Kalkine has a fully transformed New Avatar.

Company Overview: Service Stream Limited is a provider of essential network services, including access, design, build, installation and maintenance across copper, fiber and wireless telecommunications networks, as well as to private and public energy, and water entities. The Company's segments include Fixed Communications, Mobile Communications, and Energy & Water. The Fixed Communications segment provides design, construction, maintenance and customer connection services to the owners of telecommunications network infrastructure in connection with the roll-out of the National Broadband Network in Australia. The Mobile Communications segment provides program management and turnkey services for infrastructure projects in the telecommunications sector. The Energy & Water segment provides a range of metering and energy services to electricity, gas and water networks, and through the Customer Care business provides contact center services and workforce management support for contracts.

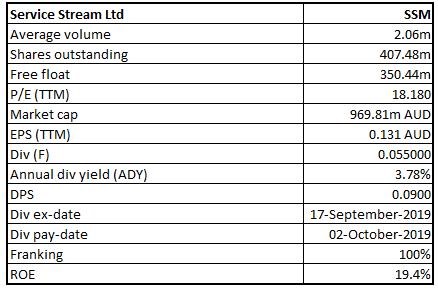

SSM Details

Growth Trajectory in Dividends Continues: Service Stream Limited (ASX: SSM) is a provider of essential network services to the telecommunications and utility sectors. It has workforce strength of over 2,200 employees and more than 3,000 specialist contractors across all states and territories. The market capitalisation of the company stood at ~A$969.81 million as of 28 November 2019. The company has released its results for FY19 and delivered another year of growth along with significant improvements throughout the key profitability measures. The company’s FY19 was highlighted by acquisition of Comdain Infrastructure on January 2, 2019, and its contribution to the company’s earnings for 2H of the financial year. The company’s revenue rose to $852.2 million from $632.9 million, which reflects a 35% YoY rise due to growth in each of 2 reporting segments of Telecommunications (+10%) and Utilities (+156%) and, notably, an acquisition of Comdain Infrastructure contributed $160.2 million (+150%) of Utilities. The company’s earnings before interest, tax, depreciation and amortisation (or EBITDA) stood at $89.5 million in FY19 as compared to $67.3 million in FY18, reflecting a 33% YoY rise. This follows the average annual growth in the same metric of 38% over the time span of preceding 3 financial years. SSM’s EBITDA growth was witnessed by each of Telecommunications (+22%), and Utilities (+127%) and acquisition of Comdain Infrastructure made the contribution amounting to $11.1 million (+106%) of the Utilities.

The company’s basic earnings per share (or EPS) stood at 13.09 cents in FY19 as compared to 11.29 cents in the previous year and the rise was primarily because of increase in the company’s NPAT despite an impact of higher average shares on issue including that arising from an issue of 40.189 Mn shares. These shares were issued as part consideration for the acquisition of Comdain Infrastructure. Form the dividends front, the company has declared a fully franked final dividend of 5.5 cents, which takes the total dividends in respect of FY19 to 9.0 cents (fully-franked) as compared to 7.5 cents (fully-franked) in respect of FY18, exhibiting an increase of 20%. Dividends have witnessed a CAGR growth of 56.51% in the time frame of between FY15- FY19 and, therefore, it can be said that the company has been focusing on delivering returns to its shareholders. Since FY16, the company’s dividend pay-out ratio has been increasing, and in FY19, pay-out ratio stood at 68.8%, which might be a point to consider for dividend seeking investors. Based on decent capabilities to generate revenues, respectable liquidity levels, a full-year contribution from Comdain Infrastructure and focus on identifying and assessing the further market expansion and diversification opportunities, we have valued the stock using two relative valuation methods, i.e., P/E and EV/EBITDA multiples, and arrived at a target price of lower double-digit growth (in percentage terms). At CMP of $2.50, the stock of the company is trading at P/E multiple 16.56x of FY20E consensus EPS.

.png)

Key Financial Highlights (Source: Thomson Reuters), *Dividend Payout Ratio - based on Statutory EPS

Top 10 Shareholders: The following table provides a brief overview of the top 10 shareholders in Service Stream Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Margins Higher Than Industry Median: The company’s key margins are higher than the broader industry median, which reflects that SSM’s financial standing is decent when compared to its industry. The company’s net margin stood at 5.9% in FY19, which is higher than the industry median of 2.7% and, therefore, it can be said that SSM has better capabilities to convert its top-line into the bottom-line as compared to the broader industry. Notably, the company’s gross margin stood at 95.6% in FY19 as compared to the industry median figure of 12.9%. The company’s RoE stood at 19.4% in FY19, which is higher than the industry median of 9.9% and, therefore, it can be said that SSM has been delivering better returns to its shareholders as compared to the broader industry. SSM’s current ratio stood at 1.25x as compared to the industry median figure of 1.14x, therefore, it can be said that the company has decent a liquidity position to meet its short-term obligations. Also, decent liquidity footing provides sufficient headroom to the company for making deployments towards strategic growth objectives. It looks like decent capabilities to convert its top-line into the bottom-line along with a decent liquidity position might help the company moving forward.

.png)

Key Ratios (Source: Thomson Reuters)

SSM Secures Agreement with Optus: Service Stream Limited announced that it had secured wireless design & construction agreement with Optus. The agreement happens to be a panel arrangement in the form of newly awarded Statement of Works for Mobile Deployment (or SoW) with Optus Mobile Pty Ltd, that operates under a pre-existing Group Master Supply Agreement with Singtel (or Singapore Telecommunications Limited).

Under the Statement of Work, SSM would initially be providing site acquisition, design and construction services on Optus network nationally, with regards to 5G. It was also added that the agreement allows for site upgrades, small cell and RANCAP services with respect to existing 4G infrastructure, subject to future negotiations. The SoW is having a term of 3 years with an option of the one-year extension.

Extension of NMRA Contract With nbn: Service Stream Limited made an announcement about the extension of its Network MACs and Restoration Activities contract with NBN Co. It was added that NMRA contract has been extended for the additional 18-month term out to June 30, 2021. The company’s revenue under NMRA contract was around $55 million in FY19 and $35 million in FY18.

Improvement in Financial Position: The financial position of SSM has witnessed an improvement during FY19, and net assets as at June 30, 2019, amounted to $307.8 million as compared to $206.9 million as at June 30, 2018. The company stated that $70.4 million of an increase was because of issuance of 40.189 million shares. As at June 30, 2019, the company’s current assets exceeded its current liabilities by $53.4 million.

.png)

Improvement in Net Assets (Source: Company Reports)

Overview of Overall Group’s Strategy: The financial performance of SSM has witnessed an improvement during FY19, and it delivered on the strategic plan in line with the expectation of the Board. Considering the company’s robust financial position, Board of the company has been reviewing SSM’s capital management strategy in order to ensure that it remains effective when it comes to maximising the shareholder value. The following image provides the information related to the dividends:

.png)

Dividends (Source: Company Reports)

Dividend Continues to Improve: The Board of the company declared increased final dividend amounting to 5.5 cents per share (fully-franked), which takes the total dividends with regards to FY19 to 9.0 cents per share (fully-franked) that happens to be in line with the company’s progressive dividend policy approach. As can be seen in the following image, the company’s dividends have been increasing since FY 15 and, thus, it can be said that SSM has been focusing on delivering respectable returns to its shareholders.

.png)

Key Indicators (Source: Company Reports)

Moving forward, there are expectations that the growth in EPS since FY 15 as well as in dividends per share might help the overall company to attract the attention of the market participants.

What to Expect from SSM Moving Forward: The company has been focusing towards 5 fundamentals that drive operational effectiveness, continual improvement as well as help the future growth. These include service delivery, client relationships, optimising the delivery model, people, and delivering growth. The company has been anticipating continued growth in revenues and profits in FY20 and the year would be characterised by full-year contribution from Comdain Infrastructure, which might get partly offset by reduced earnings as a result of a cessation of nbn D&C operations.

The main priorities for FY20 consist of securing the organic growth opportunities as and when they emerge throughout the existing operations and maintenance of readiness to deliver the increased volume of wireless services as 5G upgrade/augmentation activities witnesses a gain in the momentum. In addition, the company is expecting that Fixed Communications would grow, considering the extensions that have been secured to OMMA and NMRA agreements.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: EV/EBITDA multiple Approach

.png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

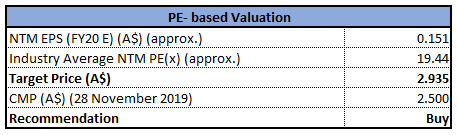

Method 1:PE- Based Valuation

PE- Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

.png)

Historical PE Band (Source: Thomson Reuters)

Stock Recommendation: The stock of SSM has witnessed an increase of 36.39% on YTD basis, while in the time frame of the past one year, it has increased 40.83%. The company manages capital in order to make sure that it is able to continue as the going concern and maximise the returns to its shareholders. To maintain or to adjust the capital structure, the company has the power to adjust amount of dividends as well as return capital paid to the shareholders or issue new shares. It was further added that the capital is managed to maintain a decent financial position and to ensure that the financing needs could be optimised at all times in a cost-efficient manner in order to support a goal of maximising the wealth of shareholders. The company’s revenues have witnessed a CAGR growth of 19.98% in the span of FY15- FY19, while its bottom-line encountered a CAGR growth of 43.62% during the same time span. Based on decent capabilities to generate revenues, respectable liquidity levels, a full-year contribution from Comdain Infrastructure and focus on identifying and assessing the further market expansion and diversification opportunities, we have valued the stock using two relative valuation methods, i.e., P/E and EV/EBITDA multiples, and arrived at a target price of lower double-digit growth (in percentage terms). Hence, we give a “Buy” rating on the stock at the current market price of A$2.500 per share (up 5.042% on 28 November 2019).

SSM Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...