Kalkine has a fully transformed New Avatar.

Company overview - Smart Parking Limited is engaged in the design, development and management of parking technology. The Company operates through the segments, including technology, which consists of car parking technology products sold globally, and parking management, which operates in the United Kingdom and consists of the provision of car parking management services on behalf of third party car park owners and on sites leased by the Company and managed its own behalf. Its SmartApp is a mobile application, which enables drivers to locate vacant parking spaces. Its SmartEye is a sensor technology that gathers and transmits information for management, payment and compliance monitoring. It offers radio-frequency identification (RFID) solutions for payment, enforcement and management, including parking permits. Its SmartRep is a parking management software for both daily administration and long term planning. It offers SmartGuide, which identifies special status parking areas.

.PNG)

SPZ Details

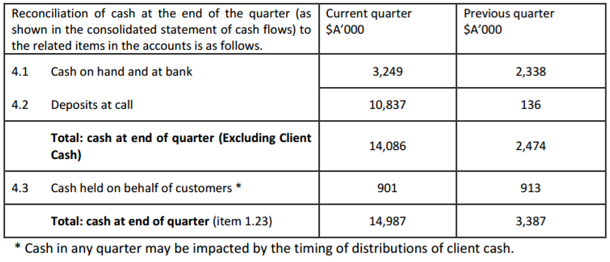

Strengthening balance sheet: Smart Parking Ltd (ASX: SPZ) improved their operating cash flows by $0.9 million to $0.3 million as of December 2016 quarter as compared to the earlier quarter. The deployment of technology solutions in the UK coupled with the finishing of technology projects drove the cash. Meanwhile, the group’s Management Services Division incurred $0.1 million of capital expenditure during the quarter. They expect the operating cash flow in the UK Management Services division would continue to enhance given the ongoing deployment of technology solutions across new sites. Moreover, better operating margins would also drive the division’s cash flow. Smart Parking cash flow from financing activities comprised receipts of $11.4 million (net of costs) from an accelerated non-renounceable pro-rata entitlement offer and a share placement. The group recently finished their fully underwritten 1 for 7 accelerated pro-rata non-renounceable entitlement offer (Entitlement Offer). With this offer, the group targeted to raise $8.4 million via the overall Entitlement Offer. From the Retail Entitlement Offer, the group raised over A$3.6 million at an issue price of A$0.20 per share, leading to 18,307,495 new shares being issued. Accordingly, eligible retail shareholders subscribed for 13,617,267 new shares leading to proceeds of about A$2.7 million under their pro-rata entitlements (representing 74% of new shares offered under the Retail Entitlement Offer). However, there was a shortfall of 4,690,228 shares (Shortfall Shares) between the number of shares subscribed for by eligible retail shareholders on a pro rata basis and the number of shares offered under the Retail Entitlement Offer. As a result, the group allocated these Shortfall Shares as per guidelines. As a result, the group now has cash on hand (excluding client funds) of $14.1 million as of December 2016 end, which is an increase of $11.6 million.

Reconciliation of Cash (Source: Company Reports)

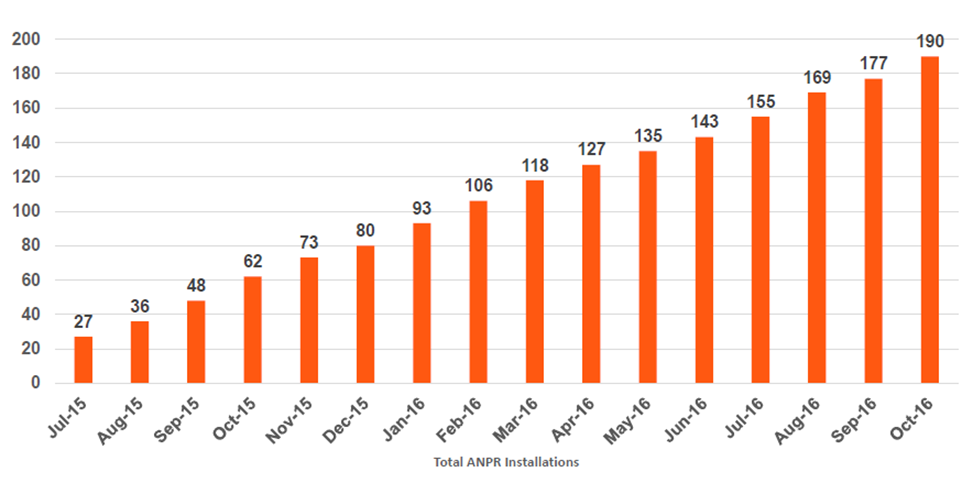

Ongoing contract wins: The group continued to win new contracts and announced for a key contract to be awarded to the group to supply, install and maintain a city-wide deployment of in excess of 3,000 parking bay sensors, ANPR (Automatic number plate recognition) technology and smartphone application to the City of Cardiff Council. The group’s management Services division delivered a solid performance for fiscal year of 2016 driven by the major contract wins during the year. The division won Lidl UK contract to manage more than 30 sites and Matalan UK contract for managing more than 88 sites. New UK sites were added every month leading to a better market share, wherein the group now operates at more than 120,000 car parking spaces in the United Kingdom. As a result, the division’s FY16 revenue rose 33% year on year (yoy) to $28.4 million, and consequently, the EBITDA surged $4.7 million to $5.3 million. Meanwhile, better customer service, deployment of technology on new and existing sites coupled with strong cost control also contributed to this division’s performance. Civil Penalty income surged 119% driven by the segment’s strategy of deploying technology solutions on manually operated car parking sites in the UK. On the other side, Management Services division incurred capital expenditure of $2.4m due to technology rollout but enhance their margins leading to an EBITDA growth by $0.7 million to $5.3 million. The parking management contract with Asda which was terminated on 30 April 2016 contributed a revenue of $9.2m for fiscal year of 2016. However, the cameras are retained and directed to new sites which would enhance return on capital.

Rising ANPR installations in Management services (Source: Company Reports)

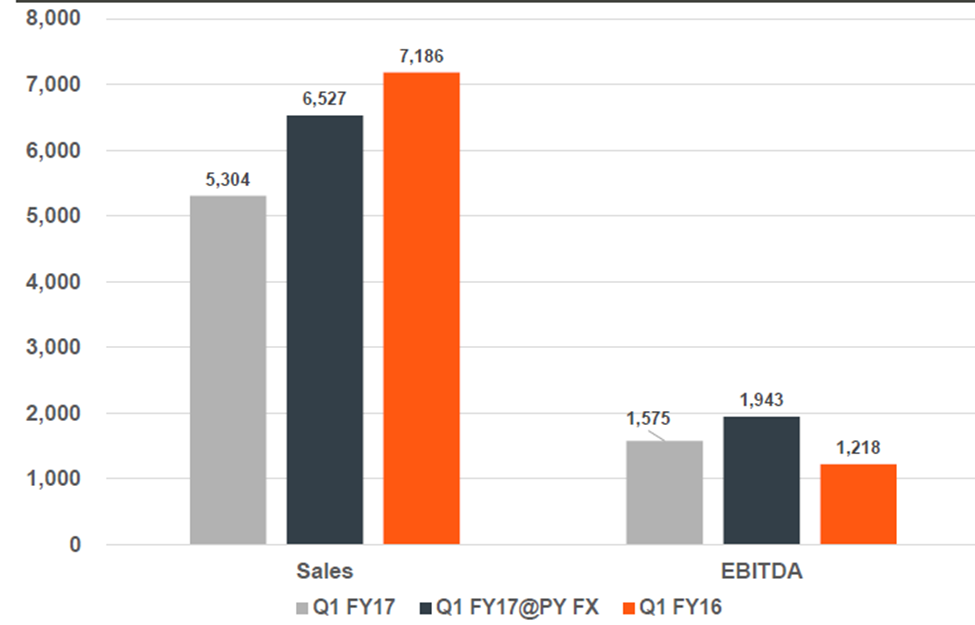

First quarter of FY17 performance on track: Smart Parking continued to drive better margins and EBITDA, and accordingly posted an outstanding EBITDA rise of 719% for the first quarter of FY17 over first quarter of FY16. Consequently, the EBITDA margin surged to 14.7% for the quarter as compared to 1.5% in the prior corresponding period. This strong EBITDA performance is a respite as the top line continued to be under pressure wherein the first quarter of 2017 revenue fell 15% yoy to $6.5m impacted by the Asda contract loss as well as foreign exchange movements. However, Management Services division’s UK headcount fell to 136 as of first quarter of FY17 as compared to 278 in the prior corresponding quarter. But, the group is offsetting the Asda contract loss, where income was shared, by replacing with better margin businesses like new sites with technology. Moreover, the division’s ANPR Installations rose to 190 as of October 2016 as compared to 62 in October 2015. Management expects the division’s performance to continue for fiscal year of 2017 given the ongoing ANPR site installations. The group installed 47 sites in FY17 while more than 80 sites are in the pipeline for installation. Accordingly, SPZ is enhancing the sales team to continue site roll out. The group is also offering installation at zero cost to the customer. The average CAPEX per site is £15,000 while the average monthly ANPR revenue per site is £6,000. Accordingly, the average EBITDA margin per site per month is 70%. As per the Technology division’s first quarter of 2017 performance, the revenues surged over 91% as compared to the same quarter last year, and subsequently, the EBITDA loss improved by 53% against prior corresponding period (pcp). This division has around $30 million of tenders, quotations and proposals in the pipeline for major markets. The group is also awaiting outcomes across Australia, New Zealand and EMEA for the technology division and continues to focus on Research and Development.

Management services Q1 FY17 performance (Source: Company Reports)

Target market opportunity and industry drivers: Smart Parking is targeting the New Zealand market and especially Whangarei, which is the northernmost city in New Zealand with a population of 56,400. As per a survey in January 2016 conducted by the council, locating available parking was among ratepayers' biggest gripes, however the average occupancy of CBD car parks was just at 61% Monday to Saturday and on-street carparks were at 73% occupancy. As a result, the Whangarei District Council introduced Smart Parking’s SmartCounter technology at five of the city’s underused car parks. Smart Parking sees a lot of opportunity across the world. For instance, Verizon Communications acquired parking video analytics business Sensity for its booming Smart Cities business. Verizon’s ‘Smart Communities’ division lies within the IoT business. Smart parking industry is expected to create several opportunities for cities and enhance the value of global parking operations to more than $43 billion by 2025, based on Research & advisory firm Frost & Sullivan. Moreover, Forrester Research expects the world to have 29 megacities by 2025 as compared to just two megacities in 1950. International Data Corporation expects the global market for IoT solutions to rise to $7.1 trillion by 2020 as compared to $1.9 trillion in 2013.

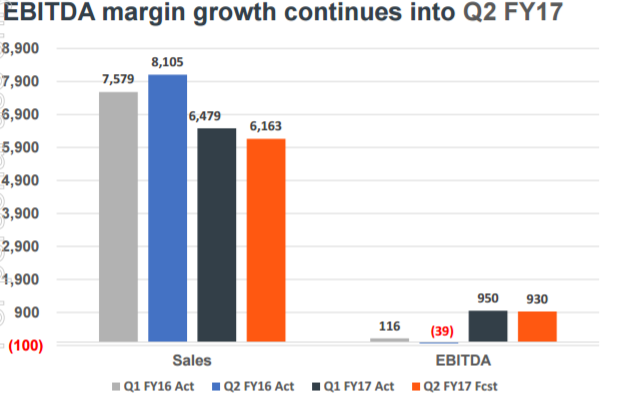

Group Financials (Source: Company Reports)

Stock performance: The group expects their fiscal year of 2017 performance to be driven by the ongoing roll out of their technology in the Management Services division and project wins in the Technology division. Accordingly, second quarter of 2017 Revenue and EBITDA would be on track subject to seasonal quarterly impact. But the first half of FY17 would not have any major technology deals as most of this business would be reflected in the second half. The group is targeting their Management Services to be installed at more than 130 new managed service sites in the UK during FY17. Meanwhile, the shares of Smart Parking rose over 16.75% in the last six months (as at February 13, 2017) and we believe this momentum to continue in the coming months. We give a “Buy” recommendation on the stock at the current price of – $ 0.30

.png)

SPZ Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Please wait processing your request...

Please wait processing your request...