Company Overview - South32 Limited is an Australia-based metals and mining company. The Company operates through segments, which include Worsley Alumina segment has a bauxite mine and alumina refinery in Western Australia; South Africa Aluminum segment has two aluminum smelters at Richards Bay; Mozal Aluminium segment has Aluminum smelter in Mozambique; Brazil Aluminium segment has Alumina refinery and aluminum smelter in Brazil; South Africa Energy Coal segment has energy coal mines and processing operations in South Africa; Illawarra Metallurgical Coal segment has metallurgical coal mines in southern New South Wales; Australia Manganese segment, a producer of manganese ore in the Northern Territory and manganese alloys in Tasmania; South Africa Manganese segment is a producer of manganese ore and alloy in South Africa; Cerro Matoso segment has laterite ferronickel mining and smelting complex in northern Colombia, and Cannington segment is a silver, lead and zinc mine located in northwest Queensland.

.png)

S32 Details

Planning to heavily control costs at South Africa Manganese: South32 Ltd (ASX: S32) recently reported that they would be controlling cash costs for several operations at South Africa Manganese. S32 intends to further decrease the manganese ore production as well as cut Rand denominated mine gate costs. The group had already suspended the mining activity at the Hotazel Manganese Mines during November 2015 leading to a decline in manganese ore production by 700kt. But, S32 would restart its operations at South Africa Manganese at a lower rate and better flexibility. The Hotazel mines would improve to a saleable production rate of 2.9Mtpa (100% basis), leading to over 900ktpa or 23% of saleable production out of the market in the near future. At South Africa Manganese operations, over 620 employees would be decreased across the joint venture while second phase of the Central Block development project at Wessels is speeding up. Moreover, the saleable production at the Wessels mine is expected to be decreased by over 36% to 740ktpa (100% basis). Saleable production at Mamatwan is also expected to decline by over 18% to 2.2Mtpa (100% basis) given the optimization of the mining and processing. Only one out of four furnaces at the Metalloys smelter is estimated to deliver continuing operations as it is generating a free cash flow. Meanwhile, the group’s efforts to deliver optimized mine plans, lay-offs and other restructuring programs would further control its Rand denominated mine gate costs. Consequently, S32 estimates to cut its annual sustaining capital expenditure by over 80% to US$7 million (S32’s share) by fiscal year of 2017. However, the group expects to incur the pre-tax restructuring costs (including redundancies) of over US$10 million (S32 share) by fiscal year of 2016.

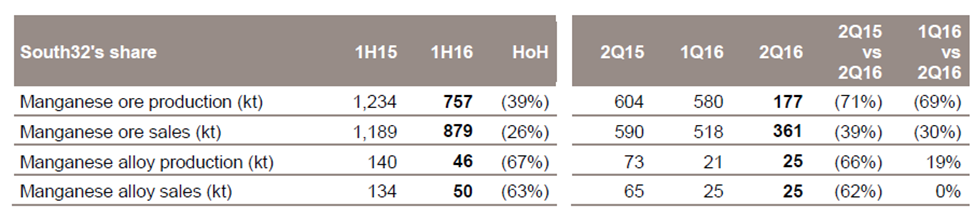

With regards to the South Africa Manganese first half of 2016 performance highlights, saleable ore production fell by 39% to 757kt on the back of deferral of operations at Wessels and Mamatwan during November 2015. Accordingly, South Africa Manganese saleable alloy production dropped 67% to 46kt during the period due to suspension of three of the four high-carbon ferromanganese furnaces at Metalloys in last year May.

Production cut at South Africa Manganese to generate value (Source: Company Reports)

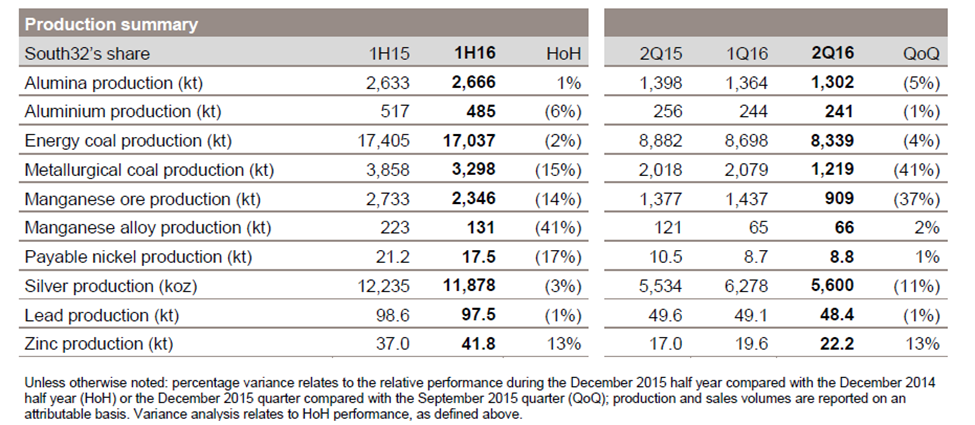

Efforts to deliver benefits via overall restructuring initiatives: South32 demerged with BHP to enhance its focus on its core operations at Illawarra Metallurgical Coal, Cerro Matoso, Worsley Alumina and Australia Manganese. Consequently, the group is making efforts to generate value despite the challenging commodity environment and continuing to optimize costs which would lead to a decrease in employees in the rest of fiscal year of 2016. Moreover, the group’s Worsley Alumina (with S32’s 86% share) reported a saleable production rise of 2% to 1,993kt in first half of 2016 driven by the processed stockpiling of alumina hydrate coupled with operating efficiency gains. South Africa Aluminum saleable production was maintained at 352kt during the period but decreased by 2% on a quarterly basis as the group stopped production in 22 pots in September 2015 for enhancing its cash flow. Mozal Aluminum saleable production was also maintained at 133kt during the six months ended on December 2015, while production slightly rose in the December 2015 quarter due to decrease in the load-shedding events. South32 estimates to maintain Aluminum production in fiscal year of 2016 at par with FY15. Brazil Alumina saleable alumina production was sustained at 673kt while the group intends to deliver an FY16 alumina production of 1.32Mt. But Alumina sales fell by 5% due to timing of the shipments wherein one shipment was categorized for the March 2016 quarter. The group was able to deliver a South Africa Energy Coal saleable production of 16.4Mt during the half year ended on December 2015 as the Khutala underground mine and the Wolvekrans Middelburg Complex operational efficiencies have offset the planned closure impact of the opencast mine at Khutala. S32 intends to achieve a saleable production of 31.95Mt of South Africa Energy Coal production in FY16. On the other hand, Illawarra Metallurgical Coal saleable production plunged 17% yoy to 3.96Mt during December 2015 half year impacted by tough geological conditions at the Appin and Dendrobium mines, coupled with a planned longwall move which was finished in December 2015 quarter.

The firm estimates a further two longwall moves in the March 2016 quarter leading to an overall expected decline in saleable coal production by 7% to 8.25Mt (metallurgical coal 6.9Mt, energy coal 1.35Mt). However, Cannington payable silver production slightly dropped by 3% to 11.9Moz during the first half of 2016 as the group maintained the average silver ore grade.

First half of 2016 production highlights (Source: Company Reports)

Focusing on boosting its capital position: South32 is making efforts to optimize its operations for generating cash flow and consequently the group was able to decrease its net debt to US$115 million during first half of 2016 as compared to US$196 million as of September 2015 and US$402 million as of June 2015 even though the current commodity markets are very challenging. The group was also able to enhance its ore grades and recoveries which led to a 13% rise in Cannington zinc production to 41.8kt. Australia Manganese saleable ore production also enhanced by 6% to 1,589kt in the first half of 2016, driven by its ongoing optimized concentrator performance. The group intends to maintain its production guidance for fiscal year of 2016 for almost all upstream operations, except Illawarra Metallurgical Coal production. Appin Area 9 project is almost finished and forecasted to begin by March 2016 quarter. Meanwhile, South 32 has cut 30% of the original budget to US$845 million for the project which withstands Illawarr3.5a Metallurgical Coal production capacity, and is already three months ahead of schedule.

South32 recent corporate review during December 2015 has indicated its ability to deliver over an estimated of US$30 million of annualized savings during fiscal year of 2016. The group expects to incur a capital expenditure of US$700 million for fiscal year of 2016 which accounts an average USD: ZAR exchange rate of 12.42 and an average AUD: USD exchange rate of 0.78.

Stock Performance: The shares of South32 Ltd (ASX: S32) have corrected over 41.46% (as of February 23, 2016) since its listing, on the back of the falling commodity prices impact on its top line coupled with the ongoing tough market conditions. Accordingly, S32 estimates a pre-tax, non-cash charges of around US$1.7B (which is close to US$1.7 billion after-tax) during six months ended on December 2015. On the other hand, the group’s shares recovered over 20.60% (as of February 23, 2016) in the last four weeks on the back of its restructuring efforts at South Africa Manganese projects as well as other optimizing efforts in order to offset the impact from the ongoing commodity turmoil to a certain extent. The recent South Africa Manganese strategic review would enable the group to restructure their manganese ore production to a low level by simultaneously decreasing Rand denominated mine gate costs. Moreover, South32 efforts to improve its underlying earnings in the first half of 2016 would lead to a better fair value to Australia Manganese.

Management also commented that their restructuring initiatives would boost their capital position and subsequently their cash generating capacity. With the stock rallying over 12.15% (as of February 23, 2016) during this year to date, we believe that S32 has the potential to rise further in the coming months. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $1.13

.PNG)

S32 Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...