Company Overview – Sirtex Medical Limited is a medical device company. The company develops and markets device for oncology treatments. Its SIR – Spheres microsphere is a medical device is a medical device used in selected internal radiation therapy for liver tumours, which contains radioactive yttrium – 90, Sirtex Medical uses small particle technology to develop the products. Its microspheres are injected into the main artery that supplies live tumours. The company offers microspheres with 32 microns of median diameter. SIR-Spheres microspheres are used in primary liver cancer (hepatocellular carcinoma) and secondary liver cancer (metastatic liver cancer), where the tumour has originated from another part of the body but has spread to the liver. It conducts research to develop products for patients with colorectal cancer. The company markets products in the Asia – Pacific, Europe, the Middle East, Africa and the Americas.

Analysis – SRX reported in the second quarter of FY14 SIR –Spheres dose sales growth of 18.7%, stronger than the three prior quarters. Dose sales growth in Americas which is 67% of the total doses led the way coming in at 23.7%, a solid improvement upon prior quarter weakness but softer than the 29.4% growth in the previous corresponding period. Asia pacific region was also stringer at 18.2% but below the longer term average of 31.1% over 3 years. Dose sales in Europe, Middle East and Africa which are 23% of total doses, at a share of 5.9% have recovered from first quarter 2014 weakness but continue to fight macro head winds (3 year Average 11.5%).

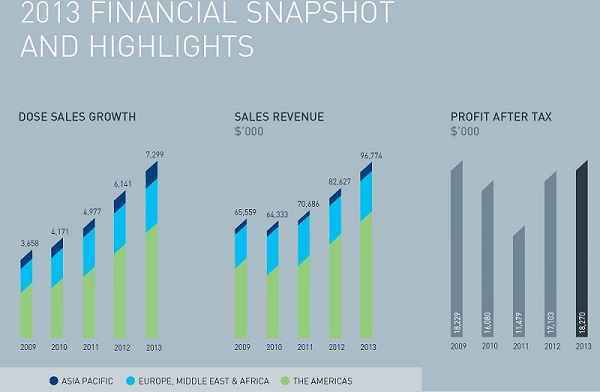

SRX’s selective internal radiation therapy for liver cancer treatment has achieved a widespread regulatory approval, but given a lack of controlled clinical trial data, it is currently used as a salvage therapy for ill patients which has seen the market penetration of less than 1% with 7299 doses sold in FY2013 versus a potential addressable market of almost 500,000 patients.

SRX has seen a robust growth with 38 quarters of consecutive dose sales growth, we would expect term growth to be sustained if not accelerate should outcomes from a series of clinical trials currently underway be consistently positive.

With gross profit margins of more than 80% any increase in revenue will flow through to earnings, however management are re-investing in the business via greater research and development spending as well as for marketing and distribution. We are encouraged by the return of growth across all regions and continued AUD weakness pointing to ongoing momentum.

|

SRX |

2013 |

2012 |

2011 |

2010 |

2009 |

|

Profitability |

|

|

|

|

|

|

Gross Margin |

81.9% |

81.0% |

80.7% |

83.2% |

80.8% |

|

EBITDA Margin |

25.7% |

27.6% |

18.4% |

21.0% |

32.6% |

|

Operating Margin |

25.3% |

26.8% |

20.4% |

26.5% |

31.3% |

|

DuPont/Earning Power |

|

|

|

|

|

|

Pretax ROA |

22.9% |

25.5% |

20.0% |

32.8% |

59.1% |

|

ROE |

22.6% |

25.6% |

20.6% |

35.4% |

58.4% |

|

Liquidity |

|

|

|

|

|

|

Quick Ratio |

3.82 |

4.23 |

4.28 |

3.93 |

4.20 |

|

Current Ratio |

3.90 |

4.28 |

4.36 |

4.00 |

4.35 |

Sirtex in June 2013 entered in to a co-marketing agreement with Surefire Medical Inc. a developer of infusion systems, to distribute Surefire’s range of infusion systems and speciality catheters for the interventional radiology and oncology markets. Under the agreement Sirtex will exclusively distribute the Surefire Medical range of products in the company’s rapidly growing Asia pacific markets including Australia.

The surefire infusion system has been designed to enhance the accuracy and delivery of drugs directly to tumours. Surefire products use a patented micro catheter with an expandable tip. When deployed the tip dynamically responds to flow conditions to enable more of the embolic agent to reach the intended destination while reducing non target delivery compared to traditional infusion systems. Surefire medical has received regulatory approval in US, Europe, Canada and NZ.

This agreement allows Sirtex and surefire medical to provide interventional radiologists and oncologists with a wider range of options. To improve patient outcomes and pursue more effective treatments for liver cancer. Burwood Chew, CEO of Sirtex Medical Asia Pacific said “ Sirtex is constantly looking for new ways to help our customers improve the outcomes of their patients with liver cancer. We believe this distribution partnership will allow us to provide interventional radiologists and oncologists with a wider range of options that may potential lead to improved patient outcomes. Which is our shared goal.”

|

Price |

Price % Change |

|

Close: |

14.10 (31-Jan-2014) |

3M: |

13.34% |

|

52 Wk High: |

14.59 (13-Jan-2014) |

6M: |

13.07% |

|

52 Wk Low: |

9.36 (05-Apr-2013) |

1Y: |

16.72% |

The major risks associated with SRX include execution on business strategy, new therapies that may be introduced to treat similar conditions, further clinical trials – quality of results and incremental benefits displayed, change in private health fund reimbursement and government funding (less relevant in oncology), market acceptance and awareness of the products offered, influence of government regulation, competitor activity, quality of clinical trial results and granting of regulatory approval, endorsement of the treatment by high profile cancer experts along with medical journals and rate of adoption by physicians.

Source - Company Reports

Source - Company Reports

|

SRX |

2013 |

2012 |

2011 |

2010 |

2009 |

|

Total Revenue |

96.77 |

82.63 |

70.29 |

72.09 |

73.89 |

|

Gross Profit |

79.22 |

66.96 |

56.74 |

53.51 |

52.95 |

|

Total Operating Expense |

72.27 |

60.51 |

55.94 |

52.99 |

50.74 |

|

Net Income |

18.27 |

17.10 |

11.48 |

16.08 |

18.23 |

SRX reports regional dosage information on a quarterly basis and given relatively low volumes of dosages there has been considerable volatility seen with the first quarter of 2014 update revealing a 5.1% decline for Europe, Middle East and Africa where as a positive extreme was the 47% increase for the US in the third quarter of 2012, notwithstanding this volatility the company has achieved 38 consecutive quarters of dose sales growth with the most recent update revealing a 18.7% growth of 18.7% for second quarter 2014.

The Americas is the largest market for SRX generating $69.8 Million in revenue in FY2013 with dose sales of 4765 representing growth of 22% respectively. Europe, Middle East and Africa saw sales growth of 9% in FY2013 to 1814 which is 25% of the total sales and with a revenue growth of 3%.

From a low base Asia Pacific dose sales grew by 29% to 720 generating revenue of $4.8 Million.

Given nearly all revenue is generated from offshore. Movements of the Australian $ against the US Dollar and Euro will have a material impact on reported profitability.

Although SIRT is a last line salvage treatment at present we do see double digit growth in dose sales as being readily achievable over the next few years in view of the growth over the past decade and the expansion of distribution taken over FY 2013 via set up of new treatment centres.

We feel more comfortable anticipating positive clinical outcomes given the readily understandable action mechanisms of the SIRT process and the implied positive factor of a decade long track record of dosage sales growth. We initiate coverage of SRX with a BUY recommendation.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...