Kalkine has a fully transformed New Avatar.

Company Overview: Smartgroup Corporation Ltd is an Australia-based company, which is engaged in outsourced administration, including salary packaging, novated leasing, software, distribution and services, and fleet management services. The Company's segments include Outsourced administration, Vehicle services, and Software, distribution and group services (SDGS). The Outsourced administration provides outsourced salary packaging services, which includes salary packaging administration, novated leasing and share plan administration. The Vehicle services segment is engaged in end-to-end fleet management services. The SDGS segment provides salary packaging software solutions, distribution of vehicle insurances and information technology services. Its employee benefits brands include Smartsalary, Smartleasing, Smartfleet, PBI Solutions, Advantage, Health-e Workforce Solutions, Smartequity, Autopia and Selectus. The Company serves the corporate, health and government sectors.

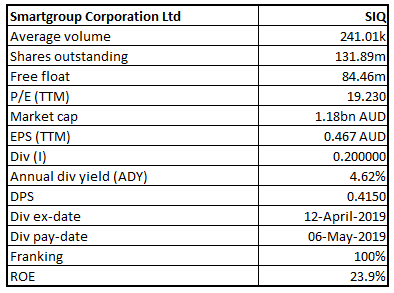

SIQ Details

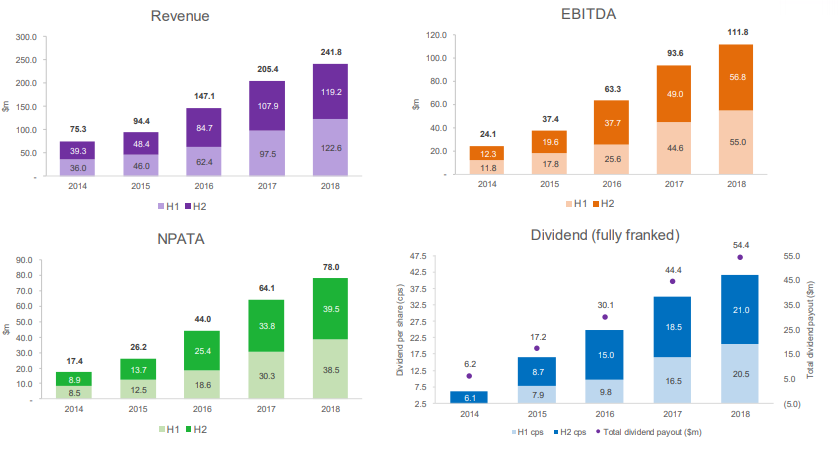

Decent Fundamentals: Smartgroup Corporation Limited (ASX: SIQ) is an ASX-listed company which is engaged in the business of salary packaging administration and fleet management services. The company earlier released its results for CY18 in which it witnessed revenues amounting to $241.8 million which implies an increase of 18% in the prior year and its Operating EBITDA stood at $111.8 million, reflecting an increase of 19% on a YoY basis. The company added that it achieved another year of growth and improved financial results, which was attained via innovation, customer service and ongoing integration of the acquisitions done by it in the past. As a result of decent financial footing, the company made an announcement about a fully franked final dividend amounting to 21 cents per share, which brings full-year dividends for the year to 41.5 cents per share. The company added that, during the year, number of Smartgroup salary packaging customers witnessed a rise of 6% to around 343,000, as well as the number of novated leases under management rose by 4% to more than 65,000. The company also concentrated on integrating the businesses that it has acquired in order to embed a collective corporate culture as well as leverage the benefits of diversity and skills. Additionally, it was stated that the integration of Smartfleet and Fleet West IT systems had been wrapped up and the company has largely transitioned the IT infrastructure and hosting services for the acquired businesses to its environment. The company is also possessing a respectable position with respect to its margins and, thus, it looks like that SIQ has a decent fundamental position. The company happens to be conservatively geared and is having net debt amounting to $14.6 million as at 31 December 2018 which reflects a net debt / EBITDA of around 0.1x. It can be said that the company’s decent fundamental position together with its robust balance sheet might help the company is witnessing growth over the long-term. Additionally, these factors can also help in delivering respectable returns to the shareholders.

There are expectations that strong balance sheet position, decent revenue-generation, and operational capabilities as well as respectable liquidity position can act as potential tailwinds for long-term growth. Also, the company’s annual dividend yield might attract the attention of market players. Based on the foregoing, we have valued the stock using a relative valuation method, EV/EBITDA multiple and five-year average P/E market multiples of 15.56x for CY20E with consensus EPS of $0.67 and have arrived at target price in the ambit of $9.89 to $10.43 (high single-digit to low double-digit growth (in %)). At CMP of $9.04, the stock of the company is trading at P/E multiple 13.49x of CY20E EPS.

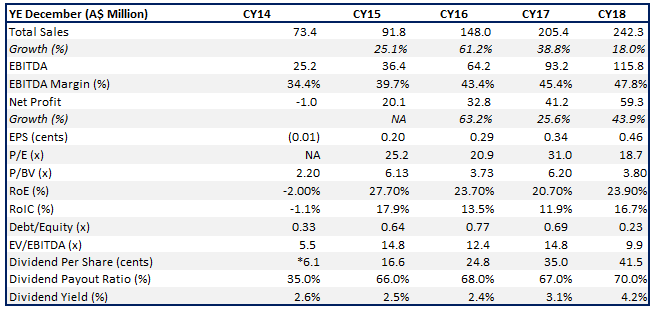

Key Metrics (Source: Company Reports) NA- Not Available, *Represents dividend declared only for H2 2014

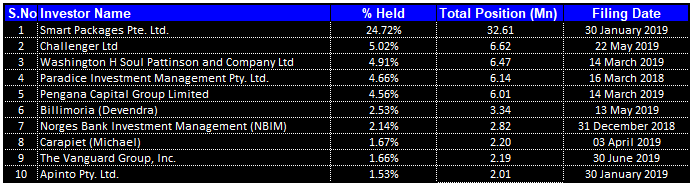

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders:

Top 10 Shareholders (Source: Thomson Reuters)

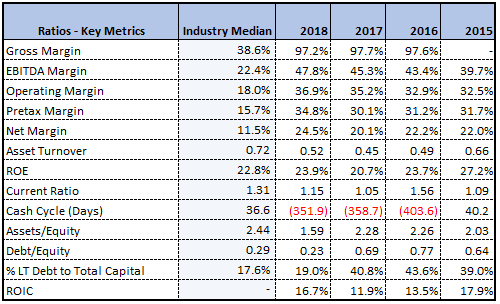

Decent Margins Position as Compared to Broader Industry Median: Smartgroup Corporation Limited is having a respectable position in terms of its key margins as its gross margin stood at 97.2% in CY18 which is comfortably higher than the industry median of 38.6%. Additionally, the company’s net margin stood at 24.5% in CY18, higher than industry median figure of 11.5% and, thus, it looks like that the company’s capability to convert its top-line into bottom-line has improved. Similarly, the company is generating good returns for its shareholders, which is visible from its ROE of 23.9% reported above the industry median of 22.8% in CY18. The company also has respectable liquidity level which is evident from its current ratio of 1.15x, reflecting an improvement of 9.4% on a YoY basis and it looks like that the company would be able to meet its short-term obligations. Also, it can be said that the company might be able to make deployments towards strategic business activities which could act as a potential long-term growth catalyst.

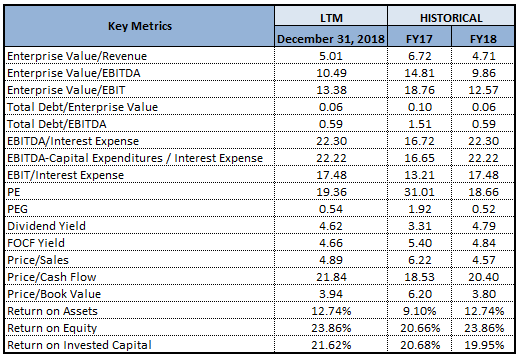

Key Metrics (Source: Thomson Reuters)

A Look at Recent Updates: EML Payments Limited has made an announcement that it has inked an 8-year agreement with the Smartgroup Corporation Limited to be their provider of the branded general-purpose reloadable card programs for the payout of salary packaging benefits. Since2017, EML has been working with Smartgroup and is managing around 50,000 benefit accounts. Recently, the company stated that as part of Selectus Pty Ltd acquisition in 2016, SIQ issued the shares as partial purchase consideration. The shares were subject to voluntary escrow. Further, the group announced that the remainder of shares issued to Selectus vendors will be released from voluntary escrow upon the release of its 1H CY19 results on August 16, 2019.

Focus on Deleveraging Balance Sheet: It looks like that the company has been deleveraging its balance sheet as evident from its Debt/Equity ratio of 0.23x in CY18, reflecting a fall of 65.9% on a YoY basis. Also, the company’s long-term debt as a percentage of total capital stood at 19% in CY18, which implies a fall of 21.8% on a YoY basis. The reduction of debt exposure might further stabilise the balance sheet and can improve its position to meet long-term growth prospects. The lower debt exposure reduces the company’s commitments and, as a result, it can deploy their funds towards other growth areas. The company has witnessed a decent performance in CY18 as it witnessed respectable growth in its key metrics, which strengthens the confidence in the company’s core operational capabilities. The following picture provides a brief overview of the same:

Overview of CY 2018 Performance (Source: Company Reports)

The company’s return on invested capital (or ROIC) stood at 16.7% in CY18, which implies a rise of 4.8% on a YoY basis, which might attract the attention of the market players.

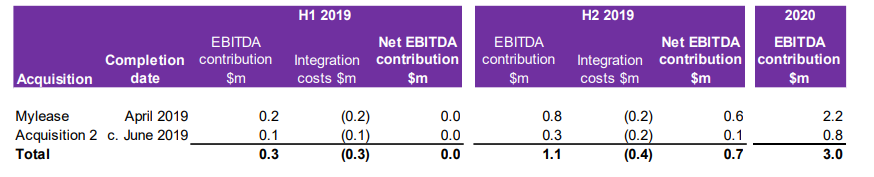

Acquisitions Might Support Long-term Growth: Smartgroup Corporation Limited has acquired novated leasing assets of Mylease from iNovation Pty Ltd which involved the consideration amounting to $6.9 million in cash, including $1.0 Mn in escrow. The company executed share purchase agreement with the vendors of the second acquisition on May 8, 2019. It was also stated that the vendors have requested that the identity of acquired company should not be made public till the client and employee communications occur.

Information About Acquisitions (Source: Company Reports)

With respect to Acquisition 2, SIQ acquired 100% of the salary packaging and novated leasing business for the consideration amounting to $2.2 million in cash, including $0.7 Mn retained in escrow.

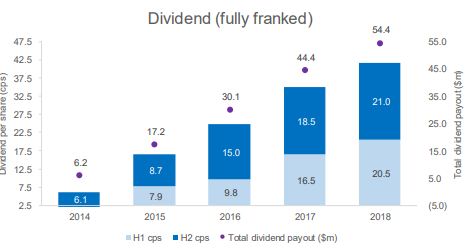

Increase in Dividends Reflects Sound Balance Sheet: Smartgroup Corporation Limited has made an announcement about the final fully franked dividend amounting to 21 cps which resulted in the full year dividends to 41.5 cps for CY18 reflecting an increase of 19% on a YoY basis. Additionally, on May 6, 2019, the company has also paid a fully franked special dividend amounting to 20.0 cps. The following picture provides a broader overview of the company’s dividends per share:

Dividends Per Share Declared (Fully Franked) (Source: Company Reports)

The annual dividend yield of the company is about 3.0% on a five-year average basis (CY14-18). At CMP of $9.04, the company is having an annual dividend yield of 4.62%, which is slightly higher than the broader industry median of 4%, which could attract the attention of the dividend-seeking investors.

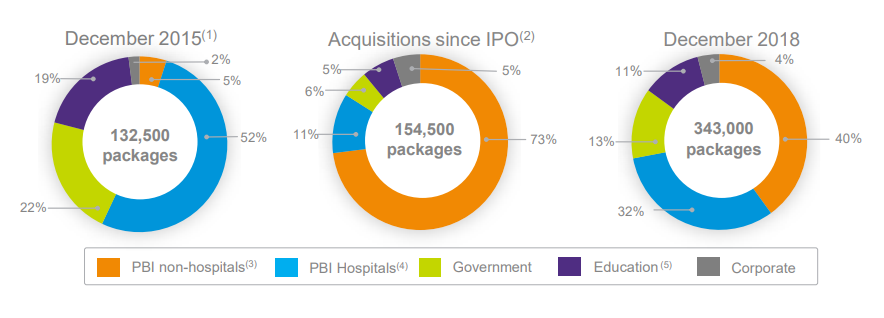

What to Expect from SIQ Moving Forward: The company’s key personnel have stated that, in 2018, SIQ led the industry when it comes to innovation and delivering exceptional customer service. The company added that innovation and customer experience happen to be a key priority for business and digital innovation is vital component of the strategy. It was stated that the company would continue to consolidate infrastructure. The company has been aiming to make each and every experience as easy as possible for the customers and clients. Considering the expanded client base as well as range of services it provides, SIQ is well-positioned to help the clients to reduce administration and the cost of doing business and to improve the financial well-being of their employees. The following picture provides a broader overview of the company’s client base:

Client Base (Source: Company Reports)

Key Valuation Metrics (Source: Thomson Reuters)

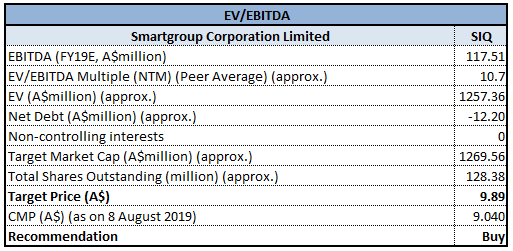

Valuation Methodology: EV/EBITDA Multiple Approach:

EV/EBITDA Multiple Approach (Source: Thomson Reuters), NTM: Next Twelve Months

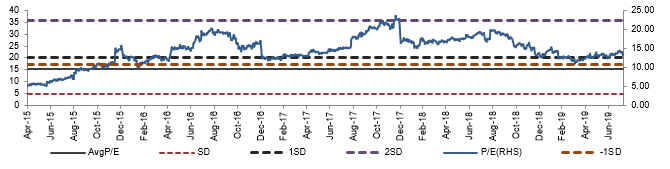

Historical P/E Band (Source: Company Reports, Thomson Reuters)

Stock Recommendation: In the span of previous three months, the stock of Smartgroup Corporation Limited has delivered the return of 5.03% while, on the YTD basis, the stock’s return stood at 4.07% which can be considered at respectable levels. The company has a diversified client base, which might act as a primary growth catalyst and that could further improve the company’s financial position. Smartgroup Corporation Limited has witnessed improvement throughout all the key financial and operational metrics.

The company has witnessed a CAGR growth of 34.79% in the span of previous CY14-18, which reflects that the company has sound capabilities to garner revenues. Also, the company is having decent operational capabilities and is evident from its CAGR growth of 48.78% between CY14-18. It can be said that the company’s operational capabilities together with its revenue-generation capabilities could support long-term growth. The company’s base of cash and short-term investments have witnessed an increase from $27.8 million in CY14 to $39.2 million in CY18, which could help it in further improving its operations. Considering the strong balance sheet, paying dividend consistently, and decent financial metrics, we have valued the stock using a Relative valuation method, EV/EBITDA multiple and five-year average P/E market multiples of 15.56x for CY20E with consensus EPS of $0.67 and have arrived at target price in the ambit of $9.89 to $10.43 (high single-digit to low double-digit growth (in %)). Currently, the stock price is trading below the average of 52-week high and low price of $13.017 and $7.079, respectively, indicating a decent opportunity for accumulation. Hence, in view of aforesaid facts coupled with decent outlook and current trading levels, we give a “Buy” recommendation on the stock at the current market price of A$9.040 per share (up 0.668% on 8 August 2019).

.png)

SIQ Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...