Company Overview - South32 Limited is an Australia-based metals and mining company. The Company operates through segments, which include Worsley Alumina segment has a bauxite mine and alumina refinery in Western Australia; South Africa Aluminum segment has two aluminum smelters at Richards Bay; Mozal Aluminium segment has Aluminum smelter in Mozambique; Brazil Aluminium segment has Alumina refinery and aluminum smelter in Brazil; South Africa Energy Coal segment has energy coal mines and processing operations in South Africa; Illawarra Metallurgical Coal segment has metallurgical coal mines in southern New South Wales; Australia Manganese segment, a producer of manganese ore in the Northern Territory and manganese alloys in Tasmania; South Africa Manganese segment is a producer of manganese ore and alloy in South Africa; Cerro Matoso segment has laterite ferronickel mining and smelting complex in northern Colombia, and Cannington segment is a silver, lead and zinc mine located in northwest Queensland.

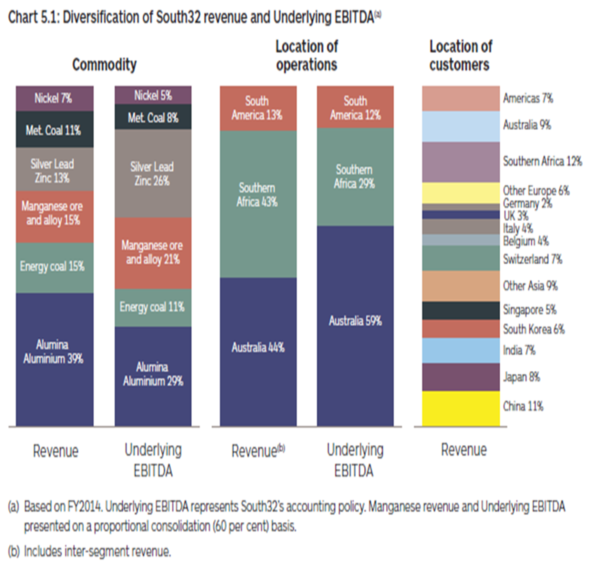

Analysis - South32 Ltd (ASX: S32) produces high quality alumina, aluminum, coal, manganese, nickel, silver, lead and zinc. Alumina aluminum accounted 39% of the firm’s revenues, followed by Energy coal and Manganese ore and alloy which represents 15% of the company’s revenues, as of FY14. South32 has a diversified revenue base with major concentration at Australia, South Africa and South America. Accordingly, the company derives 12%, 9% and 7% of revenues from Southern Africa, Australia and Americas. But the group has been decreasing its dependence from its major regions by expanding its focus to other regions as well, with China, Japan, Switzerland and South Korea contributing 11%, 8%, 7% and 6% of the FY14 revenues respectively.

Revenue and EBITDA by commodity and geography (Source: Company Reports)

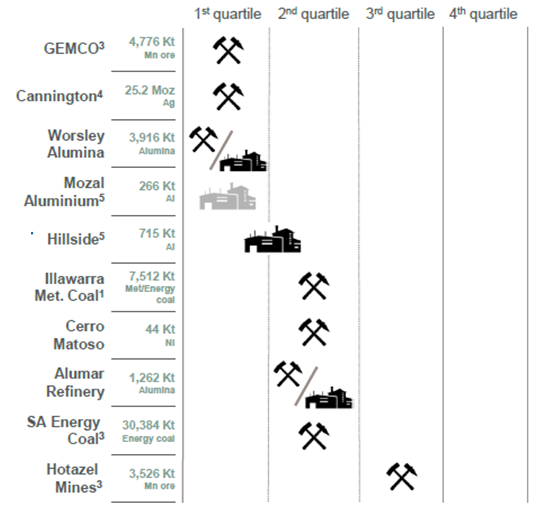

Solid assets with competitive cost curves and long resource Lives

The group’s major assets has competitive cost curves positioned in the first or second quartile of their respective industry cost curves. For instance, GEMCO, Cannington and Worsley Alumina are placed in the first quartile of their respective industry cost curves.

South32 major assets competitive cost curves (Source: Company Reports)

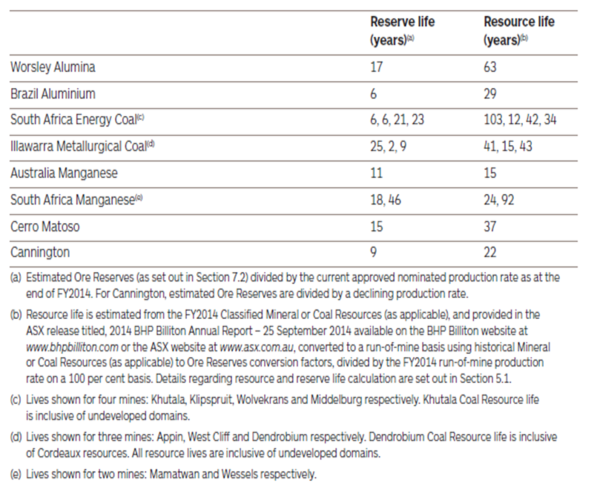

Most of the firm’s key assets also have substantial reserve lives positioning the company to sustain production for long term, with solid resource positions.

South32 resources and reserve life (Source: Company Reports)

The group got over twelve major assets including core as well as joint ventures. Located at Western Australia, Worsley Alumina (S32 has 86% of interest) is an integrated bauxite mining and alumina refining operation and is among the largest and lowest-cost alumina refineries in the world. The project has two multifuel co-generation units contract having 32 years of lease since 2014. Two gas supply agreements will be expired in 2018 and 2023. Meanwhile, Worsley Alumina has coal supply agreements with Griffin Coal and Premier Coal.

Worsley Alumina key financials (Source: Company Reports)

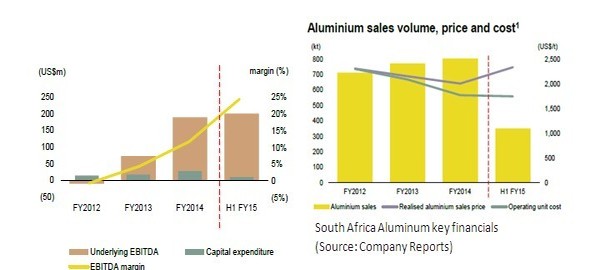

S32 has 100% interest in South Africa Aluminum which is the largest smelter in the southern hemisphere having a capacity of 723 Ktpa aluminum. The group has closed the bayside smelter last year and intends to sellbayside casthouse. The Hillside is positioned across first and second quartile on the aluminum industry cost curves. The project has long term power contracts with Eskom while three long term port facility agreements will be expired on 2019. Moreover, the project has processed over 1,400 ktpa alumina sourced from Worsley Alumina. South Africa Aluminum improved its operating costby 23% in FY2014 to US$1,771/t from US$2,303/t in FY2012.

South Africa Aluminum key financials (Source: Company Reports)

Mozal Aluminum (47.1% of interest) is an Aluminum smelter having a capacity of 566 Ktpa with dedicated port facilities in Mozambique. Majority of the aluminum derived from this project is being exported to Europe through the port of Maputo, Matola. Mozal Aluminum operating costs decreased by 10% to US$1,962/t in FY14 from US$2,189/t in FY12.

.png)

Mozal Aluminum key financials (Source: Company Reports)

South Africa Energy Coal (S32 has 90% interest) is the third major energy coal exporter (~45%) in South Africa and fifth Major domestic supplier of energy coal (~55%) with the output of 30.4 Mt (100% basis). The Richards Bay port has the capacity claim up to 17 Mtpa. The project is among the second quartile on energy coal industry cost curve and has also successfully further improved its operating costs by 20% to US$35/t in FY14 from US$44/t in FY12. The rail haulage agreements with Transnet will expire in 2024. Meanwhile, South 32 is also evaluating the life of mine to extend the projects at Klipspruit (export) and Khutala (domestic) with other brownfield development options under review.

.jpg)

South Africa Energy Coal (Source: Company Reports)

The Illawarra Metallurgical Coal project in which S32 has 100% interest, has three longwall mines near

Wollongong in New South Wales, Australia The projecthas two processing facilities with annual ROM capacity of 12 Mtpa and product capacity of 9 Mtpa. The project has a long term coal supply contract with BlueScope Steel (till 2032). Meanwhile the Appin Area 9 project is expected to start next year. The group was able to decrease the operating costs for the overall project to US$99/t in FY2014 from US$111/t in FY12.

.jpg)

Illawarra Metallurgical Coal key financials (Source: Company Reports)

South32’s high quality assets Australia Manganese (with 60% interest) includes GEMCO open-cut manganese mine and the TEMCO manganese alloy plant. The Manganese ore mine has a capacity of 4.8 Mtpa while the manganese alloy plant has a capacity of 150 Ktpa high carbon ferromanganese and 120 Ktpa silicon manganese (on a 100% basis). Located in the Northern Territory, Australia, GEMCO, is among the world’s low -cost manganese ore producers, with exports contributing over 90% of its ore product through Milner Bay port facilities. The remaining ore is shipped to TEMCO manganese alloy plant in Bell Bay, Tasmania, Australia. Most of the TEMCO’s production is exported to Asia and North America regions. The Australia Manganese project’s operating cost decreased by 7% to US$140/t in FY12 from US$130/t in FY14. The group intends to improve the output of Premium Concentrate Project by 0.5 Mtpa from FY17 on a 100% basis by incurring a capex US$139 million. TEMCO has power sourced contracts under long term agreements (till 2024).

.png)

Australia Manganese (Source: Company Reports)

South Africa Manganese encompasses the Hotazel Mines, the Wessels underground mine (44.4% interest), and the Metalloys plant (60% interest). The Hotazel mines and Metalloys smelter has a ROM capacity of 3.5 Mtpa at Mamatwan open-pit and 1.2 Mtpa at Wessels underground. . The Metalloys plant is among the major manganese alloy producers in the world with major exports going to the United States, Europe and Asia. Meanwhile, the group was able to cut 41% of the operating costs to US$82/t in FY14 from US$139/t in FY12. South Africa Manganese won contract for Transnet rail capacity for the next five years and is also enhancing the Wessels underground crushing capacity to 1.5 Mtpa (on a 100% basis). Moreover, the Coega Port Transnet expansion is expected to deliver higher ore volumes from FY19.

.PNG)

South Africa Manganese key financials (Source: Company Reports)

Located in northwest Queensland, Australia, Cannington (100% interest) is a silver, lead and zinc underground mine and concentrator operation having a nominal processing capacity of over 3.2 Mtpa. The operating costs decreased 8% to US$193/t in FY14 from US$209/t in FY12. However, Cannington’s gas supply agreements will be expired by the end of the year, and therefore South32 is negotiating the potential options.

.png)

Cannington location and cost split (Source: Company Reports)

Balance Sheet highlights

South32 has a net debt of US$674 million after the demerger with BHP Billiton and has a committed credit facility of US$1.5 billion from banks. The company managed to get a stable outlook from Moody’s investor service, and assigned a Baa 1 issuer rating as well as a short term issuer rating of P-2 to south32. The group has improved its Net operating cash flows (before financing activities and tax and after capital expenditure) to US$1.4 billion in FY14 from US$ 0.9 billion in FY12. Meanwhile, South32 might incure costs associated for the life extension of the Klipspruit opencast, Khutala Colliery ((South Africa Energy Coal) as well as to assess alternatives for effectively exploitingCannington mine. South32 has finished investments in Australia Manganese and Worsley Alumina in 2013.

.png)

Cash generation covers capital expenditure (Source: Company Reports)

Outlook

South32 Ltd (ASX: S32) started trading on ASX from May 18

th, after demerging from BHP Billiton Limited (ASX: BHP). After touching a high of $2.45 on May, the shares of South32 have been under pressure and fell over 22.6% till date (from May 21

st to July 21

st). Even BHP Billiton shares corrected over 6.7% during the same period. On the other hand, each eligible BHP Billiton shareholder got a share in South32 during the demerger, and we believe that the recent sell off was mainly due to profit taking by these investors in South32 Ltd. However, as we have mentioned in our earlier report, investors need to bear the risks associated with the commodity price fluctuations, to derive good returns from the stock.

South32 Daily Chart (Source - Thomson Reuters)

South32 Daily Chart (Source - Thomson Reuters)

South32 has demerged from BHP Billiton to enhance focus on its core assets and intends to further decrease costs as well as achieve operating efficiencies. Moreover, rumors have been swirling about the potential takeover of the company by global mining giants, while the current price levels of the stock offers an attractive opportunity for a potential takeover target. Based on the foregoing, we reiterate our “BUY” recommendation on the company at the current price levels of $1.785.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...