Kalkine has a fully transformed New Avatar.

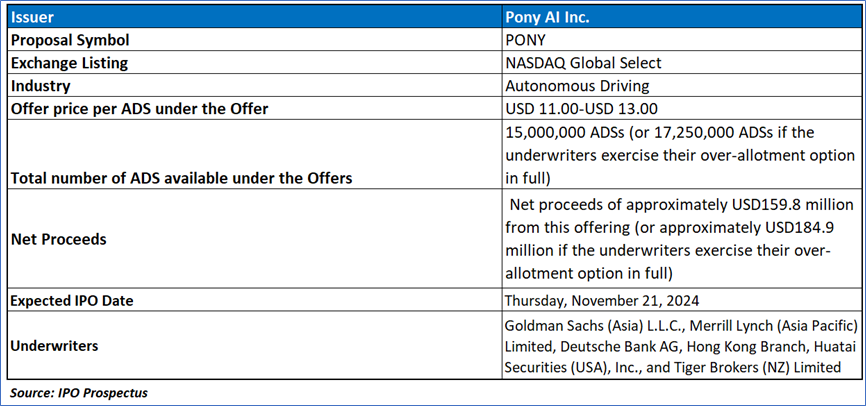

The Offer

Company Overview

Pony AI Inc (PONY) has emerged as a global leader in the large-scale commercialization of autonomous mobility, transforming science fiction into reality on the bustling streets of China. Its driverless robotaxis, hailed through the PonyPilot app, seamlessly integrate into daily life, offering a safe, intuitive, and eco-friendly commuting option. Equipped with advanced sensors, these vehicles navigate complex urban environments with precision, handling obstacles and inclement weather conditions autonomously. Passengers enjoy a smooth, driver-free journey, paying fares via the app, as the robotics depart to serve the next rider. Pony’s innovation is reshaping urban mobility and paving the way for a futuristic transportation ecosystem.

Key Highlights

Primary Offering:

The total number of ADS available under the offers includes 15,000,000 ADSs (or 17,250,000 ADSs if the underwriters exercise their over-allotment option in full).

Use of proceeds:

Based on an assumed initial public offering price of USD 12.00 per ADS, the company anticipates net proceeds of approximately USD 159.8 million from the offering (or USD 184.9 million if underwriters fully exercise their over-allotment option) and an additional USD 153.4 million from concurrent private placements, after deducting estimated expenses. The net proceeds will be allocated primarily to three areas: 40% (USD 125.3 million) to implement go-to-market strategies for the large-scale commercialization of autonomous driving technology, including robotaxi and robotruck services; 40% (USD 125.3 million) for further investment in research and development; and 20% (USD 62.6 million) for general corporate purposes and potential strategic acquisitions, although no specific opportunities have been identified yet.

The allocation of proceeds may change due to unforeseen events or shifts in business conditions. The company faces regulatory constraints under PRC laws, which limit funding to Chinese subsidiaries through loans or capital contributions unless specific governmental requirements are met, potentially impacting liquidity and expansion plans. Until deployment, the funds will be held in short-term, interest-bearing financial instruments or demand deposits.

Industry Overview:

Dividend policy:

Pony has not previously declared or paid dividends in cash or kind and does not plan to do so in the near future, as it intends to retain available funds and earnings to support business operations and expansion. As a Cayman Islands holding company, Pony relies primarily on dividends from its PRC subsidiaries to meet cash requirements, including potential shareholder dividends. However, PRC regulations may limit these subsidiaries’ ability to distribute dividends, posing potential risks to its operations. Dividend declarations are subject to the discretion of the board of directors and compliance with Cayman Islands law, which permits dividend payments only from profits, retained earnings, or share premium, provided it does not impair the company’s ability to meet debt obligations. Any future dividends will depend on various factors, including operational performance, financial condition, and contractual obligations, and would be distributed to ADS holders via the depositary under the terms of the deposit agreement.

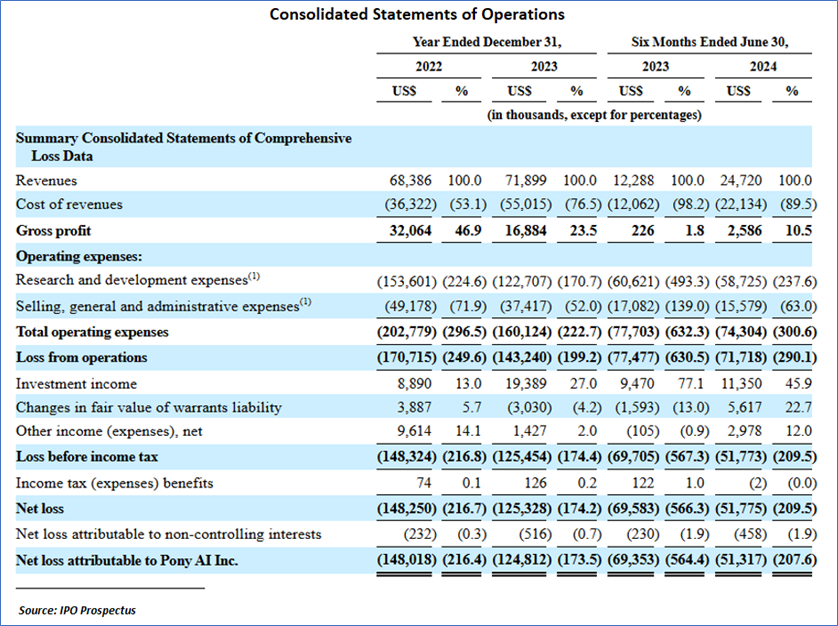

Financial Highlights (Results of Operations) (Expressed in USD)

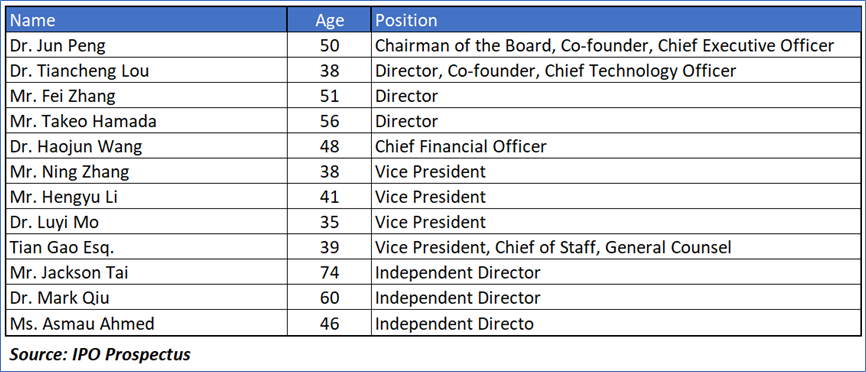

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “PONY” is exposed to a variety of risks such as:

Conclusion

Pony’s IPO offers an opportunity to invest in a global leader in autonomous mobility, leveraging its robotaxi and robotruck services to drive revenue growth and reshape urban transportation. The company’s focus on commercialization, supported by advancements in AI and electric vehicle technologies, positions it well within a rapidly evolving market projected to grow significantly. However, several risks must be considered, including heavy reliance on its PRC subsidiaries for cash flow amid stringent regulations, challenges in achieving large-scale commercialization of its technologies, and dependency on key partnerships for market penetration. Financially, the company demonstrates strong revenue growth and improved gross margins, but profitability remains constrained by high operating costs and capital investment requirements.

Hence, given the financial performance of the company, use of proceeds, and associated risks “Pony AI Inc (PONY)” IPO seems “Neutral" at the IPO price.

This report has been issued by Kalkine Pty Limited (ABN 34 154 808 312) (Australian financial services licence number 425376) (“Kalkine”) and prepared by Kalkine and its related bodies corporate authorised to provide general financial product advice. Kalkine.com.au and associated pages are published by Kalkine.

Any advice provided in this report is general advice only and does not take into account your objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your objectives, financial situation and needs before acting upon it.

There may be a Product Disclosure Statement, Information Statement or other offer document for the securities or other financial products referred to in Kalkine reports. You should obtain a copy of the relevant Product Disclosure Statement, Information Statement or offer document and consider the statement or document before making any decision about whether to acquire the security or product.

Choosing an investment is an important decision. If you do not feel confident making a decision based on the recommendations Kalkine has made in our reports, you should consider seeking advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) before acting on any advice in this report or on the Kalkine website. Not all investments are appropriate for all people.

The information in this report and on the Kalkine website has been prepared from a wide variety of sources, which Kalkine, to the best of its knowledge and belief, considers accurate. Kalkine has made every effort to ensure the reliability of information contained in its reports, newsletters and websites. All information represents our views at the date of publication and may change without notice. The information in this report does not constitute an offer to sell securities or other financial products or a solicitation of an offer to buy securities or other financial products. Our reports contain general recommendations to invest in securities and other financial products.

Kalkine is not responsible for, and does not guarantee, the performance of the investments mentioned in this report This report may contain information on past performance of particular investments. Past performance is not an indicator of future performance. Hypothetical returns may not reflect actual performance. Any displays of potential investment opportunities are for sample purposes only and may not actually be available to investors. To the extent permitted by law, Kalkine excludes all liability for any loss or damage arising from the use of this report, the Kalkine website and any information published on the Kalkine website (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine hereby limits its liability, to the extent permitted by law, to the resupply of services..

Please also read our Terms & Conditions and Financial Services Guide for further information. Employees and/or associates of Kalkine and its related entities may hold interests in the securities or other financial products covered in this report or on the Kalkine website. Any such employees and associates are required to comply with certain safeguards, procedures and disclosures as required by law.

Kalkine Media Pty Ltd, an affiliate of Kalkine Pty Ltd, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website including entities covered in this Report.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...