The Offer

_09_02_2025_19_26_32_591462.png)

Company Overview

FG Holdings Ltd (FGO), operating through its subsidiaries, is a prominent financial services provider in Hong Kong, specializing in private credit and bank mortgage loan brokerage services facilitated by a pioneering fintech platform that connects borrowers and lenders with a secure, bilingual, and user-friendly interface featuring automated assessment simulations. The company distinguishes itself as an early innovator in the mortgage brokerage sector by offering tailored loan matching and comprehensive support to enhance borrower-lender interactions, leveraging its extensive lender network and industry expertise, which has earned accolades such as the “Hong Kong’s Most Outstanding Business Award” by Corphub in 2020 and the “Startup” award in Fintech 2021 by HK01 and ICON. Beyond brokerage, FGHL provides consultancy services through its Fundergo brand, assisting corporate clients with debt restructuring and financing options using the same experienced team, targeting past borrowers and new referrals from banking, financing, and real estate networks, while actively promoting its services at industry conferences to attract new clientele.

Key Highlights

Primary Offering:

2,000,000 Class A Ordinary Shares (underwriters the right to purchase up to an additional 15% of the total number of Class A Ordinary Shares within 45 days after closing of offer)

Use of proceeds:

- Allocation of Net Proceeds from Initial Public Offering: FG Holdings Ltd anticipates receiving net proceeds of approximately USD 7,089,130 from its initial public offering, based on an assumed initial public offering price of USD 4.50 per Class A Ordinary Share (the midpoint of the price range outlined in the prospectus), with an increase to USD 8,331,130 should the underwriters fully exercise their over-allotment option, after accounting for underwriting discounts, non-accountable expense allowances, and estimated offering expenses. Each USD 1.00 adjustment in the assumed offering price would alter the net proceeds by USD 1,840,000, while a variation of 1.0 million in the number of shares offered would adjust the proceeds by USD 4,140,000, assuming all other factors remain constant. These estimates reflect the company’s strategic intent to establish a public market for its Class A Ordinary Shares, benefiting all shareholders.

- Intended Utilization of Proceeds: The company intends to allocate the net proceeds with approximately 30% directed toward acquisitions of companies and/or formation of joint ventures within the financial services industry value chain, 20% toward developing new products and diversifying service offerings, 10% for business expansion into overseas markets including the UK, US, and Canada, 10% for investment in IT infrastructure and optimization of its online platform, and the remaining 30% for working capital and general corporate purposes. This allocation is subject to the discretion of management, which retains flexibility to adapt the use of funds based on evolving business conditions or unforeseen events, though no specific acquisition targets or commitments have been identified as of the prospectus date. Any unutilized proceeds will be prudently invested in short-term, interest-bearing bank deposits or debt instruments to ensure liquidity.

- Flexibility and Contingency Planning: Given the dynamic nature of business operations, FG Holdings Ltd reserves the right to reallocate the net proceeds from this offering should circumstances necessitate a deviation from the outlined plans, reflecting a proactive approach to strategic adaptability. As of the prospectus date, the absence of formal agreements or identified acquisition targets underscores the preliminary nature of these intentions, allowing management to respond effectively to market opportunities or challenges. This strategic flexibility, combined with a robust net cash position, positions the company to optimize its financial resources for long-term growth and shareholder value creation.

Dividend policy:

FG Holdings Ltd currently intends to retain all available funds and future earnings to support its business operations and expansion, with no plans to declare or pay dividends in the foreseeable future, a decision subject to the discretion of its board of directors based on financial condition, operational results, capital needs, and other relevant factors. Since its inception, the company has not declared or paid any dividends, relying instead on dividend payments from its subsidiaries to meet cash requirements, including potential future dividends, debt servicing, and operating expenses, with any future distributions contingent upon the subsidiaries’ ability to satisfy the BVI solvency test ensuring assets exceed liabilities and debts can be met as they fall due. Cash dividends, if approved, will be paid in U.S. dollars and are not subject to tax in Hong Kong under current Inland Revenue Department practices, though the board retains flexibility to adjust this policy in response to evolving business conditions and regulatory constraints.

Industry Overview and Data Reliability

- Mortgage Lending Landscape in Hong Kong: Hong Kong’s real estate market, recognized as one of the world’s most expensive and liquid due to limited land supply, high demand, and cultural factors, significantly bolsters the city’s economy, with 67,979 property sale agreements totaling approximately HKD 534.1 billion in 2024 according to the Land Registry. The mortgage lending sector, a vital component of this market, has thrived over the past decade as a preferred lending product secured by fixed assets, driven by property transactions and refinancing needs, with total residential mortgage loans from authorized banking institutions reaching HKD 1.87 trillion by December 2024, supported by a low delinquency ratio of 0.11% as reported by the Hong Kong Monetary Authority (HKMA). Recent adjustments, including a 100-basis-point reduction in the HKMA Base Rate to 4.75% by December 19, 2024, following U.S. Federal Reserve rate cuts, along with relaxed loan-to-value ratios (e.g., 70% for first-time buyers and non-residential properties), have enhanced market liquidity and affordability, despite challenges from interest rate hikes and COVID-19-related downturns.

- Evolution of Automated Mortgage Platforms: The mortgage lending industry in Hong Kong has undergone significant digital transformation, with providers like FG Holdings adopting automated online platforms to streamline processes, featuring loan approval estimations, mortgage comparisons, online property valuations, and repayment calculators. This technological advancement enhances accessibility and transparency, positively influencing market efficiency by catering to the diverse financing needs of residential, commercial, and industrial properties, which collectively sustain strong demand despite high property prices. The market is dominated by banks offering regulated, competitive products and private credit lenders providing flexible alternatives, though the sector faces intensified competition and entry barriers including lender relationships, reputation building, market expertise, and the need for substantial marketing to establish a foothold.

- Market Dynamics and Growth Drivers: The mortgage lending business in Hong Kong is shaped by key market drivers, including property prices that have declined 20-25% over three years yet remain expensive, with potential recovery anticipated from expected interest rate reductions, improved affordability due to rising incomes, and enhanced rental yields. The increase in interbank rates from 0.75% to 5.75% since 2022, tied to the U.S. Federal Reserve’s rate hikes, has shifted some demand toward private credit for refinancing, while stable employment at a 3.1% unemployment rate and anticipated salary increases in 2025, per HAYS data, support borrower repayment capacity. Government regulations, including relaxed loan-to-value ratios and the suspension of interest rate stress testing, further stimulate market activity, positioning the industry for growth as property lending, comprising 78% of domestic loans at HKD 3.4 trillion by Q2 2024, continues to play a pivotal role.

Financial Highlights (Results of Operations) (Expressed in USD)

- Revenue Performance Analysis: FG Holdings Ltd reported a total revenue of HK$6,913,403 for the six months ended December 31, 2023, which declined by 9.3% to HK$6,272,928 (USD 807,566) for the same period in 2024, primarily due to a significant reduction in private credit mortgage loan brokerage services revenue by 87.7% to HK$148,769 (USD 19,153) and bank mortgage loan brokerage services revenue by 84.7% to HK$89,759 (USD 11,555), reflecting cautious lending amid volatile property prices. This downturn was partially mitigated by a 17.9% increase in consultancy services revenue to HK$6,034,400 (USD 776,858), indicating a strategic pivot to capitalize on growing demand for consultancy amid a challenging mortgage market. The revenue shift highlights the company’s adaptability, though the overall decline underscores sensitivity to market volatility and lender caution in Hong Kong’s property sector.

- Expenditure and Operational Cost Trends: IT development expenses rose by 25.7% to HK$357,137 (USD 45,977) for the six months ended December 31, 2024, from HK$284,080 in 2023, driven by higher staff salaries, reflecting investments in technological capabilities. Selling and marketing expenses increased by 87.1% to HK$1,981,073 (USD 255,040), with staff costs surging 135.7% to HK$1,773,611 (USD 228,332) due to expanded headcount and bonuses, though agency fees dropped 96.6% to HK$5,600 (USD 721) in line with reduced brokerage activity. General and administrative expenses decreased 32.0% to HK$2,849,303 (USD 366,813), primarily due to a 79.2% reduction in legal and professional fees to HK$440,203 (USD 56,671) post-IPO preparation, despite rises in office sundries (39.5%) and business development costs (60.3%), indicating a focus on operational efficiency amidst strategic growth initiatives.

- Liquidity and Cash Flow Assessment: The company’s cash position strengthened, with cash and cash equivalents increasing from HK$8,839,336 as of June 30, 2023, to HK$19,250,976 (USD 2,478,337) as of December 31, 2024, supported by net cash provided by operating activities of HK$3,640,812 (USD 468,712) in the latter half of 2024, driven by net income and receivable settlements. Net cash used in investing activities was minimal at HK$38,118 (USD 4,907) for the same period, reflecting equipment purchases, while net cash used in financing activities was HK$566,067 (USD 72,875), primarily from bank loan repayments and deferred offering costs. FG Holdings Ltd asserts that its current cash reserves and operational cash flows will adequately meet its needs for the next twelve months, bolstered by a net cash position of HK$155.1 billion (USD 21.66 billion) as of June 30, 2025, despite negative free cash flow of HK$4.7 billion (USD 653 million) due to AI business investments.

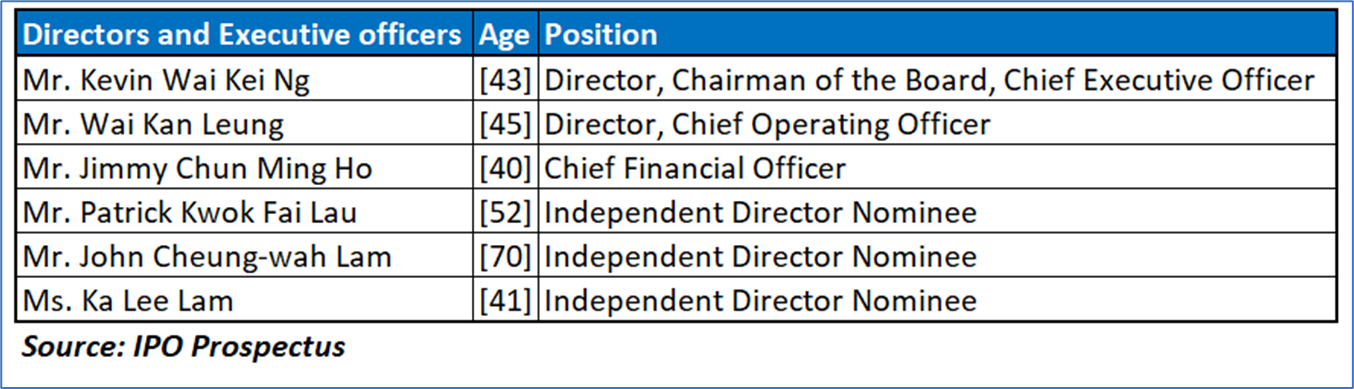

Key Management Highlights

Risk Associated (High)

Investment in the IPO of “FGO” is exposed to a variety of risks such as:

- Risks Associated with Corporate Structure: FG Holdings Ltd (FGHL), as a holding company incorporated in the British Virgin Islands (BVI), depends on dividends and equity distributions from its subsidiaries to meet its cash and financing needs, including potential shareholder dividends and debt obligations, which could be materially disrupted if subsidiaries incur debt with restrictive covenants or fail to satisfy the BVI solvency test requiring assets to exceed liabilities and debts to be payable as they fall due. The Hong Kong Companies Ordinance further limits dividends to distributable profits or reserves, excluding share capital, though no restrictions exist on currency conversion, remittance, or dividend distribution to U.S. investors under current Hong Kong practices, which are tax-exempt. Any constraints on subsidiary payments could hinder FGHL’s growth, investment opportunities, and operational funding, exacerbated by identified material weaknesses in internal controls over financial reporting—such as inadequate segregation of duties and lack of independent directors—posing risks of financial misstatements that may erode investor confidence and affect the market price of its Class A Ordinary Shares.

- Risks Pertaining to Operations in Hong Kong: Operating exclusively through subsidiaries in Hong Kong, FGHL faces potential oversight from the People’s Republic of China (PRC) government due to long-arm provisions in PRC laws, which could lead to rapid regulatory changes with little notice, impacting business operations and the value of its Class A Ordinary Shares. Although currently unaffected by PRC statements on increased oversight of overseas listings, the evolving regulatory landscape, including cybersecurity and anti-monopoly measures, introduces uncertainties regarding compliance costs, operational delays, or penalties that could necessitate restructuring or cessation of activities. The absence of current PRC operations mitigates immediate risks under the Revised Review Measures or Trial Administrative Measures, but future expansion into Mainland China could trigger cybersecurity reviews or CSRC filings, potentially restricting offerings or delisting shares if approvals are not secured.

- Risks Related to Regulatory and Audit Compliance: FG Holdings Ltd is subject to emerging U.S. regulatory scrutiny under the Holding Foreign Companies Accountable Act (HFCAA) and its amendments, including the Accelerating Holding Foreign Companies Accountable Act (AHFCAA), which mandate PCAOB inspection of auditors and could prohibit trading of Class A Ordinary Shares on U.S. exchanges if inspections are impeded for two consecutive years, potentially leading to delisting and significant share price declines. While the company’s current U.S.-based auditor, WWC, P.C., is PCAOB-inspected and no PRC operations exist, political shifts between Mainland China and Hong Kong could alter audit accessibility, and any future work papers located in China might evade PCAOB review, heightening delisting risks. Recent U.S. legislative proposals and SEC rule changes add further uncertainty, potentially imposing stringent disclosure requirements or delisting triggers, which could impair capital raising and negatively impact business prospects and shareholder value.

Conclusion

FG Holdings Ltd (FGHL), a Hong Kong-based financial services provider, is launching an initial public offering (IPO) of 2,000,000 Class A Ordinary Shares, with underwriters able to purchase up to an additional 15% within 45 days post-closing, expecting net proceeds of approximately USD 7,089,130 at an assumed price of USD 4.50 per share (midpoint of the prospectus range), potentially increasing to USD 8,331,130 if the over-allotment option is fully exercised. The company plans to allocate 30% of proceeds to acquisitions or joint ventures in the financial services sector, 20% to new product development, 10% to overseas expansion into markets like the UK, US, and Canada, 10% to IT enhancements, and 30% to working capital, though management retains flexibility to adjust based on business conditions, with no specific targets identified as of the prospectus date. Financially, revenue declined 9.3% to HK$6,272,928 (USD 807,566) for the six months ended December 31, 2024, from HK$6,913,403 in 2023, due to an 87.7% drop in private credit mortgage loan brokerage revenue amid volatile property prices, partially offset by a 17.9% rise in consultancy services to HK$6,034,400 (USD 776,858), while cash reserves grew to HK$19,250,976 (USD 2,478,337) by December 31, 2024, supported by a net cash position of HK$155.1 billion (USD 21.66 billion) as of June 30, 2025, despite negative free cash flow of HK$4.7 billion (USD 653 million) due to AI investments.

Hence, given the financial performance of the company, use of proceeds, and associated risks “FG Holdings Ltd (FGO)” IPO seems “Neutral" at the IPO price.

Disclaimer-

This report (“Report”) has been issued by Kalkine Pty Limited (ABN 34 154 808 312) (Australian financial services licence number 425376) (“Kalkine”) and prepared by Kalkine and its related bodies corporate who are authorised to provide general financial product advice. Kalkine.com.au and its associated pages are published by Kalkine.

Any advice provided in this Report is general advice only and does not take into account your objectives, financial situation or needs. You should therefore consider whether the advice is appropriate for your objectives, financial situation and needs before acting upon it.

There may be a Product Disclosure Statement, Information Memorandum or other offer document (“Offer Document”) for the securities or other financial products referred in this Report. You should obtain a copy of the relevant Offer Document and consider it before making any decision about whether to acquire the security or financial product.

Kalkine strongly recommends that you seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) before acting on any of the general advice in this Report or on the Kalkine website. Not all investments are appropriate for all people.

The information in this Report and on the Kalkine website has been prepared from a wide variety of sources, which Kalkine, to the best of its knowledge and belief, considers accurate. Kalkine has made every effort to ensure the reliability of the information contained in its reports (including this Report), newsletters and websites. All information represents our views at the date of publication and may change without notice.

The information in this Report does not constitute an offer to sell securities or other financial products or a solicitation of an offer to buy securities or other financial products. Our reports contain general recommendations to invest in securities and other financial products. Kalkine is not responsible for, and does not guarantee, the performance of, or returns on, any investments mentioned in this Report.

Kalkine does not issue, sell or deal in any financial products.

This Report may contain information on past performance of particular investments. Past performance is not a reliable indicator of future performance. Returns stated do not take into account transaction costs and taxes. To the extent permitted by law, and excluding any dishonesty or gross negligence by Kalkine, Kalkine disclaims and excludes all liability for any direct, indirect, implied, punitive, special, incidental or other consequential loss or damage arising from the use of or reliance on this Report, the Kalkine website and any information published on the Kalkine website without any warranties or representations by Kalkine to you. To the extent the law prohibits or limits this exclusion, Kalkine limits its liability to the resupply of services.

Please also read our Terms & Conditions and Financial Services Guide for further information. Employees and/or associates of Kalkine and its related entities may hold interests in the securities or other financial products covered in this Report or on the Kalkine website. Any such employees and associates are required to comply with certain, procedures and disclosures as required by law.

Kalkine Media Pty Ltd, an affiliate of Kalkine Pty Ltd, may have received, or be entitled to receive, financial consideration in connection with providing information about certain entity(s) covered on its website including entities covered in this Report.

Copyright 2025 Krish Capital Pty. Ltd. (ABN 61629651510). All Rights Reserved. No part of this report, or its content, may be reproduced in any form without our prior consent.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...