The company recently made an acquisition of a leading Australian automotive parts and accessories distribution, Metacash Automotive Holdings (MAH).

Burson distributes automotive parts to mechanic workshops in Australia. MAH is considered complimentary to the overall position of BAP in the supply chain – adding presence in wholesale, retail & service. The acquisition will increase the scale of BAP’s wholesale and distribution business, which is important for the competitive position of the company. MAH’s marketing network increases the addressable market for BAP’s distribution infrastructure and creates new growth opportunities for BAP. Acquisition is complementary to BAP’s current trade focus and BAP’s strategy for its Burson brande store network. The company has a target of 175 branded stores by June 2019. MAH customer facing functions will continue to operate separately. MAH is expected to accelerate BAP’s existing customer and product strategy.

Australian Automotive Aftermarket Parts Industry (Source - Company Reports)

Australian Automotive Aftermarket Parts Industry (Source - Company Reports)

The automotive market in Australia has historically grown at a rate equal to the population growth rate. This largely predictable and stable growth means that Burson can grow in times of healthy or challenging growth conditions. Burson is in a good position to grow revenue in its existing store network, as well as through the many opportunities to expand the number of stores via store acquisitions and greenfield developments. In the financial year 2014, the company showed growth across a number of parameters – store network growth of 10.5% to 116 stores, revenue growth of 11.5% and like for like sales growth of 3.9%. Gross margins of the company were up 0.8%. A key strategy of Burson is its growth of store network through both acquisitions and Greenfield expansion and MAH acquisition fits into that.

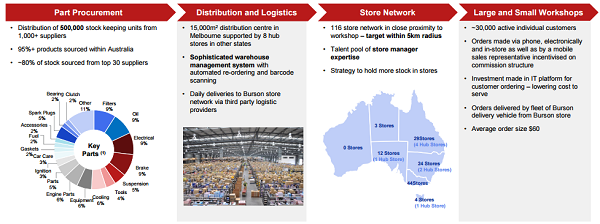

.png) Australia wide locations (Source - Company Reports)

Australia wide locations (Source - Company Reports)

This acquisition follows a series of acquisitions in 2014. The company expanded it’s store network in 2014, with the number of stores increasing from 105 to 116. The net increase in 11 stores was attributed to 8 acquisitions and 5 greenfield stores less 2 stores that were merged with existing stores. The location and set up of stores is designed to enable Burson to deliver the highest quality if service to its customers. The company now has stores across all of Australia except Western Australia and the Australian Capital territory. Approximately 80% of workshop customers are located within 5 kilometres of a Burson store. Such proximity to customers and density of customers around each store enables Burson to minimize time from receipt of order to delivery of parts and increase the frequency of delivery as more customers are located on a delivery route. Burson’s customers are primarily mechanic workshops. These workshops conduct general servicing and repairing of vehicles, with the large majority of servicing being conducted on the same day basis, whereby an owner will drop by the vehicle to the workshop and collect it on the same day. The mechanic needs to order and have the parts delivered within a short period of time to complete the servicing. The mechanic needs a distributor that holds both a wide range of parts suitable to the range of vehicles they service and offers a high level of customer service including, nearby availability of right parts, short delivery time and knowledgeable staff. Burson distributes over 500,000 stock keeping units to approximately 30,00 mechanic workshops across Australia.

Integrated distribution business model (Source - Company Reports)

Integrated distribution business model (Source - Company Reports)

The other two pillars of Bursons’s growth strategy are increasing existing store revenue and increasing existing store earnings. Burson is well placed to benefit from resilient demand for automotive aftermarket parts distribution while maintaining a high level of customer service through continued development of people and systems. Burson is focused on developing sales from electronics and other platforms, increasing walk-in’s store sales and chain workshop sales and further enhancing its inventory range. Burson is also positioned to increase its existing store earnings through a range of initiatives including improved supplier terms as purchasing volumes continue to increase, further developing Burson’s private label offering and developing direct sourcing relationship. Burson will continue to focus on continuous development of its store network through people and process development.

Burson Daily Chart (Source - Thomson Reuters)

Burson Daily Chart (Source - Thomson Reuters)

Over the period of 2013 to 2014, the company increased its revenues from 306 million to 341 million, which is an increase of 11.4 per cent. The company’s comprehensive income declined from 10.3 million to 1.1 million, which can be largely attributed to Initial Public Offering Cost of 9.7 million dollars. The company’s cash flow from operating declined from 32.2 million to 21.5 million over the same period.

The company is currently trading at a stock price of $3.400, which is somewhere close to the 52 week high of 3.6 and further from the 52 week low of 2.350. At the current price the company is trading at a Price to Earnings multiple of 51.2 and a dividend yield of 1.18%. Most of the companies in the sector are trading at a similar P/E ratio and yield.

The extremely high P/E ration will only be justified by very high growth in the company. While the growth numbers of Burson are steady, they do not justify such high P/E multiple. We believe that the company will grow at rate that is more or less in line with the overall population growth rate and increase in number of vehicles per person and the stock is expensive at the current price of $3.35.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...