Company Overview – Seven West Media was formed via West Australian Newspaper 2011 acquisition of Seven media group, joining a Western Australian newspaper business with the leading capital city free to air television network to deliver a platform to cross sell to advertisers. Earnings are derived from television (61%), newspapers (26%), magazines (8%) and online (5%). Key brands include Seven television network, The West Australian, Pacific Magazines and Yahoo 7.

ANALYSIS - The eminent multi-platform media business, Seven West Media (

ASX: SWM) entailing

Seven Television;

Pacific Magazines;

Yahoo!7 internet platform; and

The West Australian and other newspapers and radio stations, witnessed a positive twelve months in 2014. Amidst the pool of competitive media companies and challenging panorama full of technology developments and innovative new forms of content delivery tools coming-in every now and then, SWM managed to illustrate a strong balance sheet and is focused on reducing its debt.

SWM reported a statutory net profit of A$149.2 million for the year ended 28

th Jun 2014 as opposed to the previous corresponding year’s statutory net loss of A$69.8 million (including significant items). The Company’s revenue was A$1,861.8 million, down 1.1% from that of the previous year, and profit before significant items, net finance costs and tax (EBIT) of A$408.2 million, down 3.3% from that of the previous year.

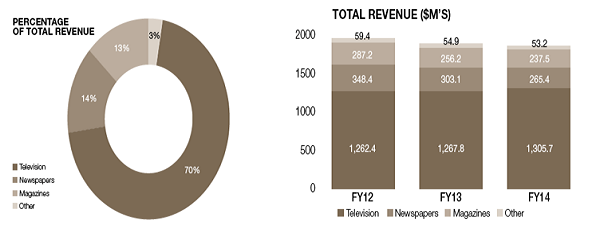

Percentage of Total Revenue and Total Revenue Figures (Source – Company Reports)

Percentage of Total Revenue and Total Revenue Figures (Source – Company Reports)

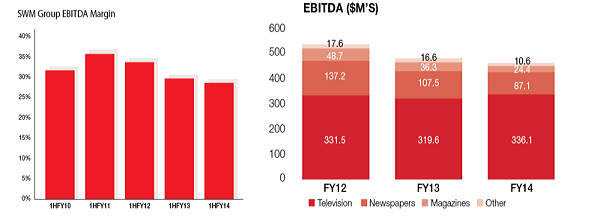

FY14 Net profit after tax (excluding significant items) was up 4.9% to A$236.2 million, and FY14 EBITDA was A$458.2m, down 4.6%.

SWM Group EBITDA Margin and EBITDA Figures (Source – Company Reports)

SWM Group EBITDA Margin and EBITDA Figures (Source – Company Reports)

SWM announced a fully franked final dividend of 6 cps, which will be paid in Oct 2014. The Company had net assets of A$2,897 million, and its net debt declined 6.6% to A$1,158.5 million compared to the previous year (A$1,240.8 million). SWM has continued to use its strong operating cash flows to pay down the debt. On 13

th Feb 2014, SWM finalized new two-pronged credit facilities totaling A$1.4 billion and used funds drawn from these facilities along with the available funds of A$100 million to repay all outstanding amounts. Total operating expenses reduced 0.4% to A$1,453.6 million.

Operating Costs’ Figures (Source – Company Reports)

Operating Costs’ Figures (Source – Company Reports)

As per the company’s Year End Results Announcement for financial year ended 28

th Jun 2014, SWM delivers profit growth, slightly ahead of guidance with

Television securing a record, market leading advertising revenue share of 40.5% and improved EBITDA growth of 12% in the second half; increased market share of the publishing business; and various cost reduction initiatives being undertaken for attaining and maintaining home market leadership.

SWM Daily Chart (Source - Thomson Reuters)

SWM Daily Chart (Source - Thomson Reuters)

From performance standpoint, SWM’s broadcast

Television segment is the cornerstone of the business. Television revenue grew 3% to A$1,306 million accounting for 70% of SWM’s revenue while EBIT increased 7.5% to A$312 million. It delivered EBITDA margin of 25.7% for the full year, with EBITDA increasing 12.4% on the corresponding prior period in the second half of the year. The Company declared to uncover more new plans, including Hybrid Broadband Broadcast Television, for video and publishing platforms.

The West Australian maintained the position of the strongest performing newspapers. While newspaper declines in print advertising continue, the Company continued to smash down its competitors from advertising and circulation activities. The newspaper revenue declined 12.4% to A$265.4 million while EBIT fell 23.9% to A$65.9 million.

Pacific Magazines’ revenue declined 7.3% to A$237.5 million compared to a 10.8% decline last year, with an improvement in the rate of decline. The company delivered a 4.3% decrease in costs to A$217.1 million, generating EBIT of A$20.4 million.

Yahoo7 continued its strong growth with more than 7.4 billion page views and video downloads growing at 25% year on year. The share of profit from

Yahoo7 increased 22% compared to the last financial year.

SWM also announced the formation of two new international production companies, 7Wonder and 7Beyond. It has also secured a number of additional tier-2 sports; and is investing in projects such as Big Data project.

Further, the Company gives an importance to owning and producing domestic content to mitigate issues related to piracy that tends to dilute the worth of any widely available content. Such content control capability allowed SWM to create and build an export business, which entails selling shows such as My Kitchen Rules (MKR) to Indonesia, House Rules into Russia etc. This also facilitated SWM to focus on compiling and providing sports content and has won the rights to air the Olympic Games until 2020 and the Gold Coast Commonwealth Games in 2018, thus bringing an edge over other competitors.

SWM will be running a single Perth desk, which will be used to generate content that will then flow online and into newspapers, and air on television. This may be seen as a practical initiative to counterbalance the dilution of returns from the traditional newspaper business.

It is also possible that the Company follows development offshore and seeks to monetize its content through partnership deals and the development of subscriber-based applications aimed at online TV platforms from Apple, Google and Microsoft. This look-out for M&A opportunities in the media industry may prove fruitful for SWM.

It is to be noted that SWM is the largest content company in Australia producing over 4,000 hours per annum of drama, entertainment, news and public affairs, giving the Company an edge over others in the market, while maintaining control of the production costs and increasing revenue through overseas content sales.

SWM’s Yahoo7 partnership with Yahoo! Inc. has helped the Company to build its audiences and delivering significant growth in mobile audiences. The Company has also dramatically expanded its PLUS7 catch-up TV offering that streams full episodes of SWM’s most popular programmes every month – with 250 hours of content each month, 7TWO and 7mate primetime programmes.

Unlike SWM’s competitors - Nine and Ten, which mostly rely on an outsourcing production model with the help of third-party companies; MKR's intellectual property rights are vested with SWM. This enables the Company to export the MKR show, or its format, to other international broadcasters, at the same time cross promoting MKR through its breakfast show, “Sunrise”. SWM thus appears to believe in creating, promoting, and controlling content, which may enable it to maximize return for advertisers.

Without losing the context here, it also prudent to wait and watch whether SWM will be interested in demerging/ spinning-off its

Print media business as its overall growth rates in earnings are pulled down by said business segment. This has come under speculation in the last 12 months, and is to be watched in view of similar strategy being recently adopted by three of SWM’s most comparable US media companies (Gannett, Tribune and E.W. Scripps). Of course, such a decision pivots at the edge of the possible pros & cons of a suitable business strategy.

Coming back to SWM’s

Television business, Metro TV ad markets remain under pressure with 1Q15 expected to be down 5-10%. Additionally, structural revenue pressures remain at both WAN and Pacific Magazines with FY15 guidance that indicate further revenue declines. In such case, Nine entertainment Co. (NEC) with no print exposure and a stronger balance sheet (1.7x net debt to EBITDA) may appeal to some, although prospects may look uncertain.SWM’s cost guidance for Consumer Price Index growth may also appear little disappointing.

Metro FTA TV Ad Revenue Market Share (Source – Company Reports)

Metro FTA TV Ad Revenue Market Share (Source – Company Reports)

Nevertheless, the FY14 result for the Company was broadly in line with set expectations. The print advertising and circulation trends have been feeble but were partially equalized by share performance for the ‘

Television’ business

. As per the Advertising Market Outlook

, for

Television, there will be low single digit growth; the current trend would continue for

Newspapers and the rate of decline is expected to lessen for the

Magazines. SWM indicates increasing its operating costs in FY15 at a similar rate to inflation as it continues to reinvest to produce content that can be accessed via a variety of different media platforms.

Also, the reduced EBITDA forecasts are partially offset by reduced interest and tax expense. Further, there is a good chance that the interest charges drop following the recent re-financing completed by the Company and the lower overall debt balance. No doubt that SWM has a lot of challenges ahead, however, the Company appears to be highly cash generative with a diluted free cash yield of ~10%, which is indeed spectacular.

Let’s also not forget that SWM has a portfolio of brawny and stable media assets, and its earnings may rebound strongly if there is a sustained recovery in advertising markets. Moreover, trading of the stock on low multiples appears to bring multifarious opportunities for investors with a long-term focus.

We thus put a BUY recommendation on the stock at the current price of $1.655.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...