Company Overview - Slater and Gordon is a consumer law firm. The principal activity of the Firm is operation of legal practices in Australia and the United Kingdom. The Firm has two operating segments: Slater & Gordon Australia, which conducts legal services within the geographical area of Australia. This segment also includes investments in the Firms other segment, and borrowings, and capital raising activities to finance investment and operations of the combined Group, and Slater & Gordon United Kingdom, conducts legal services in the United Kingdom. The Firms services include Personal Injury Law (PIL) practice, which provides specialist legal services to people in a range of areas including motor vehicle accidents, workers compensation and civil liability law, and General Law (GL) practice, which is made up of Personal Legal Services (PLS) and Business and Specialized Litigation Services (B&SLS). PLS offers family and relationship law, conveyancing, wills and estate planning and probate practices.

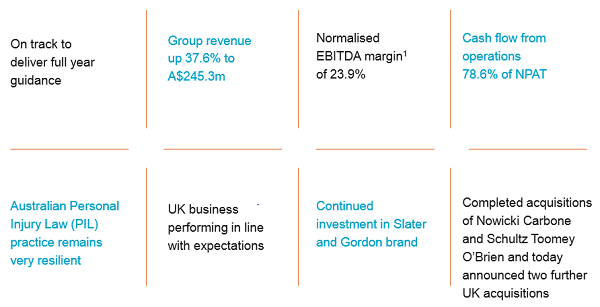

Analysis - Slater and Gordon Limited (SGH) has been in the spotlight given the delivery of a strong operating result for 1HFY15. The result was as per the market’s expectations illustrating 38% revenue growth against prior corresponding period with adjusted NPAT increase of 47% to $35.9 million and EBITDA growth of 43% to $58 million. The margins have been up 78bps to 23.9%. The Company reported that the Australia EBITDA has been up to $31 million while the UK EBITDA has been up to $28.0 million. 26% growth in operating cash flow to $26.5 million signified 79% of NPAT as opposed to the FY15 target of above 70%. The dividend per share has been up 17% to 3.5c against the prior corresponding period.

1HFY15 Highlights (Source – Company Reports)

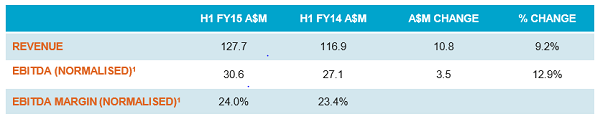

Based on geographic performances, the operating result for Australia was in line with EBITDA growth to $31 million with revenue growth around 9%. Personal Injury law (PI) revenue rose by 5% irrespective of a high level of competition for clients in all markets. Strong performance was noted for VIC with NSW, ACT, SA and WA meeting SGH’s expectations. Competition, regulatory change etc. did pull down QLD to some extent. There was a 37% rise in General Law (GL) revenue to $27 million with the Family Law service line being well set. For the UK operations, EBITDA moved up to $28.0 million and the Company witnessed a humungous 92% revenue growth to $118 million for the region. Thus, there has been a 435bps rise in margins to 23.8%. The PI revenue was found to be $94 million through acquisitions, legislative environment and alliance of claims management companies. GL revenue was reported to be $24 million based on scale up practices and proficiency. Given the splendid 1HFY15 performance, the Company has not gone overboard in upgrading its full-year outlook. This may reflect a secured approach taking into account various efforts in the direction of SGH’s acquisition strategy.

SGH on 9th April 2015, announced for dispatching of its retail offer booklet and other requisite forms for eligible retail shareholders. The retail entitlement offer is closing on 20th April 2015 and is expected to raise about $282 million. Proceeds from the sale of entitlements under the retail shortfall bookbuild are intended to be remitted proportionately to retail holders.

Australian Operations (Source – Company Reports)

The Company quite recently only, announced for the completion of the Institutional Entitlement offer of its fully underwritten 2 for 3 pro rata accelerated renounceable entitlement offer of new SGH ordinary shares at an offer price of $6.37 per new share to raise about $890 million. SGH reported to have raised gross proceeds of about $608 million through the completion of the Institutional Entitlement offer and Institutional Shortfall Bookbuild. Based on the entitlement offer, the first dividend payable with regards to the new shares may be the final dividend for FY15 by SGH. The Company may announce the dividend in August 2015.

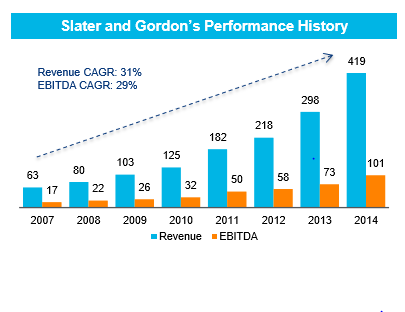

Performance History (Source – Company Reports)

The execution of an agreement to acquire Quindell’s Professional Services Division (PSD) was announced lately by SGH. As per the Company, this effort is related to a return of an upfront consideration of $1,225 million and an earn-out based on performance of PSD’s legacy noise induced hearing loss cases. The raising of $890 in the aforementioned equity will be used to fund the acquisition. This is nonetheless conditional on a majority vote by the shareholders scheduled in April 2015. The transaction is also subject to customary regulatory approvals. This entire opportunity is a transformational opportunity which will enable SGH position as the leading personal injury law group in the UK. Primarily, SGH will be able to penetrate £2.5bn UK personal injury market.

Market Share (Source – Company Reports)

The acquisition opportunity is also expected to deliver value for SGH’s shareholders as it may prove to be EPS accretive (above 30%) based on SGH’s first full year of ownership. The acquisition seems to be a striking one with multiple of c.6.9x pro forma adjusted volume trend core PSD EBITDA. All in all, the SGH’s share of UK PI market is expected to surge from 5% to 12% in one transaction. The Company would also be able to expand existing direct to customer distribution base in the UK. Re-launch of PSD under SGH’s efforts will also yield fruitful results.

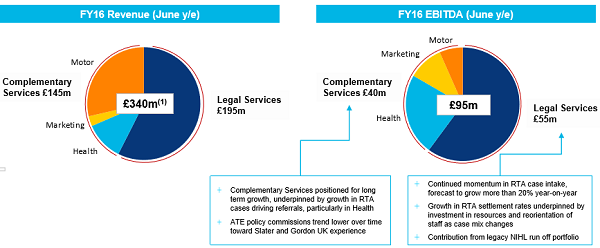

We note that the PSD business is segmented into two divisions under Legal Services that provides specialist personal injury claims services (such as road traffic accident, noise induced hearing loss (NIHL), employers liability and public liability operating) and Complimentary Services relating to Motor Services and Health Services divisions. There is also a Marketing Services unit that supports Legal Services through claims sourcing and aggregation.

FY16 PSD Earnings Guidance (Source – Company Reports)

This step will also allow SGH to be included in the S&P/ASX100 and the Company will be able to maintain the capital structure within 30-40% gearing range with pro-forma net debt/EBITDA of c.1.9x. The Company has also conveyed that in case the acquisition remains unsettled then SGH will return the proceeds from the Entitlement offer to shareholders post an appropriate assessment. The Company expects the financial close to be in May.

Business Locations and PSD Service Lines (Source – Company Reports)

The Company confirmed its FY15 guidance for existing operations with total revenue of $500 million that excludes announced UK acquisitions. The normalised EBITDA margin has been stated to be 23-24% while the cash from operations has been confirmed >70% as percentage of NPAT.

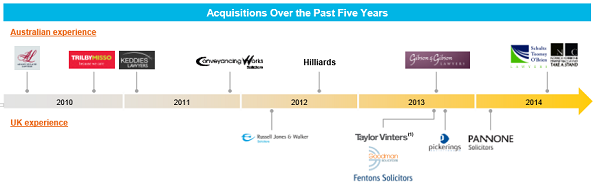

SGH’s Acquisitions (Source – Company Reports)

One point of concern does prevail around the fact that SGH has stepped up for a big acquisition in a business which does not lie under its own competence. But at the same time, we also think that the Company has taken an initiative which can help the Company to leapfrog into a highly EPS accretive business. The acquisition does look to be a positive one. The other recent announcements with regards to acquisitions of Walker Smith Way and Leo Abse & Cohen are potential with an effect of increasing SGH’s UK geographic presence into Wales and North West England.

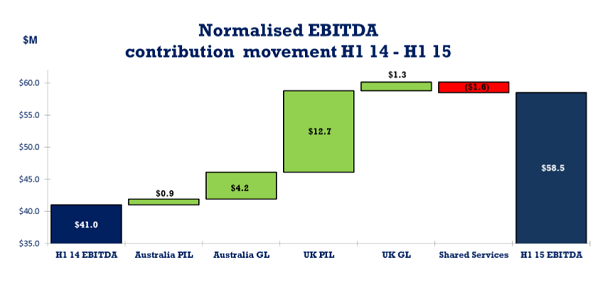

Normalised EBITDA (Source – Company Reports)

Competition and regulatory risks given the consumer law market do prevail but overall the scenario looks interesting. Other factors that need to be taken into account include risks related to M&A pricing and integration, and extended cash conversion cycle along with WIP recoverability of personal injury cases.

SGH Daily Chart (Source - Thomson Reuters)

Overall, SGH will have a strategic focus on acquisitions in FY15. The brand recognition in personal injury law appears to remain strong given various efforts undertaken by the Company. Strong balance sheet with other an efficient management are other key drivers for performance. The Company positions among the top 100 Australian listed companies in terms of market capitalisation post the PSD acquisition.

Based on the foregoing, we put a BUY recommendation for this stock at the current price of $7.47.

Please wait processing your request...

Please wait processing your request...