Kalkine has a fully transformed New Avatar.

Company Overview: South32 Limited is a metals and mining company. The Company's segments include Worsley Alumina, which includes an integrated bauxite mine and alumina refinery in Western Australia; South Africa Aluminium, which includes an aluminum smelter in Richards Bay; Brazil Alumina, which includes an alumina refinery in Brazil; Mozal Aluminium, including an aluminum smelter in Mozambique; South Africa Energy Coal, including open-cut and underground energy coal mines and processing operations in South Africa; Illawarra Metallurgical Coal, which includes underground metallurgical coal mines in New South Wales; Australia Manganese, which produces manganese ore in the Northern Territory and manganese alloys in Tasmania; South Africa Manganese, which produces manganese ore and alloy in South Africa; Cerro Matoso, including an integrated laterite ferronickel mining and smelting complex in Colombia, and Cannington, including silver, lead and zinc mine in Queensland.

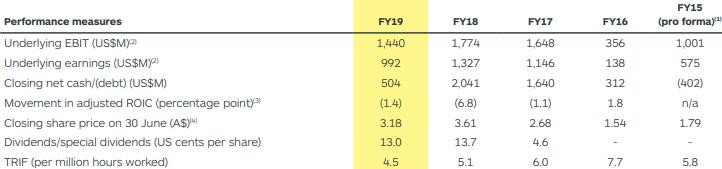

S32 Details

Nameplate Capacity for FY20 Expected To Increase Following Record Production for Sep Qtr: South32 Limited (ASX: S32) is involved in the mining and metal production, from a portfolio of assets including alumina, aluminium, bauxite, energy coal, manganese ore, manganese alloy, nickel, silver, lead and zinc. The company owns high-grade zinc, lead and silver development option in North America and has several partnerships with junior explorers with a focus on base metals.

Looking at the past performance over FY14 to FY19, total revenue and net income of the company have grown with a CAGR (compounded annual growth rate) of 53.52% and 53.26%, respectively. Group’s total revenue improved from US$853 Mn in FY14 to US$7,274 Mn in FY19, and net income improved from US$46 Mn in FY14 to US$389 Mn in FY19.

Lower aluminium and thermal coal prices led to a decline of 25% in FY19 underlying earnings. However, improving outlook for commodities and an increase in the group’s production volumes and cost reduction initiatives across labour, energy and materials usage are expected to boost the company’s earnings in the coming times.

Moreover, the company achieved record production at Brazil Alumina and Worsley Alumina in the September quarter, which is likely to help its initiative to increase the nameplate capacity from FY20. Illawarra Metallurgical Coal saleable production increased by 30% to 2.1Mt in the September 2019 quarter following the successful completion of two longwall moves in the June 2019 quarter.

Group’s production volumes are expected to rise by 3% in FY20 with assumptions such as Illawarra Metallurgical Coal returning to a three longwall configuration from H2 FY20; South Africa Energy Coal recovering from the dragline incident and commencing production from the Klipspruit Extension Project; an improvement in calciner availability at Worsley Alumina; and Brazil Alumina realising the full benefits of the Debottlenecking Phase One project, following the introduction of package boilers to improve the reliability in steam generation.

Past Financial Performance (Source: Thomson Reuters)

September’19 Quarter Key Highlights: Worsley Alumina hydrate production increased by 4% to 967kt as the hydrate circuit operated at an annualised rate of 4.5mtpa (100% basis), whilst alumina saleable production decreased by 4% to 952kt as a scheduled calciner shut was completed. Brazil Alumina saleable production increased by 14% to a record 356kt as the refinery benefitted from the installation of package boilers, enabling the benefits of the De-bottlenecking Phase One project to be realised. Hillside Aluminium saleable production increased by 1% to 181kt as the smelter continued to test its maximum technical capacity, despite a modest impact to production from load-shedding and the completion of a major workforce restructure in the June 2019 quarter. Mozal Aluminium saleable production increased by 2% to 67kt, as the smelter continued to test its maximum technical capacity, despite a modest impact to production from load-shedding. South Africa Energy Coal saleable production decreased by 6% to 6.3Mt in the September 2019 quarter following elevated production in the prior quarter, with lower equipment availability at Klipspruit and preparation for the upcoming wet season impacting volumes.

Australia Manganese saleable ore production increased by 21% to 868 kwmt, as higher utilisation rates were achieved in the primary circuit as the impact of heavy rainfall in the prior quarter subsided. Manganese alloy saleable production decreased by 30% to 28kt in the September 2019 quarter as one of the four furnaces was taken offline. South Africa Manganese saleable ore production decreased by 4% to 547kwmt in the September 2019 quarter as planned maintenance shut was completed at high-grade underground Wessels mine. Manganese alloy saleable production decreased by 27% to 16kt.

Cerro Matoso payable nickel production was unchanged at 10.6kt in the quarter as mining rates increased in-line with the plan, resulting in a lower contribution of stockpiled ore feed. Cannington payable zinc equivalent production increased by 1% to 60.5kt in the September 2019 quarter as a higher zinc grade offset the impact of lower silver and lead grades and reduced mill throughput following planned maintenance.

Company’s net cash increased by US$163 Mn to US$527 Mn, following the allocation of a further US$74 Mn to its on-market share buy-back. It bought back an additional 41 Mn shares during the September quarter and has completed US$1.06 Bn of its US$1.25 Bn capital management program, including the purchase of 359 Mn shares at an average price of A$3.10 per share. During the quarter, the company settled an insurance claim for the incident that led to an extended outage of the Klipspruit dragline at South Africa Energy Coal during FY19, receiving US$98 Mn as full and final payment from its insurers during the September’19 quarter.

It received net distributions of US$63 Mn from its manganese equity accounted investments (EAI) in the quarter following the payment of US$115 Mn (100% share) in royalties at Australia Manganese in respect of the prior six months period.

.png)

Company’s Production Summary (Source: Company Reports)

FY19 Key Financial Highlights for the period ended June 30, 2019: Group’s statutory profit after tax decreased by 71% to US$389 Mn in FY19 following the recognition of impairment charges totalling US$504 Mn (US$578 Mn after tax, including de-recognition of deferred tax assets) in relation to its South Africa Energy Coal operation. Underlying earnings decreased by 25% to US$992 Mn, mainly due to lower aluminium and thermal coal prices offset by 3% increase in Group production volumes, and cost reduction initiatives across labour, energy and materials usage.

Net cash balance at the end of FY19 stood at US$504 Mn, with free cash flow from operations, including distributions from its manganese equity accounted investments of US$1.0 Bn.

.png)

FY19 Income Statement (Source: Company Reports)

Recent Updates:

On November 20, 2019, the company informed the market that it has bought back 392,020,512 shares at the value of $1,198,475,492.

On November 18, 2019, Karen Wood, Chairman, South32 Limited, announced the appointment of Guy Lansdown as an additional director (independent non-executive director) to the Board. Mr. Lansdown has leadership experience in mining and capital projects with an emphasis on greenfield developments in the Americas and is expected to join the Board on December 2, 2019 and seeks election by shareholders at next year’s Annual General Meeting. He is a civil engineer with over 35 years’ experience, including as an executive at Newmont Mining Corporation, where he served as Executive Vice President Discovery and Development.

On November 6, 2019, the company announced that it has entered into a binding conditional agreement for the sale of its 91.835% shareholding in South32 SA Coal Holdings Proprietary Limited (SAEC) to a wholly-owned subsidiary of Seriti Resources Holdings Proprietary Limited and two trusts which will acquire and hold equity on behalf of employees and communities. Following the transaction, Seriti Resources will make an up-front cash payment of around 100 Mn South African Rand to acquire South32’s shares in SAEC. The purchase price also includes a deferred consideration component where S32 will receive 49% of the free cash flow generated by SAEC for a period commencing at the date of completion to March 2024, with payment capped at a maximum of 1.5 Bn South African Rand per annum.

On October 10, 2019, the company paid a fully franked dividend of US$139 Mn in respect of the June 2019 half year.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 25.12% of the total shareholding. Schroder Investment Management Ltd. (SIM) and BlackRock Institutional Trust Company, N.A. hold maximum interests in the company at 6.54% and 3.14%, respectively.

.png)

Top 10 Shareholders (Source: Thomson Reuters)

A Quick Look at Key Metrics: Its gross margin FY19 stood at 67.3%, better than the industry median of 41.1%. Its current ratio for FY19 stood at 2.01x, better than the industry median of 1.87x, implying the company’s decent liquidity position. Its debt to equity multiple for FY19 stood at 0.09x, lower than the industry median of 0.13x.

.png)

Key Metrics (Source: Thomson Reuters)

Key Risks: The company is susceptible to certain risks such as actions by governments, political events or tax authorities; global economic uncertainty and liquidity; natural catastrophes; climate change; etc.

What to Expect: As per the release, S32, in its endeavor to partner with companies to fund early stage greenfield exploration opportunities has invested US$3 Mn during the September’19 quarter. It has further directed US$14 Mn towards exploration programs at its existing operations (US$11 Mn capitalised), including US$1 Mn for its EAI (all capitalised) and US$6 Mn at Hermosa (all capitalised) to further increase its knowledge of the Taylor deposit and the greater Hermosa land package.

The company has progressed over pre-feasibility study at its Hermosa project, which is expected to complete by June 2020 half year. Advanced study work at the Eagle Downs Metallurgical Coal project is ahead of schedule for the December 2020 half year, where a final investment decision has to be taken.

In September quarter, exploration drilling at the Southern Areas at GEMCO was commenced following receipt of final regulatory approval. The initial program is designed to infill areas of known mineralisation and to test regional targets.

FY20 production guidance for Worsley Alumina hydrate remains unchanged at 3,965kt with the refinery to benefit from improved calciner availability and the drawdown of excess hydrate stocks over the remainder of the year. FY20 production guidance for Illawarra Metallurgical Coal remains unchanged at 7.0 Mt with longwall moves scheduled during the December 2019 and March 2020 quarters. FY20 production guidance for Brazil Alumina, Australia Manganese ore and South Africa Manganese ore remains unchanged at 1,330kt, 3,560 kwmt and 2,100kwmt, respectively. FY20 production guidance for Cerro Matoso payable nickel remains unchanged at 35.6kt with the operation scheduled to undertake a major furnace refurbishment in the June 2020 quarter. FY20 production guidance for Cannington payable zinc equivalent remains unchanged with silver 11,200koz, lead 104.0kt and zinc 59.0kt.

.png)

S32 FY19 Vs. FY20E Production data (Source: Company Reports)

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price to Cash Flow Multiple Approach

.png)

Price to Cash Flow Multiple Approach (Source: Thomson Reuters), *NTM-Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock price fell by 23.36% in the past six months. Currently, the stock is trading towards its 52-week low of $2.360, proffering an opportunity for share accumulation. Company’s top-line and bottom-line have shown a decent performance over the past five years, with CAGR above 50% each. Its production for September quarter was recorded the highest, ending the period with a net cash position. The company has kept FY20 production guidance unchanged for many of its products. However, with the cooling-off of macro-economic concerns, especially the USA-China trade war, global growth is expected to revive in the coming times, which, in turn, is likely to help the company to improve its margins. Looking at the business prospects over the long-term, we have valued the stock using a relative valuation method, i.e., Price to Cash Flow multiple, and arrived at a target price of lower double-digit growth (in % term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$2.640 per share, down 1.859% on November 20, 2019.

(1).jpg)

S32 Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...