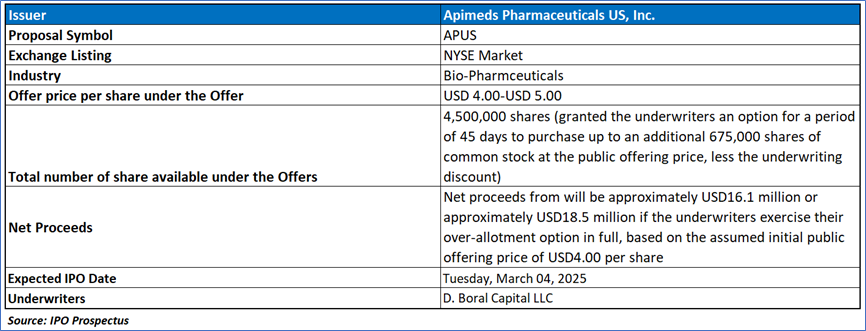

The Offer

Company Overview

Apimeds US, a clinical-stage biopharmaceutical company, is advancing Apitox, a bee venom-based therapy derived from Apis mellifera, targeting inflammation and pain management for knee osteoarthritis (OA) and, to a lesser extent, multiple sclerosis (MS), leveraging clinical data from Apimeds Korea’s Apitoxin, approved in South Korea since 2003 for OA pain and mobility with no serious adverse events in a 2003–2009 post-marketing study. Following Apimeds Korea’s completion of Phase I, II, and III trials for OA, and a U.S. Phase III trial in 2018 involving 330 patients that showed therapeutic benefits but fell short of FDA approval due to a small sample size and data handling issues, Apimeds US is preparing a second Phase III trial to meet FDA standards, focusing on advanced knee OA patients (grades 2–4) to demonstrate efficacy. The Company remains optimistic about Apitox’s potential as an innovative treatment, supported by prior clinical results, and plans to extend its research to explore applications for MS, capitalizing on its proprietary venom processing and historical use in Asia and Europe for pain relief.

Key Highlights

Primary Offering:

4,500,000 shares (granted the underwriters an option for a period of 45 days to purchase up to an additional 675,000 shares of common stock at the public offering price, less the underwriting discount).

Use of proceeds:

- Estimated Net Proceeds: The company anticipates receiving approximately USD 16.1 million in net proceeds from this offering, assuming an initial public offering price of USD 4.00 per share. If underwriters fully exercise their option to purchase additional shares, the net proceeds are estimated to reach approximately USD 18.5 million. These estimates are calculated after deducting underwriting discounts, commissions, and other offering expenses payable by the company.

- Purpose of the Offering: The primary objective of the offering is to fund clinical trials, enhance capitalization, and improve financial flexibility. Additionally, the offer aims to create a public market for common stock, facilitate future access to public equity markets, and enhance the company's visibility in the marketplace.

- Intended Use of Proceeds: The company plans to allocate the net proceeds, along with existing cash reserves, to finance its Phase III clinical trial in knee osteoarthritis (OA), initiate at least one non-registered corporate-sponsored study in multiple sclerosis (MS), cover manufacturing expenses, and support general corporate purposes. The expected allocation includes approximately USD 10.0 million for the Phase III knee OA trial, USD 1.5 million for the MS study, and USD 1.0 million for manufacturing. Additionally, around USD 0.3 million and USD 0.4 million will be used to repay two promissory notes to the majority stockholder, Inscobee, with 5% interest maturing in May and August 2025, respectively. The remaining funds will support working capital and general corporate expenses.

- Broad Discretion in Fund Utilization: The allocation of proceeds is based on the company’s current business plans and market conditions, which are subject to change. Due to the inherent uncertainties in product development, the exact usage of proceeds may vary. The company may also allocate a portion of the funds to strategic investments or acquisitions, although no agreements or commitments are in place at this time. Management will have broad discretion in utilizing the net proceeds, and investors will rely on their judgment regarding the application of the funds.

- Funding Timeline: Based on current projections, the net proceeds from this offering, combined with the company's existing cash, are expected to cover operating expenses and capital expenditure requirements for at least the next 12 months. The proceeds are anticipated to enable the completion of the Phase III knee OA trial, initiation of the MS study, manufacturing activities, and repayment of debt liabilities within the next 24 months.

- Additional Capital Requirements: If the net proceeds amount to less than USD 10 million, the company will prioritize the Phase III knee OA trial, regulatory and manufacturing costs, and internal operations. Under such circumstances, the company may require additional capital to complete product development. Future financing needs are expected to be met through public or private equity or debt financing, collaborations, strategic alliances, or licensing arrangements. Unutilized proceeds will be invested in short- and intermediate-term interest-bearing obligations, investment-grade instruments, certificates of deposit, or U.S. government-backed securities.

Dividend policy:

Apimeds US has never declared or paid cash dividends on its capital stock and currently intends to retain all available funds and any future earnings to support the development and expansion of its business, with no plans to pay cash dividends in the foreseeable future. Any future decisions regarding dividend payments will be determined by the board of directors, taking into account the company’s financial condition, operating results, contractual obligations, capital needs, business prospects, and other relevant factors, while potential future agreements may impose restrictions on dividend payouts.

Strategic Development and Market Potential of Apitox by Apimeds US:

- Market Opportunity and Strategic Focus: Apimeds US recognizes a substantial and growing market opportunity for its product candidate, Apitox, in the United States for addressing the symptoms of knee osteoarthritis (OA) and, in the longer term, multiple sclerosis (MS), driven by the significant prevalence and economic burden of these chronic conditions. According to Precedence Research, the osteoarthritis therapeutics market, valued at USD 8.28 billion in 2022, is projected to expand dramatically to USD 20.24 billion by 2032, achieving a compound annual growth rate (CAGR) of 9.4% from 2023 to 2032, reflecting the increasing demand for effective treatments as OA, particularly affecting joints like knees, hips, and spines, causes persistent pain and mobility issues. Similarly, Pharmaceutical Technology reports that the U.S. MS market, valued at USD 10.73 billion in 2022, is projected to grow to USD 24.4 billion by 2030, with a CAGR of 10.32%, underscoring the need for innovative therapies to manage MS symptoms. This dual focus aims not only to address the debilitating symptoms of these diseases but also to enhance overall patient well-being, positioning Apitox as a transformative solution in these expanding therapeutic markets.

- Therapeutic Potential of Apitox: Apitox, a purified venom from the western honeybee (Apis mellifera), is formulated as a lyophilized powder reconstituted in 0.5% preservative-free lidocaine for intradermal injections, containing key biologically active components such as melittin (40-50%), apamin (2-3%), mast cell degranulating peptide (2-3%), phospholipase A2 (10-15%), hyaluronidase (1.5-2%), and trace elements like dopamine and norepinephrine. Scientific studies, including Shi et al.’s “Pharmacological effects and mechanisms of bee venom and its main components: Recent progress and perspective,” highlight Apitox’s potential anti-inflammatory and analgesic properties, attributed to components like Peptide 401 and adolapin, which inhibit prostaglandin synthesis. Additionally, Bava et al.’s “Therapeutic Use of Bee Venom and Potential Applications in Veterinary Medicine” suggests that Apitox’s immune-modulating effects, potentially mediated by phospholipase A2 and regulatory T cells, could mitigate immune-inflammatory responses in MS, positioning it as a promising add-on therapy for relapsing-remitting, primary-progressive, and secondary-progressive MS patients.

- Clinical Rationale and Quality of Life Improvement: Apimeds US posits that living with chronic conditions such as knee OA and MS presents profound challenges, including physical limitations, mental health struggles, and social isolation, all of which significantly diminish patients’ quality of life. The Company’s approach with Apitox centers on reducing these symptoms—particularly inflammation and pain—thereby enhancing patients’ overall well-being, leveraging bee venom’s demonstrated ability to suppress key inflammatory cytokines like interleukin-6, IL-8, interferon-γ, and tumor necrosis factor-α. For knee OA, especially in advanced stages, Apitox’s potential to target key inflammatory drivers could reduce reliance on narcotics, offering a novel treatment option, while its application to MS aims to address similar inflammatory and mobility challenges.

- Development Strategy and Market Positioning: Apimeds US is strategically building on the extensive clinical foundation established by Apimeds Korea, where Apitoxin, a comparable bee venom product, completed Phase I, II, and III trials for OA by 2003, leading to its approval by the Korean Ministry of Food and Drug Safety for treating pain and mobility issues. In the U.S., following a Phase III trial for knee OA in 2018 that showed therapeutic benefits but failed to meet FDA standards, Apimeds US is now designing and implementing a second Phase III trial specifically targeting advanced knee OA patients (grades 2–4) to address FDA requirements. For MS, the Company plans to launch non-registered corporate sponsorship studies in Q1 2025 to explore Apitox’s potential, positioning it as an innovative therapy to meet unmet needs in both the OA and MS markets, which are expected to grow significantly.

Financial Highlights (Results of Operations) (Expressed in USD)

- Financial Performance Overview for Apimeds US (Nine Months Ended September 30, 2024): Apimeds US reported no revenue for the nine months ended September 30, 2024, consistent with the same period in 2023, as the Company remains in the clinical development phase without commercial operations. Research and development expenses decreased significantly to USD 0 from USD 69,993 in 2023, a reduction of USD 69,993, primarily due to lower payroll costs, reflecting a strategic shift or pause in certain development activities. Conversely, general and administrative expenses surged to USD 999,482 from USD 118,372, an increase of USD 881,110, driven predominantly by elevated professional service costs of approximately USD 603,767 and higher salaries and wages for several officers, totaling USD 297,000, as the Company prepares for key regulatory and pre-IPO milestones.

- Other Financial Metrics and Net Loss Analysis: For the nine months ended September 30, 2024, Apimeds US recorded other expenses of USD 78,875, up from USD 22,363 in 2023, an increase of USD 56,512, largely due to accretion expenses of USD 55,101 related to notes payable, which began accruing at the end of 2023. This resulted in a net loss of USD 1,078,357 for 2024, compared to USD 210,728 in 2023, marking an increase of USD 867,629, primarily attributable to the sharp rise in general and administrative expenses, including payroll and professional fees associated with the S-1 filing and pre-IPO preparations. As of September 30, 2024, the Company held cash reserves of USD 26,571, and management believes the anticipated net proceeds from its offering, combined with existing cash, will fund operating expenses and capital needs for the next 12 months, though this estimate relies on assumptions that may change, potentially necessitating additional capital for advancing Apitox, seeking regulatory approval, and exploring in-licenses or acquisitions.

- Cash Flow from Operating Activities: Cash utilized in operating activities amounted to USD 633,910 for the nine months ended September 30, 2024, comprising a net loss of USD 1,078,357, partially offset by non-cash interest expense from related parties of USD 26,568, accretion expense of USD 55,101, and a net increase of USD 362,778 in operating assets and liabilities. In comparison, cash used in operating activities for the same period in 2023 was USD 287,217, driven by a net loss of USD 210,728, mitigated by stock-based compensation expense of USD 69,994, non-cash interest expense from related parties of USD 16,500, and a net increase of USD 162,983 in operating assets and liabilities. This increase in cash usage in 2024 reflects heightened operational expenditures, particularly in preparation for clinical and regulatory advancements, despite the absence of research and development costs.

- Financing Activities and Capital Position: Cash inflows from financing activities totaled USD 250,000 for the nine months ended September 30, 2024, entirely derived from proceeds of USD 250,000 through notes payable to related parties, bolstering the Company’s liquidity to support ongoing operations. In contrast, cash provided by financing activities in 2023 amounted to USD 1,032,100, comprising USD 500,000 in cash advances for obligations to issue common shares, USD 500,000 from issuing common stock, and USD 64,000 from related party advances, offset by USD 31,900 in repayments to related parties. This shift in financing activities highlights a more conservative approach in 2024, relying on debt financing to sustain operations, as Apimeds US positions itself for future growth and regulatory milestones in developing Apitox for knee OA and MS.

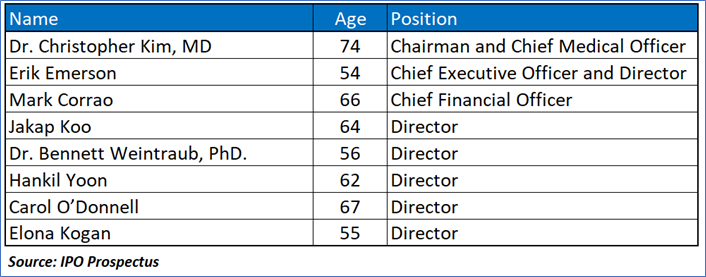

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “APUS” is exposed to a variety of risks such as:

- Financial Instability and Capital Requirements: Apimeds US faces significant financial risk due to its early-stage status, lack of revenue, and net losses of USD 1,078,357 in 2024 and USD 210,728 in 2023, with an accumulated deficit of USD 4,080,291 and only USD 26,571 in cash as of September 2024. Its need for substantial additional funding to advance Apitox through late-stage trials and FDA approval is jeopardized by potential economic or market disruptions, risking delays or termination of development if capital cannot be raised.

- Dependence on Apimeds Korea and Potential Conflicts of Interest: Apimeds US’s heavy reliance on its license with Apimeds Korea for Apitox data poses a major risk, as termination of the agreement due to default could halt development and harm prospects. Conflicts of interest among shared directors and officers, like Dr. Christopher Kim and Mr. Jakap Koo, may disrupt collaboration and commercial success, despite awareness of fiduciary duties, potentially leading to misaligned priorities or disputes.

- Regulatory and Clinical Development Challenges: Apimeds US risks delays or failure in obtaining FDA approval for Apitox due to its limited experience with pivotal trials, the complexity of the regulatory process, and Apitox’s novel bee venom-based nature, which could increase costs and timelines. Reliance on third parties and external disruptions, such as government shutdowns or health crises, further heightens the risk of execution failures, potentially preventing commercial viability if not managed effectively.

Conclusion

Apimeds US, a clinical-stage biopharmaceutical company, is advancing Apitox, a bee venom-based therapy derived from Apis mellifera, to address knee osteoarthritis (OA) and potentially multiple sclerosis (MS). The company aims to leverage previous clinical data from Apimeds Korea, where Apitoxin received regulatory approval in South Korea. Apimeds US is planning a second Phase III trial to meet FDA standards, focusing on advanced knee OA patients. The IPO proceeds, estimated at USD 16.1 million, will primarily fund the Phase III trial, MS studies, manufacturing expenses, debt repayment, and general corporate purposes. The company holds broad discretion in fund utilization, which may include strategic investments. Apimeds US faces significant risks due to its early-stage nature, lack of revenue, heavy reliance on Apimeds Korea, regulatory hurdles, and the necessity for substantial additional funding. The market potential for OA and MS treatments presents opportunities for Apitox, but the company's financial instability, dependency on key partnerships, and regulatory uncertainties pose considerable investment risks.

Hence, given the financial performance of the company, use of proceeds, and associated risks “Apimeds Pharmaceuticals US, Inc. (APUS)” IPO seems “Neutral" at the IPO price.

Disclaimer-

This report has been issued by Kalkine Pty Limited (ABN 34 154 808 312) (Australian financial services licence number 425376) (“Kalkine”) and prepared by Kalkine and its related bodies corporate authorised to provide general financial product advice. Kalkine.com.au and associated pages are published by Kalkine.

Any advice provided in this report is general advice only and does not take into account your objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your objectives, financial situation and needs before acting upon it.

There may be a Product Disclosure Statement, Information Statement or other offer document for the securities or other financial products referred to in Kalkine reports. You should obtain a copy of the relevant Product Disclosure Statement, Information Statement or offer document and consider the statement or document before making any decision about whether to acquire the security or product.

Choosing an investment is an important decision. If you do not feel confident making a decision based on the recommendations Kalkine has made in our reports, you should consider seeking advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) before acting on any advice in this report or on the Kalkine website. Not all investments are appropriate for all people.

The information in this report and on the Kalkine website has been prepared from a wide variety of sources, which Kalkine, to the best of its knowledge and belief, considers accurate. Kalkine has made every effort to ensure the reliability of information contained in its reports, newsletters and websites. All information represents our views at the date of publication and may change without notice. The information in this report does not constitute an offer to sell securities or other financial products or a solicitation of an offer to buy securities or other financial products. Our reports contain general recommendations to invest in securities and other financial products.

Kalkine is not responsible for, and does not guarantee, the performance of the investments mentioned in this report This report may contain information on past performance of particular investments. Past performance is not an indicator of future performance. Hypothetical returns may not reflect actual performance. Any displays of potential investment opportunities are for sample purposes only and may not actually be available to investors. To the extent permitted by law, Kalkine excludes all liability for any loss or damage arising from the use of this report, the Kalkine website and any information published on the Kalkine website (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine hereby limits its liability, to the extent permitted by law, to the resupply of services..

Please also read our Terms & Conditions and Financial Services Guide for further information. Employees and/or associates of Kalkine and its related entities may hold interests in the securities or other financial products covered in this report or on the Kalkine website. Any such employees and associates are required to comply with certain safeguards, procedures and disclosures as required by law.

Kalkine Media Pty Ltd, an affiliate of Kalkine Pty Ltd, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website including entities covered in this Report.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...