The Offer

Company Overview

Picard Medical, Inc. (PMI) serves as a holding company fully owning SynCardia Systems, LLC, a medical technology firm focused on the SynCardia Total Artificial Heart (TAH)—the sole FDA- and Health Canada-approved implantable TAH, with over 2,100 units implanted across 27 countries as a bridge to transplantation for biventricular heart failure patients. The system includes artificial ventricles, external pneumatic drivers for hospital and home use, and drivelines, implanted via standard surgical methods to deliver pulsatile flow. The company's roadmap involves enhancing driver technology, broadening indications to Bridge to Candidacy and long-term use (two years+), expanding globally, and pioneering the fully implantable Emperor TAH as a transplant alternative, with prototypes in testing, animal studies slated for early 2025, and potential FDA approval by 2028. Facing competitors like Carmat's Aeson TAH, BiVACOR's clinical trials, and off-label LVAD combinations, Picard emphasizes its clinical expertise, intellectual property, and advantages in mechanical circulatory support. In 2025, it pursued an NYSE IPO to secure approximately USD 17 million for growth and innovation.

Key Highlights

Primary Offering:

34,250,000 shares (underwriters an option to purchase up to an additional 637,500 shares)

Use of proceeds:

- Estimated Net Proceeds: Picard Medical, Inc. anticipates receiving net proceeds of approximately USD 15.4 million from the sale of common stock in its initial public offering, based on an assumed price of USD 4.00 per share, the midpoint of the indicated range, after deducting underwriting discounts, commissions, and estimated offering expenses. A USD 0.50 increase or decrease in the offering price would adjust the net proceeds by about USD 2.0 million, assuming the number of shares remains constant. Similarly, an increase or decrease of one million shares offered would alter the net proceeds by approximately USD 3.8 million, holding the assumed price steady. These funds are primarily intended to bolster operational capital, establish a public market for the company's stock, and enhance future access to equity markets.

- Allocation of Net Proceeds: The company plans to allocate the net proceeds as follows: USD 2.85 million to fund SynCardia Medical (Beijing), Inc., for distribution rights with a local sales distributor, with the contribution occurring upon the offering's closing; up to USD 3.36 million for research and development of its fully implantable system, including early feasibility animal trials and design activities; approximately USD 0.50 million to enhance sales, marketing, and distribution capabilities for its total artificial heart system, covering additional inventory and driver expansion; USD 0.5 million for working capital, including vendor payments; USD 0.20 million for general corporate purposes such as executive travel and board meetings; and USD 0.39 million for operational expenses like facility rent and utilities. Additionally, up to USD 5.6 million will satisfy related party Senior Secured Notes, including accrued interest, and USD 2.0 million will address working capital related party loans. Management retains discretion over the precise application of these funds, subject to business conditions and risk factors.

- Senior Secured Notes Overview: The Senior Secured Notes comprise a series of related party obligations issued between October 2024 and July 2025, totaling approximately USD 5.6 million in principal and interest. This includes a USD 250,000 working capital loan issued on August 20, 2024, and amended on July 1, 2025; a USD 93,633 note to Hunniwell for travel reimbursements; a USD 187,190 note to Daniel Teo for severance; and a USD 425,000 note issued on July 8, 2025, to Fang Family Fund I, LLC, affiliated with an executive director. These notes bear 6% annual interest, with principal and interest due by October 15, 2025, at the company's election or upon demand. They are secured by a continuing interest in the company's collateral, and their maturity dates were extended to October 15, 2025, on July 1, 2025.

Dividend policy:

Picard Medical Inc currently plans to retain all available funds and future earnings to support the ongoing operations and growth of its business, with no intention to declare or pay dividends on its capital stock in the near term.

Cardiovascular Disease Industry and International Expansion Overview

- Global Burden of Heart Failure: Cardiovascular disease remains the primary cause of mortality in the United States and worldwide. Recent studies from 2024 indicate that approximately 6.8 million individuals in the United States and 56.2 million globally are affected by heart failure. In the United States alone, one in four people experiences heart failure, contributing to 680,909 deaths from heart disease in 2023, while global heart failure fatalities approach 18 million annually. Despite modest improvements in prognosis over recent decades, mortality rates in the United States stand at around 10% within 30 days, 20–30% at one year, and 45–60% over five years. These rates vary regionally, with the highest observed in Africa and India, and the lowest in China, South America, and the Middle East.

- Heart Transplantation and Market Dynamics: Heart transplantation serves as the preferred treatment for select patients with advanced or end-stage heart failure, a condition affecting at least 300,000 individuals in the United States, where prevalence estimates range from 5% to 25%. However, donor heart supply falls short of demand, with over 7,500 patients on the U.S. transplant waiting list and more than 4,000 added annually; in 2023, only 4,539 transplants occurred domestically, compared to an estimated 8,200 worldwide in 2020. The global heart implant market extends significantly beyond the United States, encompassing approximately 15 million annual heart failure cases in the European Union, up to 4.6 million in India, 12 million in China, and 3.75 million in the Middle East. Pricing flexibility varies by region, yet international growth represents a pivotal strategy for future success.

- International Presence and Expansion Initiatives: Picard Medical, Inc., through its subsidiary SynCardia Systems, LLC, is actively pursuing global expansion. In China, SynCardia Medical (Beijing), Inc., established in July 2022, is positioned to handle registration and distribution of the SynCardia Total Artificial Heart (TAH) under a Capital Increase Agreement dated July 2, 2023, whereby Picard will invest USD 2.85 million for a 60% stake, contingent on public listing. Exclusive distribution and regulatory affairs agreements outline responsibilities, including NMPA registration based on FDA data, with potential approval within 12 months of filing, though not guaranteed. In India, dual strategies involve seeking an MD-15 import license and emergency use clearances via the CDSCO, alongside preparations for individual patient licenses and clinical data collection. In the Middle East, partnerships with hospitals in Saudi Arabia have led to initial sales and an ongoing SFDA application submitted in May 2023. Discussions are underway with potential partners in the United Kingdom, Southeast Asia, Eastern and Central Europe, Latin America, and other regions, with plans for regional transplant hubs. Regulatory approvals in these markets, including the EU and UK, are sought but not assured on anticipated timelines.

Financial Highlights (Results of Operations) (Expressed in USD)

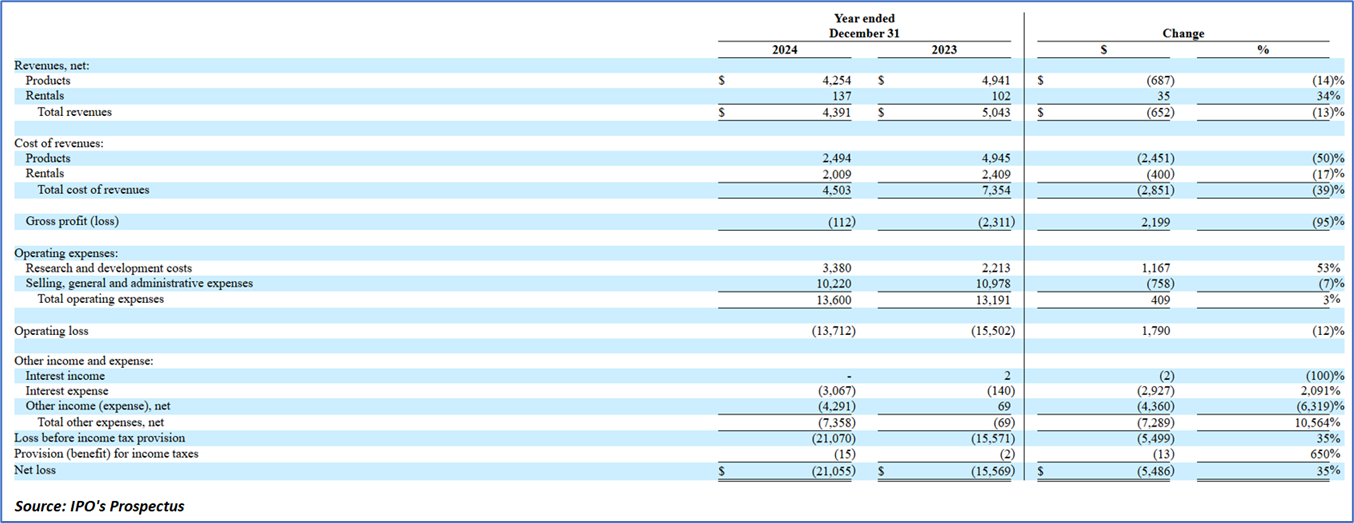

- Revenue Analysis: For the three months ended March 31, 2025, Picard Medical, Inc. experienced a significant decline in total revenues by USD 1.4 million, or 69%, compared to the corresponding period in 2024. This reduction was primarily attributed to a USD 1.0 million decrease in U.S. sales and a USD 0.3 million drop in foreign sales. A key factor in the U.S. revenue shortfall was the contribution from the company's largest customer, which fell from USD 1.3 million in the prior period to USD 0.3 million in 2025.

- Cost of Revenues: The total cost of revenues decreased by USD 0.2 million, or 17%, for the three months ended March 31, 2025, relative to the same period in 2024, largely due to lower rental costs. Rental revenue and costs exhibit an indirect correlation, as revenue is accrued upon probable receipt following patient discharge with a Freedom Driver, whereas costs encompass scheduled maintenance irrespective of usage duration or patient turnover. Consequently, this led to a negative gross margin of 58% in the 2025 period, with costs constituting 158% of total sales, up from 59% in 2024.

- Operating Expenses: Research and development expenses increased by USD 0.1 million, or 17%, in the three months ended March 31, 2025, compared to the prior year, driven mainly by elevated labor costs; although supplies are allocated by product, personnel expenses remain undifferentiated, with staff dedicated exclusively to development activities. Selling, general, and administrative expenses rose by USD 0.1 million, or 5%, over the same timeframe, also primarily due to higher labor expenditures. Total other expenses escalated by USD 2.2 million, or 2,685%, owing to non-cash derivative accounting associated with convertible notes.

- Liquidity and Capital Resources: Picard Medical, Inc. has recorded persistent operating losses since inception, including USD 21.1 million for the year ended December 31, 2024, and USD 5.6 million for the three months ended March 31, 2025, as it scales revenue from FDA-approved products while investing in innovations and preparing for public company operations. Future financing is expected via equity, debt, or related-party sources, potentially diluting shareholders or imposing restrictive terms; substantial doubt persists regarding going concern viability, necessitating adjustments absent additional capital, though financial statements assume continuity. As of March 31, 2025, cash equivalents stood at USD 688,000, historically supported by Series A-1 Preferred Stock (converted in July 2025), related-party loans (USD 4.8 million outstanding at 6% interest), and convertible notes (USD 9.5 million balance with IPO-triggered conversions). Cash flows for the quarter reflected USD 2.2 million used in operations (from net loss offset by working capital shifts), no investing activity, and USD 2.8 million from financing (convertible notes, related-party loans, and stock issuance); 2024 annual flows showed USD 11.9 million operational outflow, minimal investing, and USD 11.7 million financing inflow.

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “PMI” is exposed to a variety of risks such as:

- Risk of Sustained Losses and Profitability Challenges: The company has a history of substantial net losses, amounting to USD 21.1 million and USD 15.6 million for the years ended December 31, 2024, and 2023, respectively, and USD 5.6 million and USD 2.0 million for the three months ended March 31, 2025, and 2024. With an accumulated deficit of USD 55.4 million as of March 31, 2025, ongoing investments in sales expansion, manufacturing, regulatory approvals, and research are expected to perpetuate these losses. Failure to achieve sufficient revenue growth or commercialize new products could exacerbate working capital constraints, potentially hindering the company's ability to attain or maintain profitability and adversely affecting stockholder equity.

- Risk of Product Dependence and Market Acceptance: Substantially all revenue derives from a narrow range of products, including the SynCardia 50cc and 70cc TAH, associated drivers, and ancillary hardware, with future reliance anticipated on driver rentals. Any decline in sales, quality issues, component shortages, or regulatory setbacks could eliminate the primary revenue source. Moreover, limited market acceptance by physicians and hospitals—due to competition from established left ventricular assist devices (LVADs), reluctance to adopt new technologies, or emotional barriers related to native heart removal—may impede growth. Inadequate peer-reviewed publications or advocacy could further limit adoption, constraining cash flow and operational sustainability.

- Risk of Manufacturing and Supply Chain Disruptions: The SynCardia TAH production relies on specialized, handcrafted processes requiring highly skilled technicians, posing risks of delays from personnel shortages, equipment failures, or regulatory non-compliance with FDA Quality System Regulations. Dependence on single-source suppliers for critical components, such as SynHall Valves and driver elements, exposes the company to supply interruptions, quality variances, or prioritization issues from vendors. Inability to secure alternative suppliers promptly, coupled with potential production scale-up failures or facility disruptions (e.g., from natural disasters or public health events), could result in reduced output, delayed deliveries, recalls, or regulatory actions, severely impacting revenue and market competitiveness.

Conclusion

Picard Medical, Inc. (PMI) stands as a fundamentally decent enterprise in the medical technology sector, dedicated to advancing life-saving solutions for heart failure patients through its wholly owned subsidiary, SynCardia Systems, LLC. As the exclusive manufacturer of the FDA- and Health Canada-approved SynCardia Total Artificial Heart (TAH)—the only implantable total artificial heart available, with over 2,100 units deployed across 27 countries to bridge biventricular failure patients to transplantation—PMI addresses a profound global health challenge affecting 56.2 million individuals and contributing to nearly 18 million annual deaths, amid severe donor shortages that restrict transplants to around 8,200 worldwide each year. The company's principled approach is evident in its roadmap, which prioritizes ethical innovation by refining driver technology, extending indications to bridge-to-candidacy and long-term use, and pursuing the fully implantable Emperor TAH (with prototypes in testing, animal studies planned for early 2025, and potential FDA approval by 2028), all while fostering responsible global expansion in markets like China, India, and the Middle East through strategic partnerships and regulatory diligence. By allocating IPO proceeds thoughtfully to research and development (USD 3.36 million), sales and marketing enhancements (USD 0.50 million), operational needs, and debt management (USD 7.6 million), PMI upholds strong intellectual property, clinical integrity, and a commitment to sustainable progress, positioning it as a reliable contributor to improving outcomes in the mechanical circulatory support field against alternatives like LVADs and emerging competitors.

Hence, given the financial performance of the company, use of proceeds, and associated risks “Picard Medical Inc (PMI)” IPO seems “Attractive" at the IPO price.

Disclaimer-

This report (“Report”) has been issued by Kalkine Pty Limited (ABN 34 154 808 312) (Australian financial services licence number 425376) (“Kalkine”) and prepared by Kalkine and its related bodies corporate who are authorised to provide general financial product advice. Kalkine.com.au and its associated pages are published by Kalkine.

Any advice provided in this Report is general advice only and does not take into account your objectives, financial situation or needs. You should therefore consider whether the advice is appropriate for your objectives, financial situation and needs before acting upon it.

There may be a Product Disclosure Statement, Information Memorandum or other offer document (“Offer Document”) for the securities or other financial products referred in this Report. You should obtain a copy of the relevant Offer Document and consider it before making any decision about whether to acquire the security or financial product.

Kalkine strongly recommends that you seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) before acting on any of the general advice in this Report or on the Kalkine website. Not all investments are appropriate for all people.

The information in this Report and on the Kalkine website has been prepared from a wide variety of sources, which Kalkine, to the best of its knowledge and belief, considers accurate. Kalkine has made every effort to ensure the reliability of the information contained in its reports (including this Report), newsletters and websites. All information represents our views at the date of publication and may change without notice.

The information in this Report does not constitute an offer to sell securities or other financial products or a solicitation of an offer to buy securities or other financial products. Our reports contain general recommendations to invest in securities and other financial products. Kalkine is not responsible for, and does not guarantee, the performance of, or returns on, any investments mentioned in this Report.

Kalkine does not issue, sell or deal in any financial products.

This Report may contain information on past performance of particular investments. Past performance is not a reliable indicator of future performance. Returns stated do not take into account transaction costs and taxes. To the extent permitted by law, and excluding any dishonesty or gross negligence by Kalkine, Kalkine disclaims and excludes all liability for any direct, indirect, implied, punitive, special, incidental or other consequential loss or damage arising from the use of or reliance on this Report, the Kalkine website and any information published on the Kalkine website without any warranties or representations by Kalkine to you. To the extent the law prohibits or limits this exclusion, Kalkine limits its liability to the resupply of services.

Please also read our Terms & Conditions and Financial Services Guide for further information. Employees and/or associates of Kalkine and its related entities may hold interests in the securities or other financial products covered in this Report or on the Kalkine website. Any such employees and associates are required to comply with certain, procedures and disclosures as required by law.

Kalkine Media Pty Ltd, an affiliate of Kalkine Pty Ltd, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website including entities covered in this Report.

Copyright 2025 Krish Capital Pty. Ltd. (ABN 61629651510). All Rights Reserved. No part of this report, or its content, may be reproduced in any form without our prior consent.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...