes but the main determinant is the favorability of regulatory decisions. RAB growth remains robust with +6.6% during the fiscal period taking it to A$8.6bn with SKI’s share being A$4.2bn. Overall Group RAB should grow at 7-8% compound annual growth rate. FY13 of dividend Per Share of 11 cents per share was in line with expectations and represented a 77.1% payout ratio on a standalone basis. Management provided FY14 Dividend Per Share guidance of 11.5 cents per share implying a 6.4% yield at current levels and reaffirmed its commitment to 3-5% DPS growth in 2015 with the DPS to be fully covered by operating cash flows. With no resets until 1 January 2016 SKI is continuing to benefit from past resets with Victoria Power Networks in particular enjoying a strong regulated pricing path over the next two years and Group RAB growth of around 6% expected over the same time frame. We see upside should SKI continue to outperform regulatory benchmarks. We like the SKI story and would be putting a BUY at the current price of $1.66.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...