Company Overview: South32 Limited is a metals and mining company. The Company's segments include Worsley Alumina, which includes an integrated bauxite mine and alumina refinery in Western Australia; South Africa Aluminium, which includes an aluminum smelter in Richards Bay; Brazil Alumina, which includes an alumina refinery in Brazil; Mozal Aluminium, including an aluminum smelter in Mozambique; South Africa Energy Coal, including open-cut and underground energy coal mines and processing operations in South Africa; Illawarra Metallurgical Coal, which includes underground metallurgical coal mines in New South Wales; Australia Manganese, which produces manganese ore in the Northern Territory and manganese alloys in Tasmania; South Africa Manganese, which produces manganese ore and alloy in South Africa; Cerro Matoso, including an integrated laterite ferronickel mining and smelting complex in Colombia, and Cannington, including silver, lead and zinc mine in Queensland.

.png)

S32 Details

Decent Financial Performance for years FY14-19: South32 Limited (ASX: S32) is engaged in the mining and production of metals such as aluminium, bauxite, alumina, metallurgical coal, energy coal, manganese alloy, metallurgical coal, nickel, silver, lead and zinc. It operates in geographies such as Australia, Southern Africa and South America. It also owns high-grade zinc, lead and silver development business in North America along with partnering junior explorers with focus on base metals. Looking at the past performance over FY14 to FY19, total revenue and net income of the company have grown with a CAGR (compounded annual growth rate) of 53.52% and 53.26%, respectively. Group’s total revenue improved from US$853 Mn in FY14 to US$7,274 Mn in FY19, and net income improved from US$46 Mn in FY14 to US$389 Mn in FY19.

Company’s disciplined way of capital allocation allowed it to return a further US$74 Mn with the continuation of its US$1.25 Bn capital management program, in addition to the US$139 Mn ordinary dividend in respect of the prior six months. It is well on track to finalise Seriti Resources’ offer for its South Africa Energy Coal business, which will be a significant milestone for the company in its divestment program and a further step towards reshaping the portfolio.

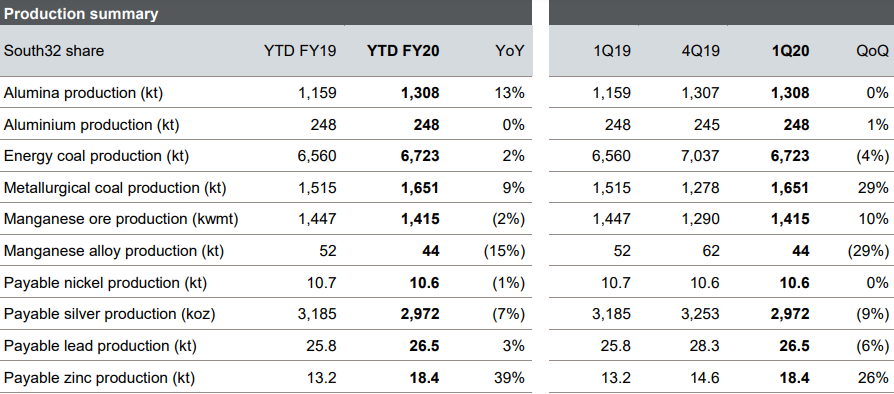

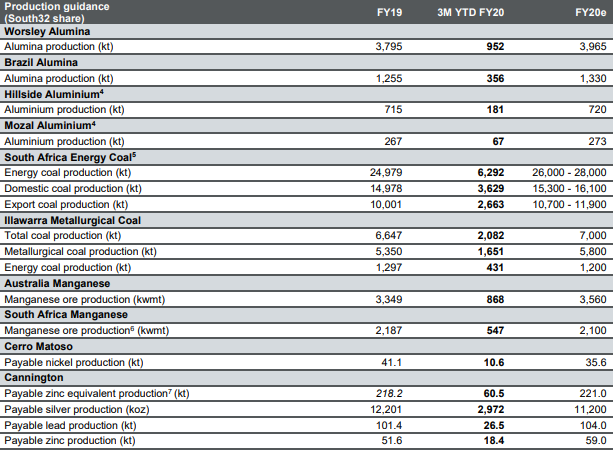

Under FY20 guidance, aluminum production at Worsley Alumina, Brazil Alumina, Hillside Aluminium and Mozal Aluminium is expected to increase on the previous year. Coal production from its South Africa Energy Coal project and Illawarra Metallurgical Coal project is also expected to increase on the previous year. Manganese production from Australia is also expected to increase, but to remain flat for South African production. Nickel production at Cerro Matoso is expected to decrease on the previous year. Production for other metals such as zinc, zinc equivalent and lead at Cannington is expected to increase whereas silver production is expected to decrease on the previous year..png)

Historical Business Performance (Source: Company Reports)

September’19 Quarter Key Highlights: Despite an increase in finished goods inventory during the period, the company benefitted from an unwind in working capital for on-market share buy-back leading to an increase in net cash by US$163 Mn to US$527 Mn. The company reported record production at Brazil Alumina and strong quarter at Worsley Alumina, highlighting its initiatives to sustainably increase to nameplate capacity from FY20. Moreover, despite the impact of load-shedding, S32 kept operating aluminium smelters at their maximum technical capacity.

As the longwalls continued to perform strongly with the completion of two moves in the prior quarter, production at Illawarra Metallurgical Coal improved by 30%. Its low-cost, flexible operations and commencement of exploration drilling in the Southern Areas target at GEMCO, helped the company to maintain higher rates of manganese ore production. Moreover, in order to increase its knowledge of the Taylor Deposit and greater land package, it invested US$17 Mn in exploration at its early stage greenfield projects and existing operations. During the period, the company negotiated with Seriti Resources regarding the acquisition proposal of its South Africa Energy Coal business and may update the market in the December quarter result.

Following the payment of US$115 Mn in royalties at Australia Manganese with respect to the previous two quarter period, the company received net distributions of US$63 Mn from its manganese equity accounted investments (EAI). On October 10, 2019, the Board of Directors declared fully franked dividend of US$139 Mn, with respect to the second half of financial year 2019.

Production Summary (Source: Company Reports)

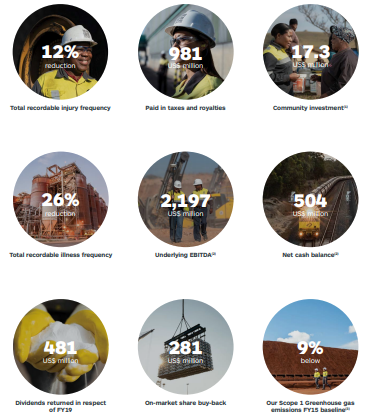

FY19 Key Highlights for the period ended June 30, 2019: Group’s statutory profit after tax was reported at US$389 Mn, a decrease of 71% on the previous year, following the acknowledgement of damage charges of around US$504 Mn (US$578 Mn after tax, including de-recognition of deferred tax assets) with regard to its South Africa Energy Coal operation. Underlying earnings for the period was reported at US$992 Mn, a decrease of 25% on the previous year. This was due to strong operating performance in terms of production volumes, and cost reduction initiatives across materials usage, energy and labour, offset by lower thermal coal prices and aluminium. Net cash balance at the end of the period was reported at US$504 Mn. Group’s free cash flow from operations declined by 35% to US$571 Mn, following investments in underground development at Illawarra Metallurgical Coal.

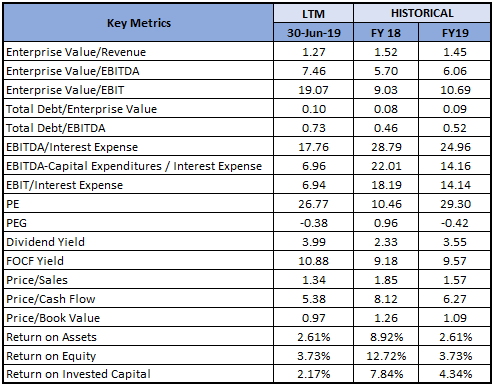

FY19 Key Metrics (Source: Company Reports)

Recent Updates:

(a) Recently, the company announced death of its Non-executive Director Dr Xolani Mkhwanazi on January 4, 2020, due to short illness. He joined S32 Board in July 2015, and previously held senior executive positions at BHP Billiton as Chairman of BHP Billiton South Africa and as President and Chief Operating Officer of South Africa Aluminium. He had also served Bateman Africa as senior executive and helped the National Energy Regulator in the formulation of the South African National Science and Technology Policy.

(b) In another update, the company informed the market about cancellation of its 28,389,692 ordinary shares at amount $77,661,456. With this share structural change, total number of the company’s shares stands out to be 4,899,731,136 at value $16,453,671,113.91.

(c) On December 20, 2019, S32 and Trilogy Metals Inc. together informed the market about the exercise of option to acquire a 50% interest in a Joint Venture (JV) that will own the Upper Kobuk Mineral Projects located in northwest Alaska, by South32. This JV will be retaining US$87.5 Mn out of subscription payment of US$145 Mn to fund its exploration activities with the balance of US$57.5 Mn loaned back to S32. The loan is expected to be repaid in instalments, subject to resource drilling, regional exploration programs and advance development studies.

(d) On December 13, 2019, S&P Dow Jones Indices announced the separation of S32 from S&P/ASX 20 Index, effective from December 23, 2019.

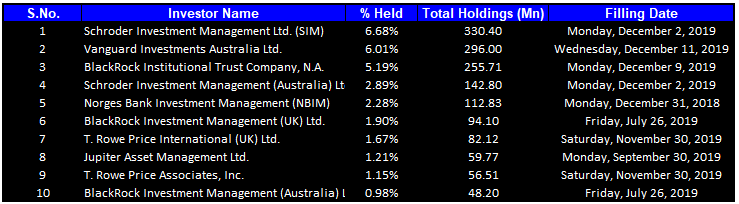

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 29.96% of the total shareholding. Schroder Investment Management Ltd. (SIM) and Vanguard Investments Australia Ltd. hold maximum interests in the company at 6.68% and 6.01%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

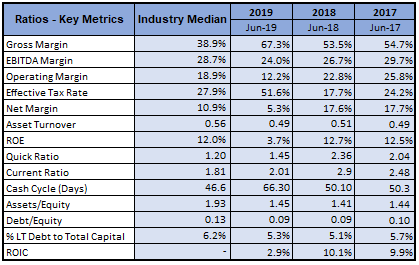

A Quick Look at Key Metrics: Its gross margin FY19 stood at 67.3%, better than the industry median of 38.9%. Its current ratio for FY19 stood at 2.01x, better than the industry median of 1.81x, which implies that the company is in a good position to address its short-term obligations. Its debt to equity multiple for FY19 stood at 0.09x, lower than the industry median of 0.13x.

Key Metrics (Source: Thomson Reuters)

Key Risks: The company is susceptible to certain risks such as actions by governments, political events or tax authorities; global economic uncertainty and liquidity; natural catastrophes; climate change; etc.

What to Expect: As per the release, S32 invested amount close to US$3 Mn to partner with companies to fund early stage greenfield exploration opportunities. Additionally, the company invested US$14 Mn for exploration programs, comprising funding for its existing operations (US$11 Mn capitalised) which included equity accounted investments worth US$1 Mn (all capitalized) and US$6 Mn at Hermosa (all capitalised) to further increase its knowledge of the greater Hermosa land package and the Taylor Deposit.

The company is progressing well for its Hermosa project pre-feasibility study, which is expected to complete by June 2020. The final investment decision for the Eagle Downs Metallurgical Coal project is expected to finalize by December quarter 2020 and is well supported by the advanced study work. Moreover, with the receipt of final regulatory approval, the company commenced exploration drilling in the Southern Areas at GEMCO, and the initial program is designed to test regional targets and to infill areas of known mineralization.

FY20 Guidance (Source: Company Reports)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price to Cash Flow Multiple Approach

Price to Cash Flow Multiple Approach (Source: Thomson Reuters), NTM-Next Twelve Months, *1 USD = 1.45 AUD

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Technical Analysis:

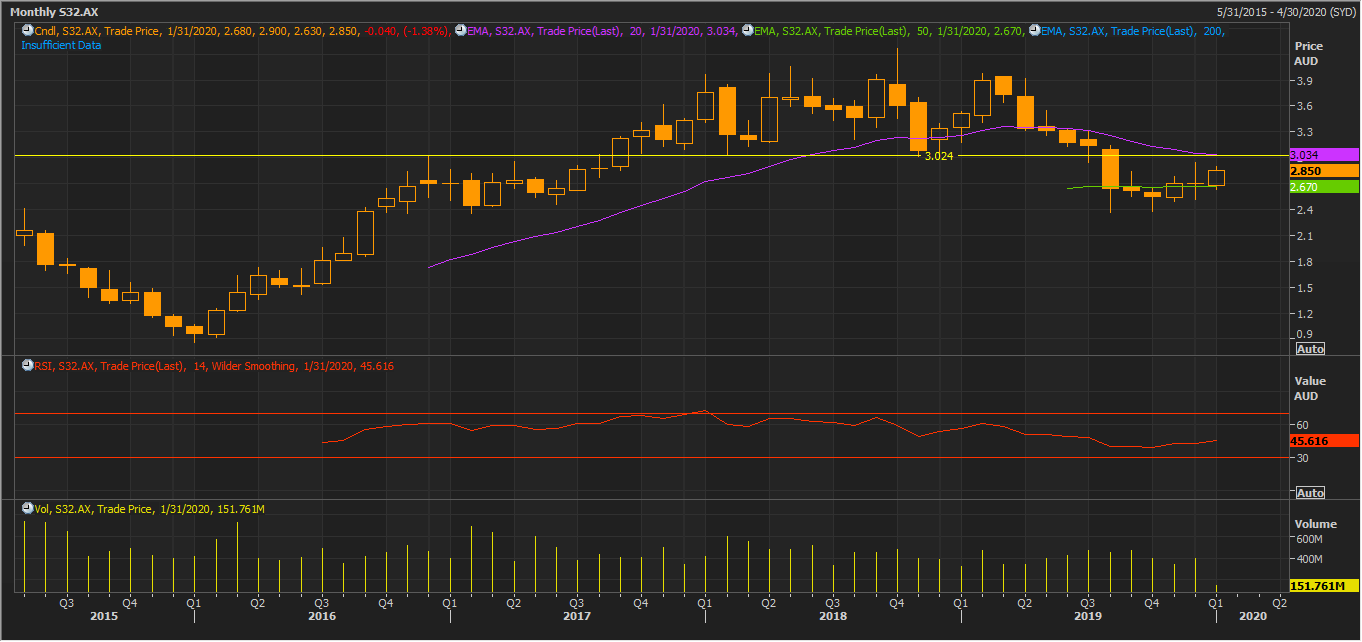

Monthly Chart:

(Source: Thomson Reuters)

Weekly Chart:

(Source: Thomson Reuters)

The stock crossed 20 EMA from below in both the weekly and monthly charts, suggesting that bearish trend may have bottomed-out whose confirmation can be arrived once stock price crosses 50 EMA. Strong resistance at around $3.024 can be expected as target one. It is supported by RSI (14 periods) value of 51.632 suggesting momentum building up at the present level.

Note: EMA – Exponential Moving Average, RSI – Relative Strength Index

Stock Recommendation: Company has maintained annual production guidance for all of its operations at its alumina refineries, underpinned by a 10% increase in manganese ore production and 30% increase in production at Illawarra Metallurgical Coal. With macro conditions favoring the key commodity prices, the company remains focused on its operating performance and driving cost across its portfolio. Considering the company’s business model, September’19 quarter results, FY19 performance, FY20 guidance, commodities outlook and current trading levels, we have valued the stock using a relative valuation method, i.e., price to cash flow multiple, and arrived at a target price of higher single-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$2.850 per share, down 1.384% on January 15, 2020.

S32 Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...