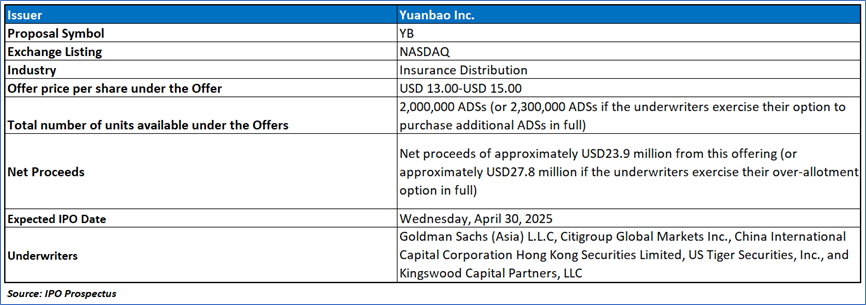

The Offer

Company Overview

Yuanbao Inc. (YB), a leading technology-driven online insurance distributor in China, specializes in the seamless integration of insurance with advanced technologies, operating a highly efficient full consumer service cycle engine that has distributed tailored, high-quality insurance products to over ten million consumers, making it the largest independent distributor in China’s personal life and accident & health (A&H) insurance market by first-year premiums in 2023, according to Frost & Sullivan. The Company’s scalable engine, supported by approximately 4,700 models as of December 31, 2024, leverages predictive capabilities and interconnected networks to provide personalized services across recommendation, purchasing, policy management, claims, and post-sales, optimizing outcomes across diverse media channels, consumer preferences, and product offerings. Yuanbao collaborates robustly with insurance carriers, enabling them to develop flagship products that attract and retain a vast consumer base, while utilizing big data to deepen insights into consumer behavior, thereby enhancing both consumer satisfaction and carrier sales.

Key Highlights

Primary Offering:

2,000,000 ADSs (or 2,300,000 ADSs if the underwriters exercise their option to purchase additional ADSs in full)

Use of proceeds:

- Overview of Proceeds and Offering Structure: Yuanbao Inc. (YB) estimates receiving net proceeds of approximately USD24.9 million from its initial public offering and concurrent private placements, or USD28.8 million if the underwriters fully exercise their option to purchase additional American Depositary Shares (ADSs), based on an assumed initial public offering price of USD14.00 per ADS, the midpoint of the estimated range, after deducting underwriting discounts, commissions, and offering expenses. The primary objectives of this offering include creating a public market for the Company’s shares, facilitating equity incentives for employee retention, and securing additional capital to support business growth. Pending utilization, the net proceeds will be invested in short-term or demand deposits to ensure liquidity and flexibility.

- Planned Utilization of Proceeds: The Company intends to allocate the net proceeds strategically to bolster its operations in mainland China, with approximately 40% dedicated to enhancing the consumer service cycle engine of the PRC Operating Entities, 30% invested in advancing core technology models and data insights, 20% directed toward expanding consumer reach and geographical coverage, and 10% reserved for working capital and other general corporate purposes. These allocations reflect Yuanbao’s focus on strengthening its technological infrastructure, broadening its market presence, and ensuring operational sustainability. However, management retains significant discretion to adjust these plans in response to unforeseen events or changing business conditions.

- Regulatory Considerations and Funding Mechanisms: As an offshore holding company, Yuanbao is subject to mainland China’s regulations, which permit funding to its mainland China subsidiary only through loans or capital contributions, and to the Variable Interest Entity (VIE) solely through loans, contingent on government registration and approval processes that may face delays or denials, potentially impacting liquidity and the ability to expand the PRC Operating Entities’ operations. The Company acknowledges these regulatory challenges as a risk factor that could materially affect its funding strategy and business growth. Despite these constraints, Yuanbao aims to deploy the proceeds efficiently to support its strategic objectives while navigating the applicable legal framework.

Dividend policy:

Yuanbao Inc.’s board of directors holds discretionary authority to determine dividend distributions, subject to Cayman Islands law, which permits dividends only from profits or share premium and prohibits payments that would impair the Company’s ability to meet its debts, with shareholders able to declare dividends up to the amount recommended by the board based on future operations, earnings, capital needs, financial condition, and other relevant factors. The Company currently has no plans to pay cash dividends in the foreseeable future post-offering, intending instead to retain funds and future earnings to support the expansion of its PRC Operating Entities’ business, while relying on dividends from its mainland China subsidiary, subject to potential restrictions under PRC regulations, with any dividends on ordinary shares represented by ADSs paid in U.S. dollars through the depositary to ADS holders in proportion to their holdings.

Industry Landscape for Yuanbao Inc.

- Growth and Penetration of China’s Internet Market: The internet market in China has witnessed consistent expansion, with the number of internet users rising to 1.09 billion in 2023 and projected to reach 1.31 billion by 2028, alongside an internet penetration rate increasing to 77.5% in 2023, expected to climb to 93.3% by 2028, according to Frost & Sullivan. This growth, coupled with an average of 29.1 hours spent online per user weekly in 2023 and a rising per capita income from RMB88.6 thousand in 2023 to a forecasted RMB118.5 thousand in 2028, has bolstered consumer spending power and fueled innovation across industries, notably enhancing the foundation for e-commerce and the online insurance sector. The adoption of online retail sales, with a penetration rate of 32.3% in 2023 projected to reach 37.8% by 2028, contrasts with the online insurance sales penetration rate of 12.3% in 2023, anticipated to grow to 30.2% by 2028, indicating a significant opportunity for market development.

- Development of China’s Personal Life and Accident & Health Insurance Market: China’s personal life and accident & health (A&H) insurance market has demonstrated steady growth, achieving a gross written premium (GWP) of RMB3.8 trillion in 2023, up from RMB3.1 trillion in 2019 with a compound annual growth rate (CAGR) of 5.0%, and is expected to reach RMB5.6 trillion by 2028 with a CAGR of 8.3%, driven by rapid health insurance growth from RMB0.7 trillion in 2019 to RMB0.9 trillion in 2023 (CAGR of 6.3%) and a projected RMB1.4 trillion by 2028 (CAGR of 9.9%), per Frost & Sullivan. Online distribution channels have gained traction, accounting for 14.6% of GWP in 2023, up from 6.0% in 2019, with projections to reach 35.9% by 2028, as online GWP grew from RMB0.2 trillion in 2019 to RMB0.6 trillion in 2023 (CAGR of 31.1%) and is forecasted to hit RMB2.0 trillion by 2028 (CAGR of 29.7%), outpacing offline growth rates of 2.5% and 2.3% over the same periods. This shift reflects an evolving consumer preference for online platforms that enhance purchasing and claim experiences, supported by the market’s second-largest global ranking by premium income in 2022.

- Market Drivers and Distribution Trends: Key growth drivers include an aging population, with the proportion of individuals aged 65 and over expected to rise from 14.2% in 2021 to 20.5% by 2030, totaling 323 million, prompting increased demand for elder care and pension solutions, bolstered by government policies encouraging commercial insurance to alleviate social pressures. Additionally, the expansion of commercial health and pension insurance as supplements to China’s basic medical and three-pillar pension systems—where pension investment remains low at 12% of GDP in 2022 compared to 30% in Japan, 89% in the UK, and 134% in the US—signals a gap that government initiatives aim to address, alongside rising disposable income (RMB39,218 per capita in 2023 with a 7.9% CAGR over ten years) and heightened health awareness post-COVID-19. Distribution channels are shifting, with distributors, including Yuanbao as the largest independent player with RMB17.6 billion in first-year premiums in 2023, growing at a CAGR of 34.2% from 2019 to 2023 and projected at 35.5% to RMB1,083 billion by 2028, outpacing traditional channels like agent-led sales (44.5% of GWP) and bancassurance (34.5%), reflecting a trend toward online, consumer-centric, and technology-driven models.

- Technological and Competitive Dynamics: The insurance industry is being transformed by advanced technologies such as data analytics and artificial intelligence, which enhance product development, distribution, risk management, and fraud detection, contributing to a more efficient ecosystem, while China’s insurance penetration rate of 3.9% in 2022, projected to reach 5.0% by 2027, lags behind mature markets like the US (11.6% in 2022, 12.9% by 2027), UK (10.5% to 11.5%), and Japan (8.2% to 9.3%). Distributors are adopting a consumer-centric approach, leveraging diverse marketing channels and partnerships with carriers to meet evolving demands, with Yuanbao, as an independent distributor since 2020, ranking second overall and leading among independents in 2023, ahead of competitors like Company A (USD51.3 billion, dependent, online) and Company B (USD10.8 billion, offline, independent). This competitive landscape underscores significant growth potential, with distributors expected to increase their market share from 6.3% in 2023 to 19.3% by 2028, driven by professionalization, technological adoption, and strengthened carrier collaborations.

Financial Highlights (Results of Operations) (Expressed in USD)

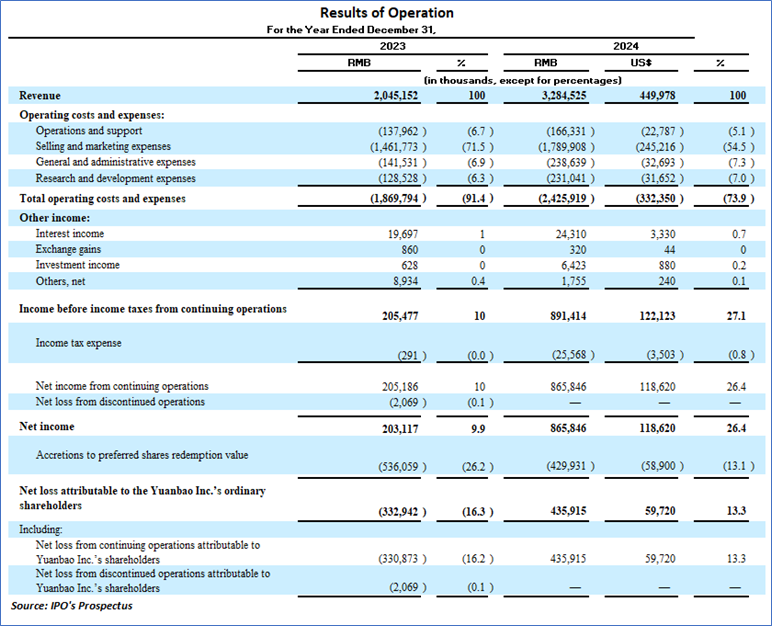

- Growth Metrics and Profitability: The Company has demonstrated robust growth, with revenue increasing by 60.6% from RMB2,045.2 million in 2023 to RMB3,284.5 million (USD450.0 million) in 2024, driven by a 51.9% rise in insurance distribution revenue to RMB1,081.3 million (USD148.1 million) and a 66.1% surge in system services revenue to RMB2,194.2 million (USD300.6 million), reflecting enhanced marketing and analytics capabilities. Key operating metrics highlight this expansion, with insurance consumers growing from 8.1 million to 13.9 million, new policies from 12.5 million to 22.4 million, and first-year premiums from RMB17.6 billion to RMB28.6 billion (a 62.8% increase) between 2023 and 2024, underscoring strong consumer engagement and market competitiveness. Achieving profitability within three years, Yuanbao reported net income of RMB205.2 million in 2023 and RMB865.8 million (USD118.6 million) in 2024, alongside net cash from operating activities of RMB426.6 million and RMB1,207.6 million (USD165.4 million), respectively, signaling financial stability.

- Liquidity and Capital Resources: As of December 31, 2024, Yuanbao maintains solid liquidity with cash and cash equivalents of RMB1,904.7 million (USD260.9 million), up from RMB863.1 million in 2023, supported by time deposits of RMB80.0 million (USD11.0 million) and restricted cash of RMB15.0 million (USD2.1 million), primarily for regulatory deposits, with operations funded through cash flows and past financing. The Company believes its current cash reserves are adequate for the next 12 months to cover operating activities, capital expenditures (RMB3.3 million in 2024), and lease payments (RMB19.7 million undiscounted, with RMB13.9 million due in 2025), though it may seek additional financing, which could dilute shareholders or impose covenants, with no assurance of favorable terms. Substantially all cash is held in mainland China, subject to VIE contractual arrangements and PRC regulatory constraints that may limit fund transfers.

- Operational Cash Flow and Future Commitments: Net cash from operating activities reached RMB1,207.6 million (USD165.4 million) in 2024, exceeding net income due to non-cash adjustments like RMB64.0 million (USD8.8 million) in share-based compensation and changes in working capital, including increased accrued expenses (RMB170.2 million) and contract liabilities (RMB50.2 million) reflecting business growth, offset by higher accounts receivable (RMB16.2 million). Investing activities used RMB157.6 million (USD21.6 million) in 2024, mainly for short-term investments, while financing activities utilized RMB9.1 million (USD1.2 million), indicating minimal external funding needs. Yuanbao plans to meet future cash requirements, including capital expenditures and lease obligations, with existing cash and potential financing, supporting ongoing business expansion.

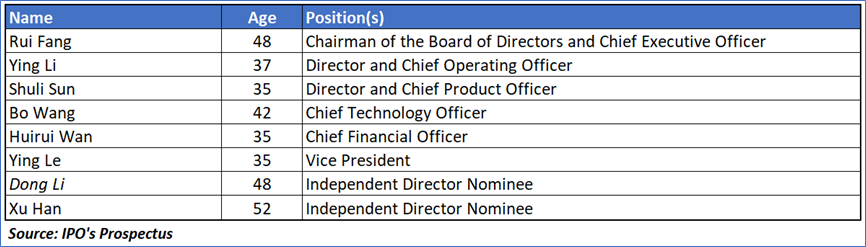

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “YB” is exposed to a variety of risks such as:

- Limited Operating History and Growth Sustainability Challenges: Yuanbao Inc. (YB), through its PRC Operating Entities, began offering online insurance distribution and services in 2020, achieving rapid growth with a 60.6% revenue increase from RMB2,045.2 million in 2023 to RMB3,284.5 million (USD450.0 million) in 2024; however, this limited history and evolving business model present uncertainties, as historical performance may not predict future results, particularly in maintaining growth rates and profitability amidst a dynamic online insurance market.

- Intense Competition in a Rapidly Evolving Industry: The PRC Operating Entities operate in a highly competitive and rapidly evolving insurance distribution industry in mainland China, facing challenges from diverse competitors, including online independent platforms, traditional intermediaries, direct sales channels of large insurers, major internet companies, and other technology firms, many of which may possess greater resources, better brand recognition, and the ability to offer more attractive products or pricing. Failure to compete effectively could lead to reduced demand for their services, lower operating margins, loss of market share, and difficulties in retaining qualified employees, compounded by the industry’s ongoing transformation through technological advancements and shifting consumer habits, making future prospects difficult to predict and potentially impacting financial performance.

- Regulatory Compliance and Evolving Legal Environment: Yuanbao’s PRC Operating Entities operate in a highly regulated industry under the oversight of the National Administration of Financial Regulation (NAFR), with an evolving regulatory framework introducing challenges such as compliance with new laws like the 2021 Notice on Internet Personal Insurance Business, which imposes stringent requirements on online insurance operations and limits marketing activities, potentially affecting business scope and profitability. Non-compliance or inability to adapt to regulatory changes, including obtaining necessary licenses and permits, could result in penalties, operational restrictions, or termination of services, while regulatory reviews and inspections may divert management focus and resources, materially adversely affecting the Entities’ business, financial condition, and results of operations.

Conclusion

Yuanbao Inc. (YB), a prominent technology-driven online insurance distributor in China, leverages its advanced full consumer service cycle engine—supported by approximately 4,700 models as of December 31, 2024—to deliver personalized insurance products to over ten million consumers, establishing itself as the largest independent distributor in China’s personal life and accident & health (A&H) insurance market by first-year premiums in 2023, according to Frost & Sullivan, while collaborating with carriers to enhance product offerings and consumer insights through big data analytics. The Company is launching an initial public offering of 2,000,000 ADSs (or 2,300,000 with over-allotment) at an assumed price of USD14.00 per ADS, expecting net proceeds of USD24.9 million (or USD28.8 million with over-allotment) to be allocated with 40% for enhancing its engine, 30% for technology and data insights, 20% for consumer reach, and 10% for working capital, though subject to management discretion and potential regulatory delays in funding its PRC Operating Entities due to China’s loan and capital contribution restrictions. The online insurance market, underpinned by a growing internet user base of 1.09 billion in 2023 projected to reach 1.31 billion by 2028 and an online sales penetration rate expected to rise from 12.3% in 2023 to 30.2% by 2028, aligns with Yuanbao’s revenue growth of 60.6% to RMB3,284.5 million (USD450.0 million) in 2024, net income of RMB865.8 million (USD118.6 million), and a robust cash position of RMB1,904.7 million (USD260.9 million), though it currently plans to retain earnings for business expansion rather than pay dividends, relying on its mainland China subsidiary subject to PRC regulatory constraints.

However, investing in Yuanbao’s IPO involves notable risks, including its limited operating history since 2020, which may not sustain its rapid growth or profitability amidst an evolving online insurance market, potentially affecting investor confidence and ADS pricing. The Company faces intense competition from well-resourced online platforms, traditional intermediaries, and major internet firms, which could erode market share and margins if Yuanbao fails to innovate or retain talent, while its highly regulated environment under the National Administration of Financial Regulation (NAFR)—with evolving laws like the 2021 Notice on Internet Personal Insurance Business—poses compliance challenges that could lead to penalties or operational restrictions if not managed effectively.

Hence, given the financial performance of the company, use of proceeds, and associated risks “Yuanbao Inc. (YB)” IPO seems “Attractive" at the IPO price.

Disclaimer-

This report has been issued by Kalkine Pty Limited (ABN 34 154 808 312) (Australian financial services licence number 425376) (“Kalkine”) and prepared by Kalkine and its related bodies corporate authorised to provide general financial product advice. Kalkine.com.au and associated pages are published by Kalkine.

Any advice provided in this report is general advice only and does not take into account your objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your objectives, financial situation and needs before acting upon it.

There may be a Product Disclosure Statement, Information Statement or other offer document for the securities or other financial products referred to in Kalkine reports. You should obtain a copy of the relevant Product Disclosure Statement, Information Statement or offer document and consider the statement or document before making any decision about whether to acquire the security or product.

Choosing an investment is an important decision. If you do not feel confident making a decision based on the recommendations Kalkine has made in our reports, you should consider seeking advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) before acting on any advice in this report or on the Kalkine website. Not all investments are appropriate for all people.

The information in this report and on the Kalkine website has been prepared from a wide variety of sources, which Kalkine, to the best of its knowledge and belief, considers accurate. Kalkine has made every effort to ensure the reliability of information contained in its reports, newsletters and websites. All information represents our views at the date of publication and may change without notice. The information in this report does not constitute an offer to sell securities or other financial products or a solicitation of an offer to buy securities or other financial products. Our reports contain general recommendations to invest in securities and other financial products.

Kalkine is not responsible for, and does not guarantee, the performance of the investments mentioned in this report This report may contain information on past performance of particular investments. Past performance is not an indicator of future performance. Hypothetical returns may not reflect actual performance. Any displays of potential investment opportunities are for sample purposes only and may not actually be available to investors. To the extent permitted by law, Kalkine excludes all liability for any loss or damage arising from the use of this report, the Kalkine website and any information published on the Kalkine website (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine hereby limits its liability, to the extent permitted by law, to the resupply of services..

Please also read our Terms & Conditions and Financial Services Guide for further information. Employees and/or associates of Kalkine and its related entities may hold interests in the securities or other financial products covered in this report or on the Kalkine website. Any such employees and associates are required to comply with certain safeguards, procedures and disclosures as required by law.

Kalkine Media Pty Ltd, an affiliate of Kalkine Pty Ltd, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website including entities covered in this Report.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...