Kalkine has a fully transformed New Avatar.

Company Overview: Skycity Entertainment Group, also known as simply Skycity, is a gaming and entertainment company based in Auckland, New Zealand. It owns and operates five casino properties in New Zealand and Australia, which include a variety of restaurants and bars, two luxury hotels, convention centres, and Auckland's Sky Tower.

.png)

SKC Details

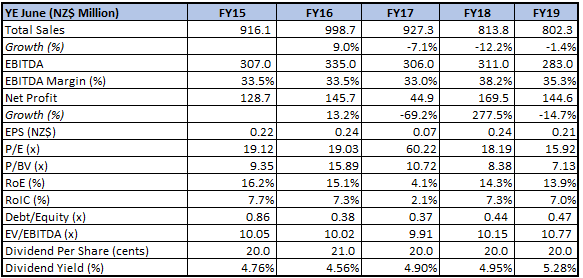

Decent Performance in FY19: SkyCity Entertainment Group Limited (ASX: SKC) happens to be New Zealand’s largest tourism, leisure and entertainment company which has a dual listing on New Zealand and Australian stock exchanges. It operates integrated entertainment complexes in New Zealand (i.e., Auckland, Hamilton and Queenstown) and also in Adelaide, Australia. As on September 19, 2019, the market capitalisation of SkyCity Entertainment Group Limited stood at ~A$2.45 billion. The company has recently released its results for FY19 wherein it witnessed robust performance from local businesses and growth in the international business (IB) turnover. The company has been maintaining ongoing focus towards the efficient capital allocation and stated that the major projects in Auckland and Adelaide are expected to be completed by 2020 end. In FY19, the company’s reported revenues amounted to NZ$822.3 million, which reflects a marginal rise of $6.4 million or 0.8% on a YoY basis. Its normalised revenue (including Gaming GST) stood at NZ$1,118.9 million in FY19, reflecting an increase of 1.6% on a YoY basis. In the recent Macquarie Investment Conference, the company stated that it has an investment grade BBB- credit rating from the S&P and committed to maintaining current dividend policy of 20cps or 80% of normalised NPAT. Also, the company has significant experience when it comes to developing and operating integrated entertainment precincts. Talking about some of the industry trends, the company added that there is a requirement to continually diversify the offering in order to compete and capture the broader customer base and capital investment is needed in order to sustain/grow the business.

Further, it was added that alternative forms of gaming (like online, AR/VR, social/skill-based gaming) and entertainment are becoming popular and there are positive secular growth trends in Asia along with growing (and increasingly mobile) middle-class. The company’s business goals revolve around improving the operating performance, optimising the existing portfolio and grow as well as diversify the business. The company added that, after eliminating Darwin and adjusting for a rise in the effective tax rate, its normalised NPAT was up 7.5% on a pcp basis. With respect to New Zealand properties, EBITDA for combined NZ properties witnessed a rise of 2.5% on pcp basis even though there was more challenging operating environment.

In the Macquarie Investment Conference, the company threw some light on key investment themes which include (1) high quality of the earnings, (2) focus towards leveraging and maximising the existing assets/casino licences, and (3) on-going focus towards the effective capital allocation and improving returns. These factors can also act as tailwinds for the long-term growth. Based on the foregoing, we have valued the stock using a relative valuation method, i.e., Price to Earnings multiple and arrived at a target price upside of single-digit (in percentage term). At CMP of $3.70, the stock of the company is trading at P/E multiple 16.14x of FY20E EPS.

Key Financial Highlights (Company Reports, Thomson Reuters)

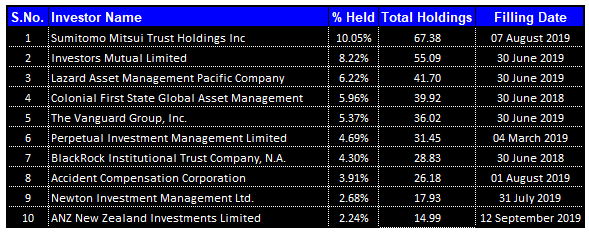

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in SkyCity Entertainment Group Limited:

Top 10 Shareholders (Source: Thomson Reuters)

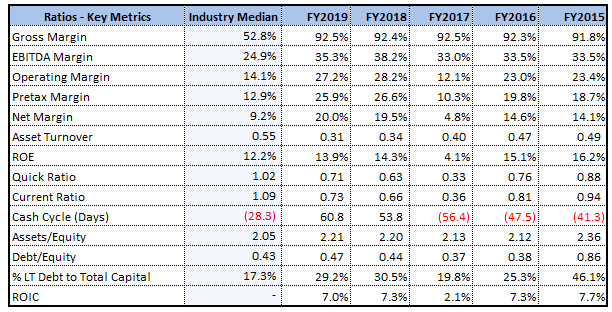

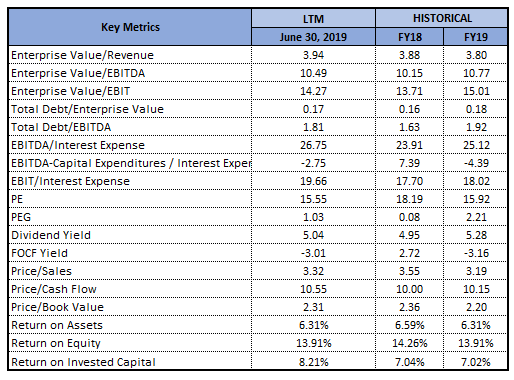

Key Margins Higher Than Broader Industry: The net margin of SkyCity Entertainment Group Limited stood at 20% in FY19, which is comfortably higher than the industry median of 9.2% and, thus, it looks like that SKC is possessing better capabilities to convert its top-line into the bottom-line as compared to the broader industry. The company’s operating and EBITDA margin stood at 27.2% and 35.3%, which are higher than the industry median of 14.1% and 24.9%, respectively reflecting a better fundamental when compared to the broader industry. The company’s RoE stood at 13.9% in FY19, which is higher than the industry median of 12.2% and, thus, it can be said that SKC is providing better returns to its shareholders as compared to the industry. SKC’s current ratio stood at 0.73x reflecting a rise from FY18 figure of 0.66x and, thus, it can be said that the company has decent liquidity levels and can meet its short-term obligations in a better way. Also, decent liquidity levels can support it in making deployments towards strategic business activities which could act as long-term tailwinds. SKC’s percentage long-term debt to total capital stood at 29.2% in FY19, which is lower than FY18 figure of 30.5% and, therefore, it looks like SKC’s exposure towards the long-term debt has been reduced.

Key Metrics (Source: Thomson Reuters)

Announcement of Plans to Offer Online Casino Gaming: SkyCity Entertainment Group Limited recently made an announcement that its Maltese subsidiary company, named SkyCity Malta Limited, will partner with international iGaming company Gaming Innovation Group Inc to provide the New Zealanders with the online casino gaming platform. The proposed ‘skycitycasino’ online gaming site is anticipated to be rolled out in the mid-2019 and would be operated from Malta under a .com URL.

According to the key personnel of SKC, the online casinos are being used by the New Zealand customers and this trend will only continue. The world has been rapidly moving online and the company’s industry is no exception, so they are ensuring that they remain relevant to the changing consumer trends and preferences.

Update Related to On Market Buy Back: The company recently gave a notice under NZX Listing Rule 3.13.1 and it is related to the acquisition of the ordinary shares in SkyCity Entertainment Group Limited under an on-market share buyback programme which was announced on February 13, 2019. The company has acquired 122,386 ordinary shares involving an acquisition price per security amounting to $3.87 (average). It was stated that percentage of the total class of the financial products acquired stood at 0.0183%. The total number of financial products of the class post acquisition (excluding treasury stock) stood at 670,245,556 ordinary shares.

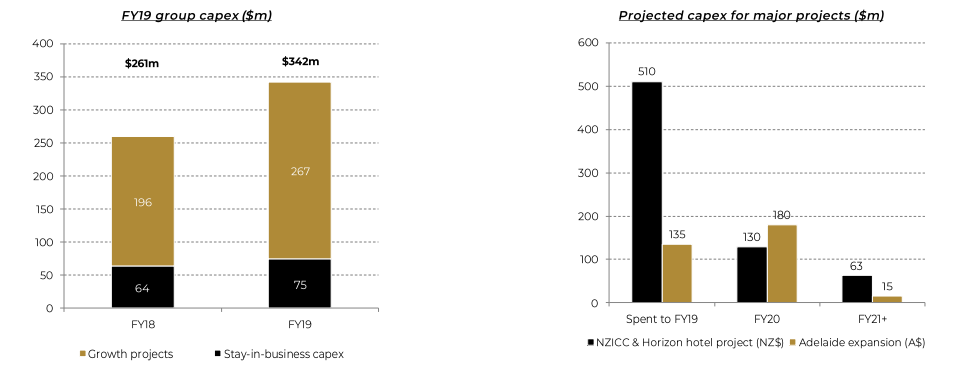

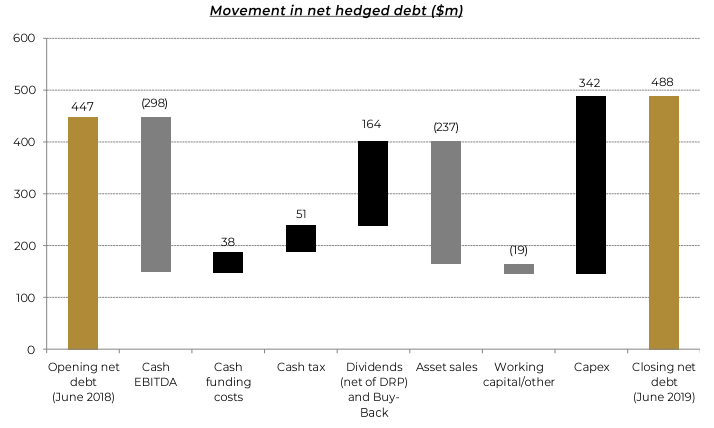

Understanding SKC’s Capital Allocation Framework: SKC is focussed towards the effective capital allocation and its balance sheet is in the robust position to deliver on its medium-term strategic plan, which might help it in gaining traction among the market players. To optimise the capital structure, the company manages the actual and forecast operational cash flows, capex and equity distributions. The following picture provides an idea of capital expenditure:

Capital Expenditure (Source: Company Reports)

Full-Year Dividend In-Line With Existing Policy: The company has declared a fully-imputed final dividend amounting to 10 cps and its full-year dividend stood at 20 cps which happens to be in-line with the existing policy. The company also stated that $39 million or 1.5% of the total shares have been acquired during 2H FY19 as part of the buy-back (involving an average share price of $3.84).

Funding and Capital Management (Source: Company Reports)

The Board has approved an on-market share buy-back programme to purchase up to 5% of its total ordinary shares on issue. It was added that, even assuming that the full buy back is executed, the company would be having sufficient funding headroom to deploy towards master planning opportunities in Hamilton and Queenstown on standalone basis and stay within the acceptable gearing limits. However, the company will need development partner in Auckland in order to make investment feasible and not stretch its balance sheet.

What to Expect from SKC Moving Forward: Considering the structural changes in business, the direct comparability of FY20 earnings to previous corresponding period would be challenging. Even though there is more challenging and uncertain operating environment domestically and internationally, the company is expecting revenue growth throughout the various businesses, partially offset by the increase cost pressures. The company continually monitor the potential for an economic slowdown and believes there is more it can do in order to improve its performance and, hence, expect to achieve some growth in earnings on a like-for-like basis.

The company has a robust platform in order to drive positive medium-term earnings growth and it has a high-quality team focussed towards the delivery of its strategic plan. SKC’s balance sheet is conservatively geared, its existing projects are financed and, while it continues to develop Group master plans, it is yet to commit to anything new that can significantly impact it. The company continues to deploy towards the future and look through cycle to the earnings potential of its business in FY22/FY23 and beyond. SKC stated that, in FY20, there are expectations that it could achieve some growth in group normalised EBITDA as compared to like-for-like FY19 comparative. The corporate costs are anticipated to be around $37 million and net interest expense is expected to be approximately $5 million. However, depreciation and amortisation (D&A) is anticipated to be approximately $90 million and the effective normalised tax rate is expected to be consistent with that of FY19.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: P/E Multiple Approach

(10).png)

P/E Multiple Approach (Source: Thomson Reuters), *1 NZD = 0.93 Australian Dollars as of 09/19/2019

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

(15).png)

Historical Price Band (Source: Thomson Reuters)

Stock Recommendation: The stock of SKC has delivered the return of 1.67% in the span of previous three months while, on a YTD basis, it posted a return of 13%. SKC has recently made an announcement that the sale of long-term concession over Auckland car parks to the Macquarie Principal Finance Group (or MPF) for the consideration amounting to $220 million has been completed. The company has been focusing towards marketing, promotions and events in order to drive visitation at key Auckland property and greater emphasis is being placed on data analytics. The company is focused towards achieving the operating efficiencies wherever possible in order to offset the cost pressures. Based on the foregoing, we have valued the stock using a relative valuation method, i.e., Price to Earnings multiple and arrived at a target price upside of single-digit (in percentage term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$3.700 per share (up 1.37% on 19 September 2019).

SKC Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...