Company Overview – Skilled group is a provider of labour and workforce services to the public and private sectors. Services it provides include the provision of trades and professional labour, maintenance services, project management, healthcare professionals and offshore marine staffing services. It is Australia’s largest provider of workforce solutions, with a branch network of over 100 local and regional offices across Australia, New Zealand, United Kingdom, Malta and UAE.

Analysis – The company has built up a strong franchise over a number of years to become Australia’s largest provider of workface solutions. As a national operator, its scale gives it some advantage over smaller operators in winning contracts. Nonetheless this competitive advantage is not strong enough to allow the company to generate superior returns. The business has strong cash flow generation and low capital expenditure requirements. However earnings are highly cyclical given its strong leverage to the economic cycle, particularly the mining and energy sectors. The competitive environment is robust and the margins are notoriously low. While the company will benefit from trends by businesses to outsource non-core activities during the recent economic slowdown, demand from outsourced labour declined. Key planks of Skilled’s strategy include building scale in attractive higher skill, higher margin segments and leveraging scale and brand strength in its workforce services business unit, with a focus on customer services, cost efficiency and safety. Steady progress is being made with implementation of the strategy. However earnings are highly leveraged to the economic cycle.

Skilled operates in a highly fragmented industry, subject to intense competition. Skilled’s main business is highly cyclical but the cost base can react quickly to changes in economic conditions given its highly variable cost base components. Skilled offers exposure to outsourced labour markets through its provision of labour hire and staffing services to a range of industries and government agencies. The trend towards greater workforce flexibility creates opportunity for skilled as they draw on a large pool of casual workers. However during the recent economic downturn this trend reversed as employers sought to reduce costs and maintain their direct workforces. Earnings can be volatile a reflection of relatively low group margins and high leverage to the economic cycle and labour markets.

Business Segment Workforce Services (Source - Company Reports)

Business Segment Workforce Services (Source - Company Reports)

The company’s balance sheet has been repaired following the global financial crisis and new leadership has implemented a new strategy. Key components of this new strategic approach include building scale in attractive, higher skill, higher margin segments and leveraging scale and brand strength in workforce services with a focus on customer service, cost efficiency and safety. Steady progress is being made with implementation. However earnings remain highly leveraged to the economic cycle. Given such high leverage to the business cycle we rate business risk as high. Although skilled is exposed to a number of attractive themes such as the trend to outsourcing and the high growth energy sector, it remains a highly cyclical stock.

Skilled Revene Comparison (Source - Company Reports)

Skilled Revene Comparison (Source - Company Reports)

We believe that the employment growth is expected to return to trend. The Australian economy which has consistently managed to create jobs growth of around 23% over the last century has had three years of below trend employment, with lead indicators suggesting some likely mean reversion towards growth. The recent ABS labour data for February showed solid rise in full time employment of 47,000 beating expectations.

SKE Daily Chart (Source - Thomson Reuters)

SKE Daily Chart (Source - Thomson Reuters)

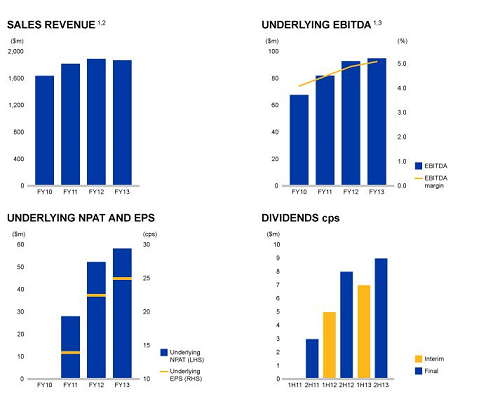

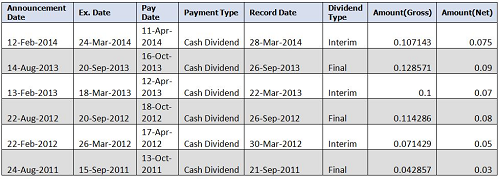

The company’s fiscal first half 2014 result was impacted by the mining slowdown and overall economic weakness, partially offset by cost reductions and the contribution from the Broadsword acquisition. Revenue fell 7% to AUD 906 million and earnings before interest and tax and depreciation, EBITDA fell 10% to AUD 43.9 million. A 7.5 cent per share dividend was declared. Management did not provide specific profit guidance except to say that the second half 2014 EBIT is expected to be higher than reported in the first half. Skilled group is in reasonable financial health. At the end of first half fiscal 2014, net debt stood at AUD 133 million. Given Skilled’s strong cash flow this is a reasonable level of debt. However we caution against significant increases.

Skilled’s Workforce (WF) business which accounts for 42% of FY141H EBITDA, provides temporary labour to a range of sectors such as FMCG, manufacturing government and infrastructure. This business has been in decline for a number of years, impacted by some structural issues within the sectors it services, such as manufacturing, as well as some more recent cyclical factors which have seen demand for casual labour weaken. Although some parts of Workforce such as mining are expected to remain challenging, we see upside from an improvement in hiring across other segments which WF services. Revenues in WF should recover as the cycle improves. SKE’s broad segment exposure should [position it well in a general economic upturn providing scope for earnings surprises.

Low levels of unemployment spur demand for temporary labour as permanent staff becomes harder to find or employers want to benefit from strong conditions without committing to a permanent increases in staff. The latter case can also be apparent at the initial stages of a recovery as employers remain cautious on the outlook but have an increased demand for labour. Skilled is improving processes, aggressively cutting costs and generating strong cash flow. The NAB business survey suggests employers hiring intentions have improved while growth in job advertisements also signals an improvement in jobs growth. We see scope for growth in professional and business services, where employment has traditionally been linked to the non-resource business capital expenditure cycle. Although capex has been weak over recent years we see likelihood of a return to more normal levels given the low starting point and accommodative financial conditions. Business capex has only been this low as a share of the economy in the early 1990’s recession, which leaves scope for a rebound in spend as housing and consumer expenditure improves.

Non mining and energy sectors represented 47% of Skilled’s FY13 revenue. The segments that are most prominent include FMCG (10% of revenues), primary manufacturing (9%), Govt and utilities (7%) and infrastructure (7%). A well-established franchise, with most businesses holding leading industry positions. Skilled is expected to benefit from a recovery in the domestic economy and strengthening labour market during fiscal 2015. A significant number of Skilled’s operations have direct exposure to the high growth oil & gas sector. Acquisitions have delivered benefits ahead of expectations. We will be putting a BUY on Skilled at the current price of $2.83.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...