Company Overview - South32 Limited is an Australia-based metals and mining company. The Company operates through segments, which include Worsley Alumina segment has a bauxite mine and alumina refinery in Western Australia; South Africa Aluminum segment has two aluminum smelters at Richards Bay; Mozal Aluminium segment has Aluminum smelter in Mozambique; Brazil Aluminium segment has Alumina refinery and aluminum smelter in Brazil; South Africa Energy Coal segment has energy coal mines and processing operations in South Africa; Illawarra Metallurgical Coal segment has metallurgical coal mines in southern New South Wales; Australia Manganese segment, a producer of manganese ore in the Northern Territory and manganese alloys in Tasmania; South Africa Manganese segment is a producer of manganese ore and alloy in South Africa; Cerro Matoso segment has laterite ferronickel mining and smelting complex in northern Colombia, and Cannington segment is a silver, lead and zinc mine located in northwest Queensland.

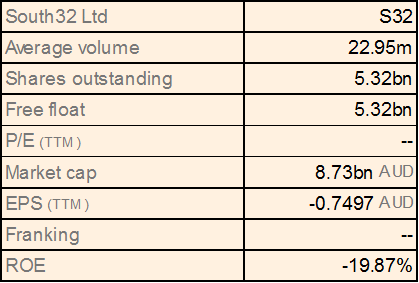

S32 Details

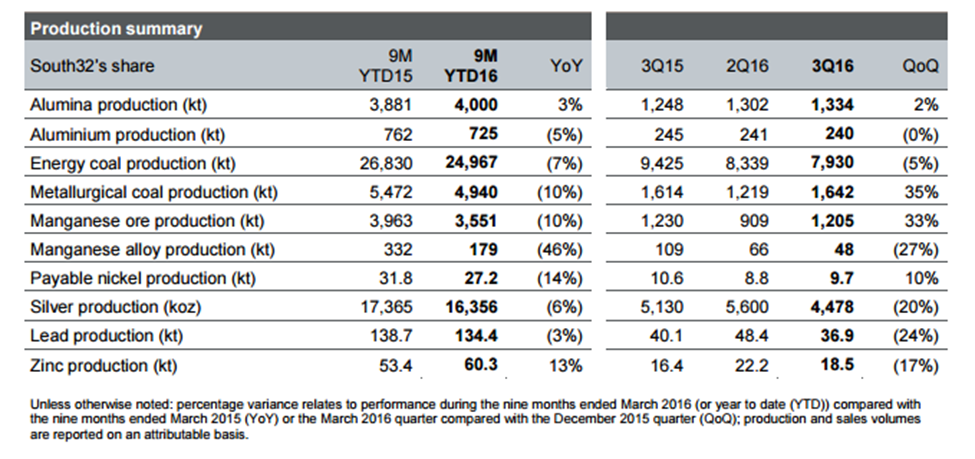

Ongoing cost control: After demerging with BHP Billiton, South32 Ltd.’s (ASX: S32) focus on its core assets coupled with its efforts of controlling costs have been generating results. The group intends to cut controllable costs by US$300 million in FY16 and finished restructuring at Worsley Alumina, South Africa Manganese and the Australia Manganese mining operations. S32 restructuring efforts at Cerro Matoso and Illawarra Metallurgical Coal are forecasted to be finished by the June 2016 quarter. South32 even controlled production in some of its projects to offset the impact of commodity prices pressure. Accordingly, the group’s South Africa Aluminum saleable production was maintained at 525kt for nine months ended on March 2016 and at 173 kt for the three months ended in March 2016. S32 even stopped production in 22 pots during September 2015 at the South Africa Aluminum project to boost its cash flow. The group’s South Africa Energy Coal saleable production fell by 7% (or 1.7Mt) to 24.1Mt during the nine months period as the group closed opencast mine at Khutala, and cut in contractor activity at the Wolvekrans Middelburg Complex as a part of its enhancing efficiency efforts.

Improving Aluminum Production: As per the production highlights for the group, Worsley Alumina saleable production rose by 4% (or 111kt) to 3.0Mt during the nine months ended on March 2016 driven by better calciner availability which led more 5% production in the March 2016 quarter. Solid hydrate production also contributed to the performance as the input circuit exceeded expanded capacity of 4.6Mtpa (100% basis).

Mozal Aluminum saleable production remained at 200kt for the nine months. As per the Brazil Alumina saleable alumina production highlights, the nine months ended on March production reached 999kt, which was largely unchanged while the quarterly sales rose by 6% due to timing difference as one shipment fell under the March 2016 quarter. Australia Manganese saleable ore production surged 7% (or 151kt) to 2.33Mt for the nine months ended March 2016 driven by the group’s optimize concentrator efforts and drier weather conditions. Hence, the inventories fell to normalized levels.

Production highlights by segment (Source: Company Reports)

Pressure in manganese production: The group’s saleable manganese alloy production fell 10% (or 13kt) to 111kt during the nine months ended on March 2016. Saleable manganese alloy production plunged 37% for the March 2016 quarter as compared to the earlier quarter due to temporary suspension of two of four furnaces on the back of the power shortages in Tasmania. The first of the furnaces were suspended in December 2015 while the second suspension followed in March 2016. The rest of the two furnaces are currently operating at a subdued electricity load while the group expects all of its four furnaces to return to full production by the end of June 2016. Even South Africa Manganese saleable ore production fell by 32% (or 563kt) to 1.22Mt during the nine months ended March 2016 on the back of suspended operations at Wessels and Mamatwan during November 2015 due to tough market conditions. Sales of manganese ore fell by 25% impacted by supply chain inventories. Meanwhile, mining activity resumed at South Africa Manganese.

The Wessels Central Block project worth of US$30M (100% basis) would lead the mining to relocate close to major infrastructure facilities leading to decrease in production costs in the underground mine, ahead of the first ore estimation in October 2016. But, South Africa Manganese saleable alloy production plunged 67% (or 140kt) to 68kt during the nine months period on the back of suspension at three of the four high-carbon ferromanganese furnaces at Metalloys in May 2015. The group reported that its Metalloys would remain to operate only in one out of the four furnaces till market conditions improve.

Solid Zinc production: The group reported a major rise in the average zinc ore grade while recoveries as Cannington led to a 13% surge in the zinc production to 60.3kt during the nine months ended on March 2016, on track with the mine plan.

On the other hand, the Cerro Matoso payable nickel production fell 14% (or 4.6kt) to 27.2kt during the nine months period as the average ore grade fell. But, contained nickel production improved given the improving processing rates and maintenance in the December 2015 quarter. Payable silver production fell by 6% (or 1.01Moz) to 16.36Moz.

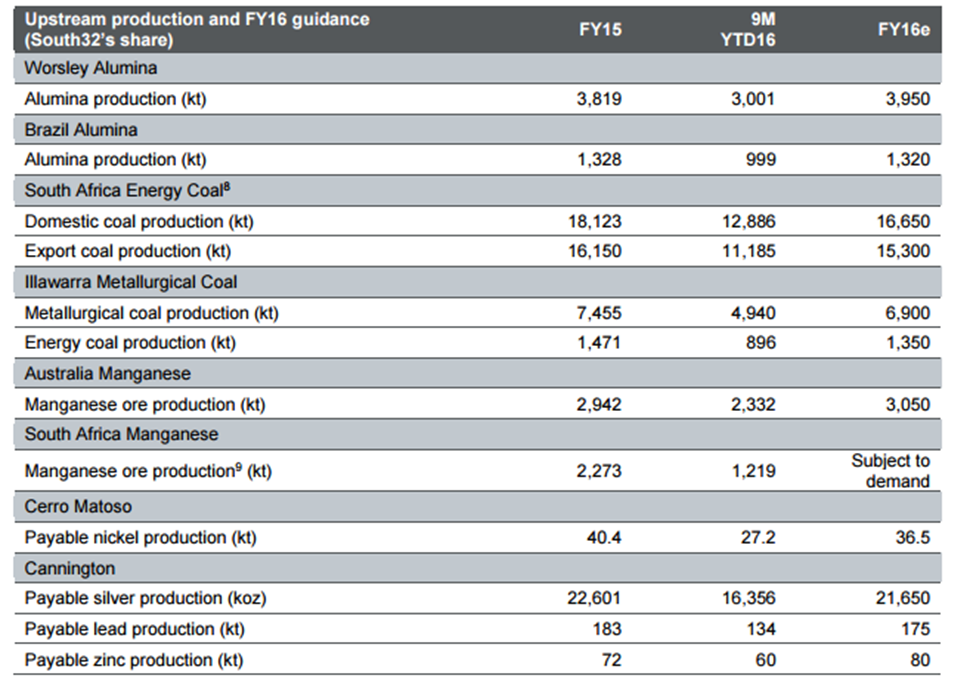

Guidance: S32 estimates that its guidance of depreciation and amortization to reach US$760 million for the full year of 2016 and the capital expenditure to reach over US$550 million during fiscal year of 2016 remains unchanged. Underlying net finance costs are forecasted to be slightly higher than the annualized first half of FY16 run-rate of US$71 million. Meanwhile, the group estimates a saleable alumina production of 3.95Mt and scheduled the next major calciner for the December 2016 quarter. The group expects to maintain its South Africa Aluminum metal production in FY16 as the number of load-shedding events in the March 2016 quarter fell below the expectations.

Brazil alumina production is anticipated to be in similar line against the earlier guidance of 1.32Mt. Nickel production estimates are maintained at 36.5kt while Australia Manganese saleable ore production is forecasted to be at 3.05Mt due to higher strip ratio on the back of planned maintenance effect on June 2016 quarter performance. S32 is also planning mill outages at Cannington during May and August 2016. Still, the group maintained its FY16 production guidance of payable silver at 21.65Moz, payable lead at 175kt and payable zinc at 80kt. South Africa Energy Coal saleable production is estimated to remain at 31.95Mt with 16.65Mt from domestic and 15.30Mt from export.

Guidance by segment (Source: Company Reports)

On the other side, the group initially cut its Aluminum production from Brazil Alumina during July 2013 and reported the suspension of all smelting activity in March 2015.

Moreover, the group even has forward sold power till the end of CY17 and stopped the contract with Eletronorte. Accordingly, S32 reported that they would incur a minimal provision in its June 2016 performance which would show cash outflow related with this contract across the rest of the eighteen month period. Unhedged power sales, inclusive of this provision, are forecasted to deliver over BRL235M to Underlying EBIT for fiscal year of 2016.

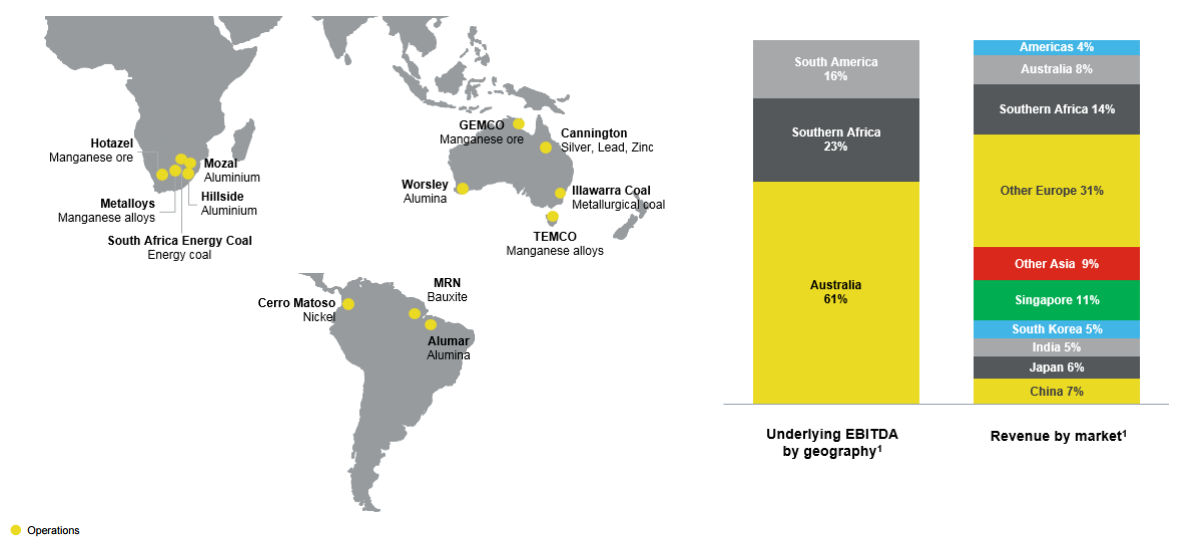

Spread of Operations (Source: Company Reports)

Stock Performance: The shares of S32 rallied over 76.84% (as of May 03, 2016) in the last three months driven by the recovering commodity prices coupled with the group’s efficiency efforts contribution. S32 is also strengthening its capital position and accordingly cut over US$134 million in net debt during the March quarter even though they incurred a US$30 million foreign exchange rate which led to an increase to US$621 million of finance lease liabilities as of March 2016 as compared to the US$595 million during December 2015. S32 also witnessed one-off redundancy and restructuring payments of over US$23 million. Still the group has a strong capital position of US$18 million as of March 2016. Meanwhile, the continuation of longwall mining at Dendrobium and finishing of the Appin Area 9 project led to a 35% rise in metallurgical coal production for the March 2016 quarter. The group’s Appin Area 9 project was also finished at 33% lower than the budget estimates and on track with the estimated schedule.

The Premium Concentrate Ore (PC02) project which is intended to boost GEMCO production capacity by 500ktpa to 5.3Mtpa (100% basis) is also 98% finished and is estimated to start by the June 2016 quarter, contributing to the group’s performance in the coming periods. We believe S32 would continue to rally in the coming months and reiterate our “BUY” recommendation at the current price of $1.54

S32 Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...