Company Overview - Skilled Group Limited (ASX: SKE), is the largest workforce solutions provider in Australia employing around 50,000 skilled workers per year. The Company extends its services on onshore and offshore total workforce management, labor solutions and project-based workforce solutions; and has over 100 offices across Australia, New Zealand, United Kingdom, Malta and the United Arab Emirates.

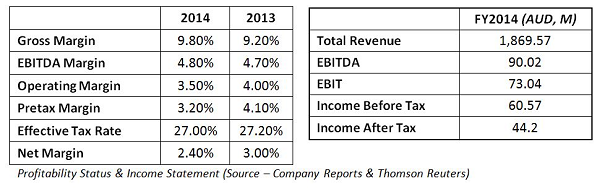

Analysis - SKE’s FY14 results appear to be quite encouraging and in line with expectations with following key highlights - Revenue was $1,873.3 million in 2H14, which is 6.7% higher than that of 1H14 (primarily driven by Engineering & Marine Services); Promising results achieved for acquisitions; Underlying EBITDA margin maintained at 5.1%; cost reduction of about $15 million in FY14 being achieved; Healthy operating cash flow; Increase in total FY14 dividend to 17.0 cps; Increased final dividend of 9.5 cps; and fully franked Gearing remaining conservative at 26.2%. Accordingly, the total dividend declared for FY14 which is 17.0 cps (fully franked), is 1.0 cps up from 16.0 cps in FY13.

Group Performance (Source – Company Reports) [1Includes equity accounted income from joint ventures; 2Refer to page for reconciliation of underlying NPAT to reported NPAT. Underlying NPAT is an unaudited non-IFRS measure;3As per segment reporting; 4Debt/(Debt + Equity)]

Group Performance (Source – Company Reports) [1Includes equity accounted income from joint ventures; 2Refer to page for reconciliation of underlying NPAT to reported NPAT. Underlying NPAT is an unaudited non-IFRS measure;3As per segment reporting; 4Debt/(Debt + Equity)]

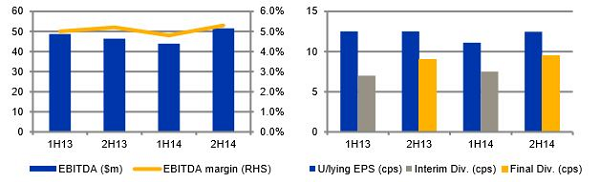

Quarter-wise Financial Data (Source – Company Reports)

Quarter-wise Financial Data (Source – Company Reports)

The overall spike in the performance has been the result of SKE’s strategy to invest in more striking and higher growth sectors while sustaining and benefitting from brand strength in the core business. The Company announced that this along with the bricks of management capability and a strong balance sheet has facilitated in building a strong foundation for SKE.

The sturdy run-rate achieved in the second half is expected to continue into FY15. While grounded with basic values on the safety performance, the Company has witnessed a 14% reduction in AIFR that has added to lowering the cost base.

Segment-wise Performance (Source – Company Reports)

Segment-wise Performance (Source – Company Reports)

An overview of the segment performance for FY14 encourages us to note the following –

Engineering and Marine Services(Brands ATIVO, Thomas & Coffey, SKILLED Offshore and Broadsword Marine Services) – This segment delivered outstanding revenue growth (32% revenue increase and 41% EBITDA increase). Activity levels in ATIVO improved in 2H14. Thomas & Coffey, acquired in February 2014, is also on track. In SKILLED Offshore, a strong performance from the International and New Zealand businesses, and improved activity levels in the Australian business raised the bar. Other catalysts include - Mobilization of the Saipem contract with major work scheduled for FY15. Broadsword Marine Services contributed $16.6 million EBITDA. Also, there is a hefty pipeline of work projects such as mining and infrastructure related projects. However, the only less attractive point was the declining contribution from the OMSA JV.

Workforce Services: The revenue and margin face challenge from unfriendly market conditions due to factors such as weaker employment growth post the Federal budget. Still, SKE has made some progress in order to combat with pricing pressures. The segment will also benefit from recently upgraded ERP (Agresso) and on-going automation and centralization of activities. Further, the segment will be benefiting from supplier consolidation in mining and FMCG market segments.

Technical Professionals: Reduced engineering project activity did come as a hit. Specifically, the Company witnessed a decline in Swan revenue, although some signs of stabilization in contractor numbers by end 2H are on the way. Thus, SKE still aims to sail through based on stable contractor numbers and a probable high-rise in demand for NBN related telecommunication roles in FY15. Other sub-segments such as Training Services and Indigenous employment have been on track.

It is also noted that all the positives offset the cyclical decline in Workforce Services and Technical Professionals.

Coming to the very interesting part here, we note that the Company has made certain strategic decisions like acquisition of Broadsword Marine Services (July 2013) which helped in achieving a rapid growth in Engineering and Marine Services. Other such example is the acquisition of Thomas & Coffey.

SKE’s strategy to invest in systems and processes to leverage scale across the Group has also paid off well – Examples include the ERP (Agresso) upgrade. Moreover, the Company capitalized on growth opportunities with national operations and maintenance services business spread across a scalable platform along with enhanced exposure to segments such as mining. Future profits would also be based on recent contract wins (in iron ore, coal, infrastructure and rail) and renewals in FY14.

EBITDA and Underlying EPS (Source – Company Reports)

EBITDA and Underlying EPS (Source – Company Reports)

Net debt and operating cash flow Net debt increased in view of payments for acquisitions of $86.5 million, additional capital expenditure and initial working capital required to support the Saipem project. Considering SKE’s journey towards a growth upsurge, the debt still looks substantially comfortable to us.

SKE’s Net Debt (Source – Company Reports)

SKE’s Net Debt (Source – Company Reports)

Total Assets, Liabilities and Equity (Source – Company Reports)

Total Assets, Liabilities and Equity (Source – Company Reports)

Of course, a few things that are playing on our minds include the risk from a new and unfamiliar CEO; potential industrial action though various recent strikes have been cancelled for resolution per se; competitive pressures; well-integration of acquisitions; labor demand and so forth. At the moment, these look to be offset by what SKE’ stores as its treasure in terms of the business accomplishments.

As per the Company’s Outlook, the positives of FY14 will penetrate into FY15 to provide a great momentum. It is expected that Saipem project will equalize the issues faced from the OMSA JV. FY15 earnings will be well-supported by Thomas & Coffey and growth in Broadsword. New contract wins and opportunities will be a fuel to the fire of success. The Company anticipates that margin pressure will be turbulent in Workforce Services, however, the activity levels seem to stabilize. Increased NBN activity will strengthen the Telecommunications activity. Health and Training Services activity levels are expected to remain solid into FY15. A further $10m benefit in FY15 is expected owing to the cost reduction program. Working capital will be crowning in mid FY15 in coherence with Saipem project’s progress. SKILLED is well positioned for longer term benefits.

It is also expected that SKE may witness further high earnings than expected when domestic economic conditions improve and demand for labor also recuperates.

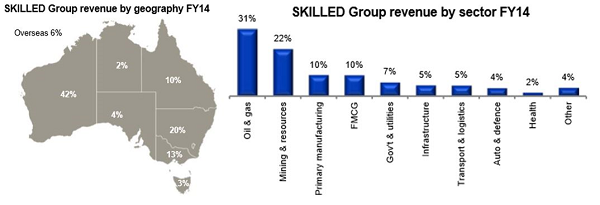

Revenue by Geography and Sector FY14 (Source – Company Reports)

Revenue by Geography and Sector FY14 (Source – Company Reports)

We are embraced by the Company’s efforts and strategy that entails building scale and capability in attractive higher skill, higher margin segments; continually achieving growth and upside potential in Engineering & Marine Services; setting synergies through Thomas Coffey and other acquisitions; expanding international network of offices into Singapore and Houston; reducing cost base remarkably; investing on many systems and processes; driving cultural integration; devising client and staff retention programs; aiming for attractive returns from recent investment in vessels; building a strong balance sheet and cash generation to support dividends and investment in future growth, and many more, which indicate that SKE is well positioned for longer term benefit.

SKE Daily Chart (Source - Company Reports)

SKE Daily Chart (Source - Company Reports)

Accordingly, this market leading brand with its strength in providing world-class solutions stemming into the domains of operators & technical professionals, engineering projects, and marine services & maintenance; coupled with a strong position in key growth sectors including ‘mining & resources’; ‘oil and gas’; ‘infrastructure’; ‘telecommunications’ etc. gain our attention. We thus put a

BUY recommendation on the stock at the current price of $2.22.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...